Wells Fargo 2006 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2006 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

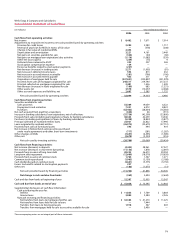

73

portfolio yield within capital risk limits approved by

management and the Board of Directors and monitored by

the Corporate Asset/Liability Management Committee. We

recognize realized gains and losses on the sale of these securities

in noninterest income using the specific identification method.

Unamortized premiums and discounts are recognized in

interest income over the contractual life of the security using

the interest method. As principal repayments are received on

securities (i.e., primarily mortgage-backed securities) a pro-rata

portion of the unamortized premium or discount is recognized

in interest income.

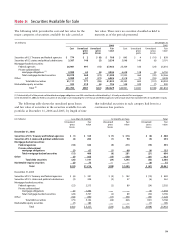

NONMARKETABLE EQUITY SECURITIES Nonmarketable equity

securities include venture capital equity securities that are

not publicly traded and securities acquired for various pur-

poses, such as to meet regulatory requirements (for example,

Federal Reserve Bank and Federal Home Loan Bank stock).

We review these assets at least quarterly for possible other-

than-temporary impairment. Our review typically includes

an analysis of the facts and circumstances of each invest-

ment, the expectations for the investment’s cash flows and

capital needs, the viability of its business model and our exit

strategy. These securities are accounted for under the cost or

equity method and are included in other assets. We reduce

the asset value when we consider declines in value to be

other than temporary. We recognize the estimated loss as

a loss from equity investments in noninterest income.

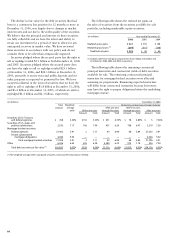

Mortgages Held for Sale

Mortgages held for sale include residential mortgages that

were originated in accordance with secondary market pricing

and underwriting standards and certain mortgages originated

initially for investment and not underwritten to secondary

market standards, and are stated at the lower of cost or market

value. Gains and losses on loan sales (sales proceeds minus

carrying value) are recorded in noninterest income. Direct

loan origination costs and fees are deferred at origination

of the loan. These deferred costs and fees are recognized in

mortgage banking noninterest income upon sale of the loan.

Loans Held for Sale

Loans held for sale are carried at the lower of cost or market

value. Gains and losses on loan sales (sales proceeds minus

carrying value) are recorded in noninterest income. Direct

loan origination costs and fees are deferred at origination

of the loan. These deferred costs and fees are recognized

in noninterest income upon sale of the loan.

Loans

Loans are reported at their outstanding principal balances

net of any unearned income, charge-offs, unamortized

deferred fees and costs on originated loans and premiums or

discounts on purchased loans, except for certain purchased

loans, which are recorded at fair value on their purchase date.

Unearned income, deferred fees and costs, and discounts and

premiums are amortized to income over the contractual life

of the loan using the interest method.

Lease financing assets include aggregate lease rentals, net

of related unearned income, which includes deferred investment

tax credits, and related nonrecourse debt. Leasing income

is recognized as a constant percentage of outstanding lease

financing balances over the lease terms.

Loan commitment fees are generally deferred and amor-

tized into noninterest income on a straight-line basis over the

commitment period.

From time to time, we pledge loans, primarily 1-4 family

mortgage loans, to secure borrowings from the Federal

Home Loan Bank.

NONACCRUAL LOANS We generally place loans on nonaccrual

status when:

• the full and timely collection of interest or principal

becomes uncertain;

• they are 90 days (120 days with respect to real estate

1-4 family first and junior lien mortgages and auto

loans) past due for interest or principal (unless both

well-secured and in the process of collection); or

• part of the principal balance has been charged off.

Generally, consumer loans not secured by real estate or

autos are placed on nonaccrual status only when part of the

principal has been charged off. These loans are charged off

or charged down to the net realizable value of the collateral

when deemed uncollectible, due to bankruptcy or other fac-

tors, or when they reach a defined number of days past due

based on loan product, industry practice, country, terms and

other factors.

When we place a loan on nonaccrual status, we reverse

the accrued and unpaid interest receivable against interest

income and account for the loan on the cash or cost recovery

method, until it qualifies for return to accrual status. Generally,

we return a loan to accrual status when (a) all delinquent

interest and principal becomes current under the terms of the

loan agreement or (b) the loan is both well-secured and in the

process of collection and collectibility is no longer doubtful.

IMPAIRED LOANS We assess, account for and disclose as impaired

certain nonaccrual commercial and commercial real estate

loans that are over $3 million. We consider a loan to be

impaired when, based on current information and events, we

will probably not be able to collect all amounts due according

to the loan contract, including scheduled interest payments.

When we identify a loan as impaired, we measure the

impairment based on the present value of expected future

cash flows, discounted at the loan’s effective interest rate,

except when the sole (remaining) source of repayment for

the loan is the operation or liquidation of the collateral. In

these cases we use an observable market price or the current

fair value of the collateral, less selling costs when foreclosure

is probable, instead of discounted cash flows.

If we determine that the value of the impaired loan is less

than the recorded investment in the loan (net of previous

charge-offs, deferred loan fees or costs and unamortized

premium or discount), we recognize impairment through an

allowance estimate or a charge-off to the allowance.