Capital One 2003 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2003 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

In addition, the occurrence of certain events may cause the securitization transactions to amortize earlier than

scheduled, which would accelerate the need for additional funding. This early amortization could, among other

things, have a significant effect on the ability of the Bank and the Savings Bank to meet the capital adequacy

requirements as all off-balance sheet loans experiencing such early amortization would have to be recorded on

the balance sheet. See page 52 in Item 7 “Management’s Discussion and Analysis of Financial Condition and

Results of Operations—Liquidity Risk Management” of this form.

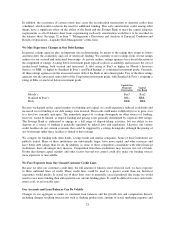

We May Experience Changes in Our Debt Ratings

In general, ratings agencies play an important role in determining, by means of the ratings they assign to issuers

and their debt, the availability and cost of wholesale funding. We currently receive ratings from several ratings

entities for our secured and unsecured borrowings. As private entities, ratings agencies have broad discretion in

the assignment of ratings. A rating below investment grade typically reduces availability and increases the cost of

market-based funding, both secured and unsecured. A debt rating of Baa3 or higher by Moody’s Investors

Service, or BBB- or higher by Standard & Poor’s and Fitch Ratings, is considered investment grade. Currently,

all three ratings agencies rate the unsecured senior debt of the Bank as investment grade. Two of the three ratings

agencies rate the unsecured senior debt of the Corporation investment grade, with Standard & Poor’s assigning a

rating of BB+, or one level below investment grade.

Capital One

Financial

Corporation

Capital

One Bank

Moody’s Baa3 Baa2

Standard & Poor’s BB+ BBB-

Fitch BBB BBB

Because we depend on the capital markets for funding and capital, we could experience reduced availability and

increased cost of funding if our debt ratings were lowered. This result could make it difficult for us to grow at or

to a level we currently anticipate. The immediate impact of a ratings downgrade on other sources of funding,

however, would be limited, as deposit funding and pricing is not generally determined by corporate debt ratings.

The Savings Bank is authorized to engage in a full range of deposit-taking activities, but our ability to use

deposits as a source of funding is generally regulated by federal laws and regulations. Likewise, our various

credit facilities do not contain covenants that could be triggered by a ratings downgrade, although the pricing of

any borrowings under these facilities is linked to these ratings.

We compete for funding with other banks, savings banks and similar companies. Some of these institutions are

publicly traded. Many of these institutions are substantially larger, have more capital and other resources and

have better debt ratings than we do. In addition, as some of these competitors consolidate with other financial

institutions, these advantages may increase. Competition from these institutions may increase our cost of funds.

Events that disrupt capital markets and other factors beyond our control could also make our funding sources

more expensive or unavailable.

We Face Exposure from Our Unused Customer Credit Lines

Because we offer our customers credit lines, the full amount of which is most often not used, we have exposure

to these unfunded lines of credit. These credit lines could be used to a greater extent than our historical

experience would predict. If actual use of these lines were to materially exceed predicted line usage, we would

need to raise more funding than anticipated in our current funding plans. It could be difficult to raise such funds,

either at all, or at favorable rates.

Our Accounts and Loan Balances Can Be Volatile

Changes in our aggregate accounts or consumer loan balances and the growth rate and composition thereof,

including changes resulting from factors such as shifting product mix, amount of actual marketing expenses and

23