Wells Fargo 2006 Annual Report Download - page 116

Download and view the complete annual report

Please find page 116 of the 2006 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

-

128

|

|

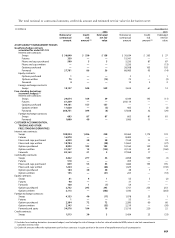

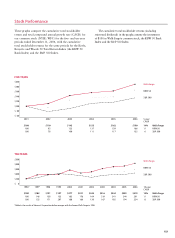

114

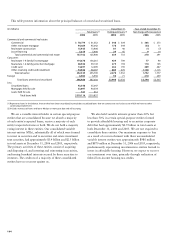

(in billions) To be well capitalized

For capital under the FDICIA prompt

Actual adequacy purposes corrective action provisions

Amount Ratio Amount Ratio Amount Ratio

As of December 31, 2006:

Total capital (to risk-weighted assets)

Wells Fargo & Company $51.4 12.50% >$32.9 >8.00%

Wells Fargo Bank, N.A. 40.6 12.05 > 27.0 >8.00 >$33.7 >10.00%

Tier 1 capital (to risk-weighted assets)

Wells Fargo & Company $36.8 8.95% >$16.5 >4.00%

Wells Fargo Bank, N.A. 29.2 8.66 > 13.5 >4.00 >$20.2 > 6.00%

Tier 1 capital (to average assets)

(Leverage ratio)

Wells Fargo & Company $36.8 7.89% >$18.7 >4.00%

(1)

Wells Fargo Bank, N.A. 29.2 7.46 > 15.7 >4.00

(1)

>$19.6 > 5.00%

(1) The leverage ratio consists of Tier 1 capital divided by quarterly average total assets, excluding goodwill and certain other items. The minimum leverage ratio guideline

is 3% for banking organizations that do not anticipate significant growth and that have well-diversified risk, excellent asset quality, high liquidity, good earnings,

effective management and monitoring of market risk and, in general, are considered top-rated, strong banking organizations.

Note 25: Regulatory and Agency Capital Requirements

The Company and each of its subsidiary banks are subject to

various regulatory capital adequacy requirements administered

by the Federal Reserve Board (FRB) and the OCC, respectively.

The Federal Deposit Insurance Corporation Improvement

Act of 1991 (FDICIA) required that the federal regulatory

agencies adopt regulations defining five capital tiers for banks:

well capitalized, adequately capitalized, undercapitalized,

significantly undercapitalized and critically undercapitalized.

Failure to meet minimum capital requirements can initiate

certain mandatory, and possibly additional discretionary,

actions by regulators that, if undertaken, could have a

direct material effect on our financial statements.

Quantitative measures, established by the regulators to

ensure capital adequacy, require that the Company and each

of the subsidiary banks maintain minimum ratios (set forth

in the table below) of capital to risk-weighted assets. There

are three categories of capital under the guidelines. Tier 1

capital includes common stockholders’ equity, qualifying

preferred stock and trust preferred securities, less goodwill

and certain other deductions (including a portion of servicing

assets and the unrealized net gains and losses, after taxes, on

securities available for sale). Tier 2 capital includes preferred

stock not qualifying as Tier 1 capital, subordinated debt,

the allowance for credit losses and net unrealized gains on

marketable equity securities, subject to limitations by the

guidelines. Tier 2 capital is limited to the amount of Tier 1

capital (i.e., at least half of the total capital must be in the

form of Tier 1 capital). Tier 3 capital includes certain

qualifying unsecured subordinated debt.

We do not consolidate our wholly-owned trusts (the Trusts)

formed solely to issue trust preferred securities. The amount of

trust preferred securities issued by the Trusts that was includable

in Tier 1 capital in accordance with FRB risk-based capital

guidelines was $4.1 billion at December 31, 2006. The junior

subordinated debentures held by the Trusts were included in

the Company’s long-term debt. (See Note 12.)

Under the guidelines, capital is compared with the relative

risk related to the balance sheet. To derive the risk included

in the balance sheet, a risk weighting is applied to each balance

sheet asset and off-balance sheet item, primarily based on the

relative credit risk of the counterparty. For example, claims

guaranteed by the U.S. government or one of its agencies are

risk-weighted at 0% and certain real estate related loans

risk-weighted at 50%. Off-balance sheet items, such as loan

commitments and derivatives, are also applied a risk weight

after calculating balance sheet equivalent amounts. A credit

conversion factor is assigned to loan commitments based on

the likelihood of the off-balance sheet item becoming an

asset. For example, certain loan commitments are converted

at 50% and then risk-weighted at 100%. Derivatives are

converted to balance sheet equivalents based on notional

values, replacement costs and remaining contractual terms.

(See Notes 6 and 26 for further discussion of off-balance

sheet items.) For certain recourse obligations, direct credit

substitutes, residual interests in asset securitization, and

other securitized transactions that expose institutions

primarily to credit risk, the capital amounts and classification

under the guidelines are subject to qualitative judgments

by the regulators about components, risk weightings and

other factors.

Management believes that, as of December 31, 2006, the

Company and each of the covered subsidiary banks met all

capital adequacy requirements to which they are subject.

The most recent notification from the OCC categorized

each of the covered subsidiary banks as well capitalized,

under the FDICIA prompt corrective action provisions

applicable to banks. To be categorized as well capitalized,

the institution must maintain a total risk-based capital ratio

as set forth in the table above and not be subject to a

capital directive order. There are no conditions or events