Asus 2014 Annual Report Download - page 238

Download and view the complete annual report

Please find page 238 of the 2014 Asus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

228 -

229

229 -

230

230 -

231

231 -

232

232 -

233

233 -

234

234 -

235

235 -

236

236 -

237

237 -

238

238 -

239

239 -

240

240 -

241

241 -

242

242 -

243

243 -

244

244 -

245

245 -

246

246 -

247

247 -

248

248 -

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

|

|

234

M. According to “Regulations Governing the Preparation of Financial Reports by Securities

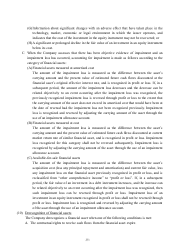

Issuers”, profit and other comprehensive income in the separate financial statements should

be the same as profit and other comprehensive income attributable to shareholders of the

parent in the consolidated financial statements, and the equity in the separate financial

statements should be the same as the equity attributable to shareholders of the parent in the

consolidated financial statements.

(14) Property, plant and equipment

A. Property, plant and equipment are initially recorded at cost. Borrowing costs incurred during

the construction period are capitalised.

B. Subsequent costs are included in the asset’s carrying amount or recognized as a separate asset,

as appropriate, only when it is probable that future economic benefits associated with the

item will flow to the Company and the cost of the item can be measured reliably. The

carrying amount of the replaced part is derecognized. All other repairs and maintenance are

charged to profit or loss during the financial period in which they are incurred.

C. Except for land which is not depreciated, other property, plant and equipment apply cost

model and are depreciated using the straight-line method to allocate their cost over their

estimated useful lives. If each component of property, plant and equipment is significant, it

should be depreciated separately.

D. The assets’ residual values, useful lives and depreciation methods are reviewed, and adjusted

if appropriate, at each end of the financial reporting period. If expectations for the assets’

residual values and useful lives differ from previous estimates or the patterns of consumption

of the assets’ future economic benefits embodied in the assets have changed significantly, any

change is accounted for as a change in estimate under IAS 8, “Accounting Policies, Changes

in Accounting Estimates and Errors”, from the date of the change. The estimated useful lives

of the buildings are 10~50 years, machinery and equipment are 3 years and miscellaneous

equipment are 1~15 years.

(15) Leased assets/ leases (lessee)

An operating lease is a lease that the lessor assumes substantially all the risks and rewards

incidental to ownership of the leased asset. Payments made under an operating lease (net of any

incentives received from the lessor) are recognized in profit or loss on a straight-line basis over

the lease term.

(16) Investment property

An investment property is stated initially at its cost and measured subsequently using the cost

model. Except for land, investment property is depreciated on a straight-line basis over its

estimated useful life of 50 years.

(17) Intangible assets

Computer software is amortised on a straight-line basis over its estimated useful life of 1~5

years.