Capital One 2003 Annual Report Download - page 70

Download and view the complete annual report

Please find page 70 of the 2003 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

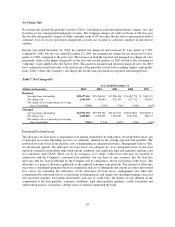

Liquidity Risk Management

Liquidity risk management refers to the way the Company manages the use and availability of various funding

sources to meet its current and future operating needs. These needs change as loans grow, securitizations

amortize, debt and other deposits mature, and payments on other obligations are made. Because the

characteristics of the Company’s assets and liabilities change, liquidity risk management is a dynamic process,

affected by the pricing and maturity of investment securities, loans, deposits, securitizations and other assets and

liabilities.

To facilitate liquidity risk management, the Company uses a variety of funding sources to establish a maturity

pattern that provides a prudent mixture of short-term and long-term funds. The Company obtains funds through

the gathering of deposits, issuing debt and equity, and securitizing assets. Further liquidity is provided to the

Company through committed facilities. As of December 31, 2003, the Corporation, the Bank, the Savings Bank

and COAF collectively had over $10.9 billion in unused commitments under various credit facilities (including

the Collateralized Revolving Credit Facility) and unused conduit capacity available for liquidity needs.

Additionally, the Company maintains a portfolio of high-quality securities such as U.S. Treasuries and other U.S.

government obligations, mortgage backed securities, commercial paper, interest-bearing deposits with other

banks, federal funds and other cash equivalents in order to provide adequate liquidity and to meet its ongoing

cash needs. As of December 31, 2003, the Company had $7.8 billion of such securities, cash and cash

equivalents.

As discussed in “Off-Balance Sheet Arrangements,” a significant source of liquidity for the Company has been

the securitization of consumer loans. As of December 31, 2003 the Company funded approximately 53% of its

managed loans through off-balance sheet securitizations. The Company expects to securitize additional loan

principal receivables during 2004. Maturities of existing securitizations vary from 2004 to 2013, and for

revolving securitizations have accumulation periods during which principal payments are aggregated to make

payments to investors. As payments on the loans are accumulated and are no longer reinvested in new loans, the

Company’s funding requirements for such new loans increase accordingly. The occurrence of certain events may

cause the securitization transactions to amortize earlier than scheduled, which would accelerate the need for

funding. Additionally, this early amortization could have a significant effect on the ability of the Bank and the

Savings Bank to meet the capital adequacy requirements as all off-balance sheet loans experiencing such early

amortization would have to be recorded on the balance sheet. As such amounts mature or are otherwise paid, the

Company believes it can securitize additional consumer loans, gather deposits, purchase federal funds and

establish other funding sources to fund new loan growth, although no assurance can be given to that effect.

The consumer asset-backed securitization market in the United States currently exceeds $1.4 trillion, with

approximately $514.0 billion issued in 2003. The Company is a leading issuer in these markets, which have

remained stable through adverse conditions. Despite the size and relative stability of these markets and the

Company’s position as a leading issuer, if these markets experience difficulties the Company may be unable to

securitize its loan receivables or to do so at favorable pricing levels. Factors affecting the Company’s ability to

securitize its loan receivables or to do so at favorable pricing levels include the overall credit quality of the

Company’s securitized loans, the stability of the market for securitization transactions, and the legal, regulatory,

accounting and tax environments governing securitization transactions. If the Company was unable to continue to

securitize its loan receivables at current levels, the Company would use its investment securities and money

market instruments in addition to alternative funding sources to fund increases in loan receivables and meet its

other liquidity needs. The resulting change in the Company’s current liquidity sources could potentially subject

the Company to certain risks. These risks would include an increase in the Company’s cost of funds, an increase

in the reserve for possible credit losses and the provision for possible credit losses as more loans would remain

on the Company’s consolidated balance sheet, and lower loan growth, if the Company were unable to find

alternative and cost-effective funding sources. In addition, if the Company could not continue to remove the loan

receivables from the balance sheet the Company would possibly need to raise additional capital to support loan

and asset growth and potentially provide additional credit enhancement.

52