Asus 2014 Annual Report Download - page 251

Download and view the complete annual report

Please find page 251 of the 2014 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

249 -

250

250 -

251

251 -

252

252 -

253

253 -

254

254 -

255

255 -

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

247

Depositary may issue new GDRs in proportion to GDRs holding ratios or raise the

number of shares of common stock represented by each unit of GDR or sell stock

dividends on behalf of GDR holders and distribute proceeds to them in proportion to

their GDRs holding ratios.

C. Treasury shares

(A) To enhance the Company’s credit and shareholders’ equ it y, t he Company reacquired its

treasury shares. During the period from July 2, 2013 to August 20, 2013, the shares

reaquired were 10,000,000 shares, amounting to $2,525,987. All of the treasury shares

had been retired on November 21, 2013.

(B) Pursuant to R.O.C. Securities and Exchange Law, the number of shares bought back as

treasury shares should not exceed 10% of the number of the Company’s issued and

outstanding shares and the amount bought back should not exceed the sum of retained

earnings, paid-in capital in excess of par value and realized capital surplus.

(C) Pursuant to R.O.C. Securities and Exchange Law, treasury shares should not be pledged

as collateral and the shareholder’s rights should not be enjoyed before transfer.

(D) Pursuant to R.O.C. Securities and Exchange Law, treasury shares should be transferred

to the employees within three years from the reacquisition date and shares not

transferred within the three-year period should be retired. Treasury shares to enhance

the Company’s credit and the shareholders’ equity should be retired within six months

from the reacquisition date.

(12) Capital surplus

Pursuant to R.O.C. Company Law, capital surplus arising from paid-in capital in excess of par

value on issuance of common stocks and donations can be used to cover accumulated deficit or

to issue new stocks or cash to shareholders in proportion to their share ownership, provided that

the Company has no accumulated deficit. Further, R.O.C. Securities and Exchange Law requires

that the amount of capital surplus to be capitalised mentioned above should not exceed 10% of

the paid-in capital each year. Capital surplus should not be used to cover accumulated deficit

unless the legal reserve is insufficient.

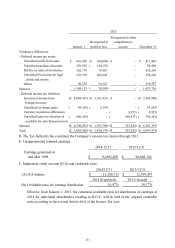

Difference between Changes in

proceeds from associates and joint

acquisition or disposal

ventures accounted

of subsidiary and for under

Share premium book value equity method Total

At January 1, 2014 4,227,966$ 227,466$ 3,195)($ 4,452,237$

Effect of changes in - 942)( 1,462 520

percentage of

ownership

At December 31, 2014

4,227,966$ 226,524$ 1,733)($ 4,452,757$