Asus 2014 Annual Report Download - page 162

Download and view the complete annual report

Please find page 162 of the 2014 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

158

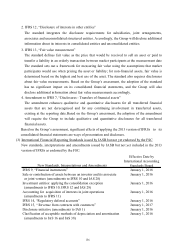

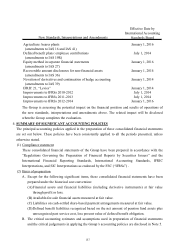

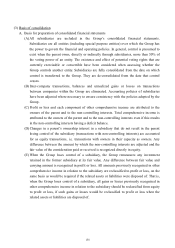

(3) Basis of consolidation

A. Basis for preparation of consolidated financial statements

(A) All subsidiaries are included in the Group’s consolidated financial statements.

Subsidiaries are all entities (including special purpose entities) over which the Group has

the power to govern the financial and operating policies. In general, control is presumed to

exist when the parent owns, directly or indirectly through subsidiaries, more than 50% of

the voting power of an entity. The existence and effect of potential voting rights that are

currently exercisable or convertible have been considered when assessing whether the

Group controls another entity. Subsidiaries are fully consolidated from the date on which

control is transferred to the Group. They are de-consolidated from the date that control

ceases.

(B) Inter-company transactions, balances and unrealized gains or losses on transactions

between companies within the Group are eliminated. Accounting policies of subsidiaries

have been adjusted where necessary to ensure consistency with the policies adopted by the

Group.

(C) Profit or loss and each component of other comprehensive income are attributed to the

owners of the parent and to the non-controlling interests. Total comprehensive income is

attributed to the owners of the parent and to the non-controlling interests even if this results

in the non-controlling interests having a deficit balance.

(D) Changes in a parent’s ownership interest in a subsidiary that do not result in the parent

losing control of the subsidiary (transactions with non-controlling interests) are accounted

for as equity transactions, i.e. transactions with owners in their capacity as owners. Any

difference between the amount by which the non-controlling interests are adjusted and the

fair value of the consideration paid or received is recognized directly in equity.

(E) When the Group loses control of a subsidiary, the Group remeasures any investment

retained in the former subsidiary at its fair value. Any difference between fair value and

carrying amount is recognized in profit or loss. All amounts previously recognized in other

comprehensive income in relation to the subsidiary are reclassified to profit or loss, on the

same basis as would be required if the related assets or liabilities were disposed of. That is,

when the Group loses control of a subsidiary, all gains or losses previously recognized in

other comprehensive income in relation to the subsidiary should be reclassified from equity

to profit or loss, if such gains or losses would be reclassified to profit or loss when the

related assets or liabilities are disposed of.