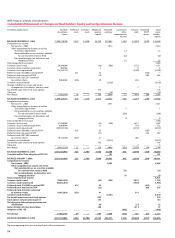

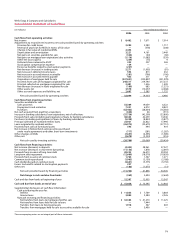

Wells Fargo 2006 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2006 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

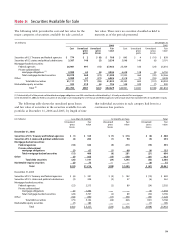

80

(in millions) December 31, 2006

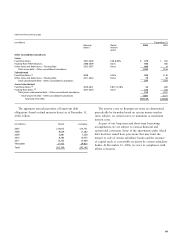

Total Weighted- Remaining contractual principal maturity

amount average After one year After five years

yield Within one year through five years through ten years After ten years

Amount Yield Amount Yield Amount Yield Amount Yield

Securities of U.S. Treasury

and federal agencies $ 768 4.56% $134 5.20% $ 551 4.33% $ 78 4.89% $ 5 7.66%

Securities of U.S. states and

political subdivisions 3,530 7.17 166 7.99 437 6.56 708 6.97 2,219 7.29

Mortgage-backed securities:

Federal agencies 27,463 5.91 2 7.11 43 6.99 68 5.84 27,350 5.91

Private collateralized

mortgage obligations 4,046 5.92 — — — — — — 4,046 5.92

Total mortgage-backed securities 31,509 5.91 2 7.11 43 6.99 68 5.84 31,396 5.91

Other 6,026 6.45 226 6.38 4,289 6.22 975 7.18 536 7.00

Total debt securities at fair value (1) $41,833 6.07% $528 6.59% $5,320 6.06% $1,829 6.95% $34,156 6.02%

(1) The weighted-average yield is computed using the contractual life amortization method.

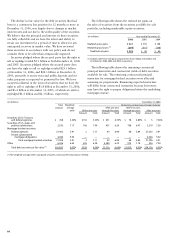

(in millions) Year ended December 31,

2006 2005 2004

Realized gross gains $ 621 $ 355 $ 168

Realized gross losses (1) (295) (315) (108)

Realized net gains $ 326 $40 $60

(1) Includes other-than-temporary impairment of $22 million, $45 million and

$9 million for 2006, 2005 and 2004, respectively.

The decline in fair value for the debt securities that had

been in a continuous loss position for 12 months or more at

December 31, 2006, was largely due to changes in market

interest rates and not due to the credit quality of the securities.

We believe that the principal and interest on these securities

are fully collectible and we have the intent and ability to

retain our investment for a period of time to allow for any

anticipated recovery in market value. We have reviewed

these securities in accordance with our policy and do not

consider them to be other-than-temporarily impaired.

Securities pledged where the secured party has the right to

sell or repledge totaled $5.3 billion at both December 31, 2006

and 2005. Securities pledged where the secured party does

not have the right to sell or repledge totaled $29.3 billion

at December 31, 2006, and $24.3 billion at December 31,

2005, primarily to secure trust and public deposits and for

other purposes as required or permitted by law. We have

accepted collateral in the form of securities that we have the

right to sell or repledge of $1.8 billion at December 31, 2006,

and $3.4 billion at December 31, 2005, of which we sold or

repledged $1.4 billion and $2.3 billion, respectively.

The following table shows the remaining contractual

principal maturities and contractual yields of debt securities

available for sale. The remaining contractual principal

maturities for mortgage-backed securities were allocated

assuming no prepayments. Remaining expected maturities

will differ from contractual maturities because borrowers

may have the right to prepay obligations before the underlying

mortgages mature.

The following table shows the realized net gains on

the sales of securities from the securities available for sale

portfolio, including marketable equity securities.