Asus 2014 Annual Report Download - page 171

Download and view the complete annual report

Please find page 171 of the 2014 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

167

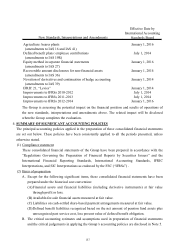

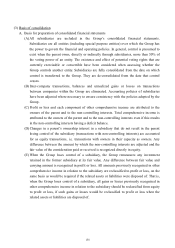

(8) Available-for-sale financial assets

A. Available-for-sale financial assets are non-derivatives that are either designated in this category

or not classified in any of the other categories.

B. On a regular way purchase or sale basis, available-for-sale financial assets are recognized and

derecognized using trade date accounting.

C. Available-for-sale financial assets are initially recognized at fair value plus transaction costs.

These financial assets are subsequently remeasured and stated at fair value, and any changes in

the fair value of these financial assets are recognized in other comprehensive income.

Investments in equity instruments that do not have a quoted market price in an active market

and whose fair value cannot be reliably measured or derivatives that are linked to and must be

settled by delivery of such unquoted equity instruments are presented in “financial assets

measured at cost”.

(9) Loans and receivables

Trade receivables are loans and receivables originated by the entity. They are created by the entity

by selling goods or providing services to customers in the ordinary course of business. Trade

receivables are initially recognized at fair value and subsequently measured at amortised cost using

the effective interest method, less provision for impairment. Due to the insignificant discount effect

on the non-interest bearing short-term receivables, they are measured at the original invoice

amount.

(10) Impairment of financial assets

A. The Group assesses at the end of the financial reporting period whether there is objective

evidence that a financial asset or a group of financial assets is impaired as a result of one or

more events that occurred after the initial recognition of the asset (a “loss event”) and that

loss event has an impact on the estimated future cash flows of the financial asset or group of

financial assets that can be reliably estimated.

B. The criteria that the Group uses to determine whether there is objective evidence of an

impairment loss is as follows:

(A) Significant financial difficulty of the issuer or debtor;

(B) A breach of contract, such as a default or delinquency in interest or principal payments;

(C) The Group, for economic or legal reasons relating to the borrower’s financial difficulty,

granted the borrower a concession that a lender would not otherwise consider;

(D) It becomes probable that the borrower will enter bankruptcy or other financial

reorganization;

(E) The disappearance of an active market for that financial asset because of financial

difficulties;

(F) Observable data indicating that there is a measurable decrease in the estimated future

cash flows from a group of financial assets since the initial recognition of those assets,

although the decrease cannot yet be identified with the individual financial asset in the