Capital One 2003 Annual Report Download - page 113

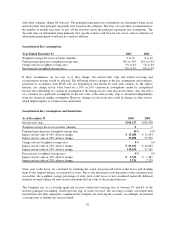

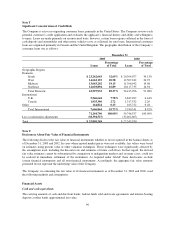

Download and view the complete annual report

Please find page 113 of the 2003 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

Hedge of Net Investment in Foreign Operations

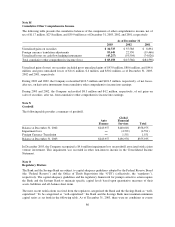

The Company uses cross-currency swaps and forward exchange contracts to protect the value of its investment in

its foreign subsidiaries. Realized and unrealized foreign currency gains and losses from these hedges are not

included in the income statement, but are shown in the translation adjustments in other comprehensive income.

The purpose of these hedges is to protect against adverse movements in exchange rates.

For the year ended December 31, 2003 and 2002, net losses of $6.0 million and $3.2 million related to these

derivatives were included in the cumulative translation adjustment.

Non-Trading Derivatives

The Company uses interest rate swaps to manage interest rate sensitivity related to loan securitizations. The

Company enters into interest rate swaps with its securitization trust and essentially offsets the derivative with

separate interest rate swaps with third parties.

The Company uses interest rate swaps in conjunction with its auto securitizations that are not designated hedges.

These swaps have zero balance notional amounts unless the paydown of auto securitizations differs from its

scheduled amortization.

These derivatives do not qualify as hedges and are recorded on the balance sheet at fair value with changes in

value included in current earnings. During the years ended December 31, 2003 and 2002, the Company had net

losses of $2.2 million and $2.3 million, respectively. The Company recognized net losses of $2.0 million during

the year ended December 31, 2003, for non-trading derivatives that were terminated.

95