Experian 2007 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2007 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

|

|

Experian Annual Report2007 |67

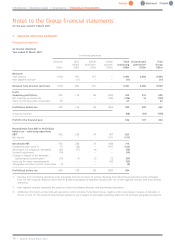

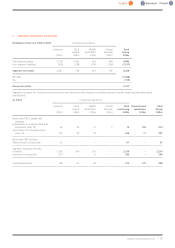

2. Basis of preparation and significant accounting policies (continued)

Acquisition intangibles

Trade marks and licences

Trade marks and licences are carried at cost and are amortised on a straight line basis over their contractual lives, up to a maximum period of 20 years.

Trade names

Legally protected or otherwise separable trade names acquired as part of a business combination are capitalised at fair value on acquisition and

amortised on a straight line basis over three to eight years based on management’s expectations to retain trade names within the business.

Customer relationships

Contractual and non-contractual customer relationships acquired as part of a business combination are capitalised at fair value on acquisition and

amortised on a straight line basis over three to eight years based on management’s estimates of the average lives of customer relationships.

Completed technology

The fair value of completed technology acquired as part of a business combination is capitalised as an intangible asset. Completed technology is

held at fair value on acquisition and amortised on a straight line basis over three to eight years based on the expected life of the asset.

Property, plant and equipment

Property, plant and equipment is held at cost less accumulated depreciation and any impairment in value.

Land is not depreciated.

Equipment on hire or lease is depreciated over the lower of the useful life and period of the lease.

Depreciation is provided on other property, plant and equipment at rates calculated to depreciate the cost, less estimated residual value based on

prices prevailing at the balance sheet date, of each asset evenly over its expected useful life as follows:

•Freehold properties are depreciated over 50 years;

•Leasehold premises with lease terms of 50 years or less are depreciated over the remaining period of the lease; and

•Plant, vehicles and equipment aredepreciated over two to ten years according to the estimated life of the asset.

Contingent consideration

Wherepartor all of the amount of purchase consideration is contingent on futureevents, the cost of the acquisition initially recorded includes a

reasonable estimate of the fair value of the contingent amounts expected to be payable in the future. The cost of the acquisition is adjusted when

revised estimates are made, with corresponding adjustments made to goodwill until the ultimate outcome is known.

Where part or all of the amount of disposal consideration is contingent on future events, the disposal proceeds initially recorded include a

reasonable estimate of the fair value of the contingent amounts expected to be receivable in the future. The proceeds are adjusted when revised

estimates are made, with corresponding adjustments made to debtors, and profit and loss on disposal, until the ultimate outcome is known.

Trade receivables

Trade receivables are initially recognised at fair value and carried at the lower of fair value (original invoice amount) and recoverable amount. Where

the time value of money is material, receivables arecarried at amortised cost.

Aprovision for impairment of trade receivables is established when there is objective evidence that the Group will not be able to collect all amounts

due according to the original terms of receivables. Any charge or credit in respect of such provisions is recognised in the Group income statement.

The cost of any irrecoverable trade receivables is recognised in the Group income statement immediately.

Available for sale assets

Available for sale assets are non-derivative financial assets that are either designated to this category or not classified in any of the other financial

asset categories. Available for sale assets are carried at fair value and are included in non-current assets unless management intends to dispose of

the assets within 12 months of the balance sheet date. Unrealised gains and losses on available for sale assets are recognised directly in equity. On

disposal or impairment of the assets, the gains and losses in equity are recycled through the income statement. At each balance sheet date, the

Group assesses whether there is objective evidence to suggest that available for sale assets are impaired. In the case of equity securities, a significant

or prolonged decline in the fair value of the security below its cost is considered in determining whether the security is impaired. If any such

evidence exists, the cumulative loss is removed from equity and recognised in the Group income statement. Impairment losses recognised in the

Group income statement on equity instruments are not subsequently reversed through the Group income statement.

Borrowings and borrowing costs

Borrowings are recognised initially at fair value, net of transaction costs incurred. Borrowings are subsequently stated at amortised cost unless they

are part of a fair value hedge accounting relationship. Initial differences between the proceeds of fixed rate borrowings and the redemption values

are recognised in the income statement over the period of the borrowings using the effective interest rate method. Borrowings that are subject to a

fair value hedge accounting relationship aremeasured at amortised cost adjusted for the change in fair value attributable to hedged risks.

Borrowings are classified as non-current to the extent that the Group has an unconditional right to defer settlement of the liability for at least 12

months after the balance sheet date.

Incremental borrowing costs which are directly attributable to the issue of debt are capitalised and amortised over the expected life of the

borrowing using the effective interest rate method. All other borrowing costs are expensed in the year in which they are incurred.