Wells Fargo 2006 Annual Report Download - page 2

Download and view the complete annual report

Please find page 2 of the 2006 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

|

|

2 To Our Owners

Building a culture of collaboration—

instinctively putting what’s best for the

customer first—is the key to outstanding

financial performance. Dick Kovacevich

and John Stumpf explain how we’re doing.

10 One Team. Pulling Together.

For Customers.

Our customers come to us every day

with financial problems they can’t solve,

financial questions they can’t answer,

financial needs they expect us to satisfy.

Eleven stories show how we do it.

24 One Team. Pulling Together.

For Communities.

We pull together as one Wells Fargo to

make our communities better places

to live and work. In financial capital alone,

we gave over $100 million to nonprofits

nationally for the first time.

31 Board of Directors, Senior Leaders

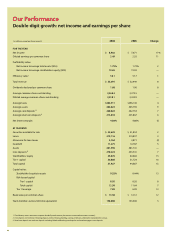

34 Financial Review

66 Controls and Procedures

68 Financial Statements

120 Report of Independent Registered

Public Accounting Firm

123 Stock Performance

124 Stockholder Information

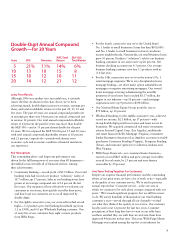

Which Measures Really Matter?

2006 Update (inside back cover)

Wells Fargo & Company (NYSE:WFC)

We’re a diversified financial services company

helping satisfy all our customers’ financial

needs—and helping them succeed financially

—through banking, insurance, investments,

mortgage loans and consumer finance.

Our corporate headquarters is in San Francisco,

but we’re decentralized so all Wells Fargo “con-

venience points”—stores, regional commercial

banking centers, ATMs, Wells Fargo Phone BankSM

centers, internet—are headquarters for satisfy-

ing all our customers’ financial needs

and helping them succeed financially.

Aaa, AAA

Wells Fargo Bank, N.A. is the only bank in the

U.S., and one of only two worldwide, to have

the highest credit rating from both Moody's

Investors Service,“Aaa,” and Standard & Poor's

Ratings Service,“AAA.”

Assets: $482 billion

(5th among U.S. peers)

Market value of stock: $120 billion

(4th among U.S. peers)

Fortune 500: Profit, 17th; Market cap, 18th

Team members: 158,000

(one of U.S.’s 40 largest private employers)

Stores: 6,000+

Reputation

Barron’s

World’s 12th most-admired company

CRO Magazine

Among 50 top corporate citizens

BusinessWeek

Among 10 most generous corporate givers

DiversityInc.

Among top 50 companies for diversity

Forbes

Among top 25 U.S. companies in composite

ranking of revenue, profits, assets and market

value

Fortune

USA’s “Most Admired” Large Bank

KeyNote WebExcellence

No. 2 full-service online broker

Luxury Institute

Among top 10 brands for wealth management

Moody’s Investors Service

S&P Ratings Services

Highest credit ratings (Wells Fargo Bank, N.A.)

Working Mother

Among 100 best companies

Our Market Leadership

#1 retail mortgage originator*

#1 mortgage servicer*

#1 small business lender

#1 small business lender in low-to-

moderate income neighborhoods

#1 insurance broker owned by bank

holding company (world’s 5th-largest insur-

ance broker)

#1 agricultural lender

#1 financial services provider to

middle-market businesses across

our banking states

#1 commercial real estate broker

#2 home equity lender

#2 debit card issuer

#2 bank auto lender

#3 ATM network

#4 deposits

Our Earnings Diversity

historical averages, near future year expectations

* Credit cards,student loans, asset-based lending, equipment finance,

structured finance, correspondent banking, etc.

Community Banking . . . . . . . . . . . . . . . . . . . . . . . . . 33%

Home Mortgage/Home Equity . . . . . . . . . . . . . . . 19%

Investments & Insurance . . . . . . . . . . . . . . . . . . . . . 16%

Specialized Lending* . . . . . . . . . . . . . . . . . . . . . . . . . 16%

Wholesale Banking/Commercial Real Estate . . . . 9%

Consumer Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7%

© 2007 Wells Fargo & Company. All rights reserved.

* Inside Mortgage Finance