Asus 2014 Annual Report Download - page 200

Download and view the complete annual report

Please find page 200 of the 2014 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

196

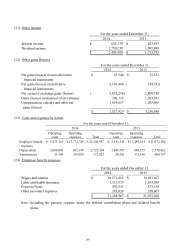

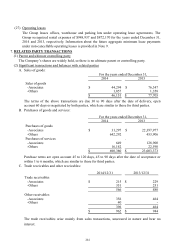

(17) Capital surplus

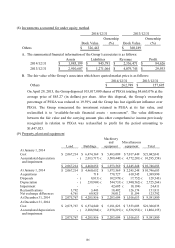

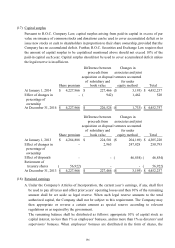

Pursuant to R.O.C. Company Law, capital surplus arising from paid-in capital in excess of par

value on issuance of common stocks and donations can be used to cover accumulated deficit or to

issue new stocks or cash to shareholders in proportion to their share ownership, provided that the

Company has no accumulated deficit. Further, R.O.C. Securities and Exchange Law requires that

the amount of capital surplus to be capitalised mentioned above should not exceed 10% of the

paid-in capital each year. Capital surplus should not be used to cover accumulated deficit unless

the legal reserve is insufficient.

(18) Retained earnings

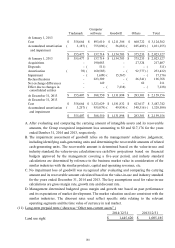

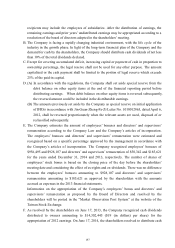

A. Under the Company’s Articles of Incorporation, the current year’s earnings, if any, shall first

be used to pay all taxes and offset prior years’ operating losses and then 10% of the remaining

amount shall be set aside as legal reserve. When such legal reserve amounts to the total

authorized capital, the Company shall not be subject to this requirement. The Company may

then appropriate or reverse a certain amount as special reserve according to relevant

regulations or as required by the government.

The remaining balance shall be distributed as follows: appropriate 10% of capital stock as

capital interest, no less than 1% as employees’ bonuses, and no more than 1% as directors’ and

supervisors’ bonuses. When employees’ bonuses are distributed in the form of shares, the

Difference between Changes in

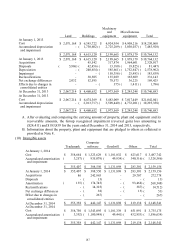

proceeds from

associates and joint

acquisition or disposal

ventures accounted

of subsidiary and for under

Share premium

book value equity method Total

At January 1, 2014 4,227,966$ 227,466$ 3,195)($ 4,452,237$

Effect of changes in - 942)( 1,462 520

percentage of

ownership

At December 31, 2014 4,227,966$ 226,524$ 1,733)($ 4,452,757$

Difference between Changes in

proceeds from

associates and joint

acquisition or disposal

ventures accounted

of subsidiary and for under

Share premium

book value equity method Total

At January 1, 2013 4,284,888$ 224,501$ 204,169)($ 4,305,220$

Effect of changes in - 2,965 247,828 250,793

percentage of

ownership

Effect of disposals - - 46,854)( 46,854)(

Retirement of

treasury shares 56,922)( - - 56,922)(

At December 31, 2013 4,227,966$ 227,466$ 3,195)($ 4,452,237$