Capital One 2003 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2003 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

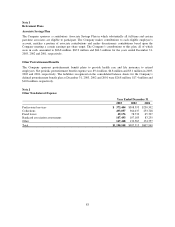

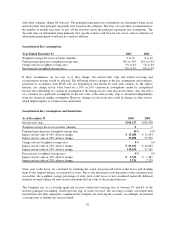

The following table presents the year-end and average balances, as well as the delinquent and net charge-off

amounts of the reported, off-balance sheet and managed consumer loan portfolios.

Supplemental Loan Information

Year Ended December 31

2003 2002

Loans

Outstanding

Loans

Delinquent

Loans

Outstanding

Loans

Delinquent

Managed loans $ 71,244,796 $ 3,177,929 $ 59,746,537 $ 3,345,394

Securitization adjustments (38,394,527) (1,604,470) (32,402,607) (1,671,525)

Reported consumer loans $ 32,850,269 $ 1,573,459 $ 27,343,930 $ 1,673,869

Average

Loans

Net

Charge-

Offs

Average

Loans

Net

Charge-

Offs

Managed loans $ 62,911,953 $ 3,683,887 $ 52,799,566 $ 2,769,249

Securitization adjustments (34,234,337) (2,037,527) (27,763,547) (1,509,565)

Reported consumer loans $ 28,677,616 $ 1,646,360 $ 25,036,019 $ 1,259,684

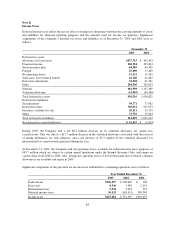

The Company’s retained residual interests in the off-balance sheet securitizations are recorded in accounts

receivable from securitizations and are comprised of interest-only strips, retained subordinated undivided

interests in the transferred receivables, cash collateral accounts, cash reserve accounts and unpaid interest and

fees on the investors’ portion of the transferred principal receivables. The interest-only strip is recorded at fair

value, while the other residual interests are carried at cost, which approximates fair value. Retained residual

interests totaled $2.2 billion and $1.6 billion at December 31, 2003 and 2002, respectively. The Company’s

retained residual interests are generally restricted or subordinated to investors’ interests and their value is subject

to substantial credit, repayment and interest rate risks on the transferred financial assets. The investors and the

trusts have no recourse to the Company’s assets, other than the retained residual interests, if the off-balance sheet

loans are not paid when due.

The gain on sale recorded from off-balance sheet securitizations is based on the estimated fair value of the assets

sold and retained and liabilities incurred, and is recorded at the time of sale in servicing and securitizations

income on the Consolidated Statements of Income. The related receivable is the interest-only strip, which is

based on the present value of the estimated future cash flows from excess finance charges and past-due fees over

the sum of the return paid to security holders, estimated contractual servicing fees and credit losses. The

Company periodically reviews the key assumptions and estimates used in determining the value of the interest-

only strip. Prior to December 31, 2002, decreases in fair value below the carrying amount as a result of changes

in the key assumptions were recognized in “servicing and securitizations” income, while increases in fair values

as a result of changes in key assumptions were recorded as unrealized gains and included as a component of

cumulative other comprehensive income, on a net-of-tax basis, in accordance with the provisions of SFAS No.

115, Accounting for Certain Investments in Debt and Equity Securities. Effective December 31, 2002 and for all

subsequent periods, the Company recognizes all changes in the fair value of the interest-only strip immediately in

servicing and securitizations income on the consolidated statements of income. In accordance with Emerging

Issues Task Force 99-20 (“EITF 99-20”), Recognition of Interest Income and Impairment of Purchased and

Retained Beneficial Interests in Securitized Financial Assets, the interest component of cash flows attributable to

retained interests in securitizations is recorded in other interest income.

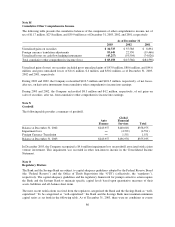

The key assumptions used in determining the fair value of the interest-only strips resulting from securitizations of

consumer loan receivables completed during the period included the weighted average ranges for charge-off

rates, principal repayment rates, lives of receivables and discount rates included in the following table. The

charge-off rates are determined using forecasted net charge-offs expected for the trust calculated consistently

91