Vodafone 2012 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2012 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

124

Vodafone Group Plc

Annual Report 2012

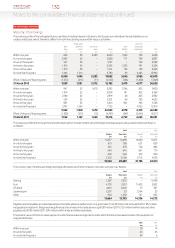

Notes to the consolidated nancial statements (continued)

20. Share-based payments (continued)

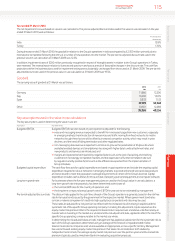

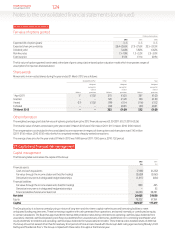

Fair value of options granted

Ordinary share options

2012 2011 2010

Expected life of option (years) 3–5 3–5 3–5

Expected share price volatility 25.4–25.6% 27.5–27.6% 32.5–33.5%

Dividend yield 5.44% 5.82% 6.62%

Risk free rates 1.1–1.9% 1.3–2.2% 2.5–3.0%

Exercise price £1.31 £1.14 £0.94

The fair value of options granted is estimated at the date of grant using a lattice-based option valuation model which incorporates ranges of

assumptions for inputs as disclosed above.

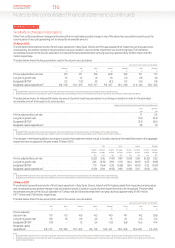

Share awards

Movements in non-vested shares during the year ended 31 March 2012 are as follows:

Global AllShare Plan Other Total

Weighted Weighted Weighted

average fair average fair average fair

value at value at value at

Millions grant date Millions grant date Millions grant date

1 April 2011 17 £1.02 370 £1.00 387 £1.00

Granted – – 120 £1.29 120 £1.29

Vested (17) £1.02 (99) £1.14 (116) £1.12

Forfeited – – (39) £0.81 (39) £0.81

31 March 2012 – – 352 £1.08 352 £1.08

Other information

The weighted average grant date fair value of options granted during the 2012 nancial year was £0.30 (2011: £0.27; 2010: £0.26).

The total fair value of shares vested during the year ended 31 March 2012 was £130million (2011: £113million; 2010: £100million).

The compensation cost included in the consolidated income statement in respect of share options and share plans was £143million

(2011:£156million; 2010: £150million) which is comprised entirely of equity-settled transactions.

The average share price for the year ended 31 March 2012 was 169.9 pence (2011: 159.5 pence, 2010: 132 pence).

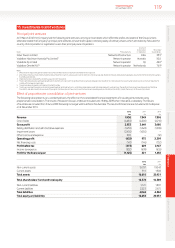

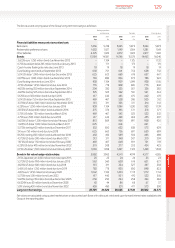

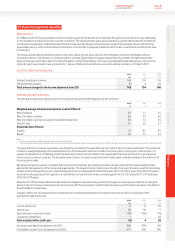

21. Capital and nancial risk management

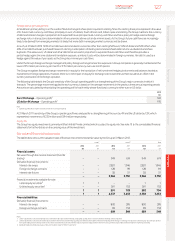

Capital management

The following table summarises the capital of the Group:

2012 2011

£m £m

Financial assets:

Cash and cash equivalents (7,138) (6,252)

Fair value through the income statement (held for trading) (2,629) (2,065)

Derivative instruments in designated hedge relationships (1,317) (654)

Financial liabilities:

Fair value through the income statements (held for trading) 889 495

Derivative instruments in designated hedge relationships – 53

Financial liabilities held at amortised cost 34,620 38,281

Net debt 24,425 29,858

Equity 78,202 87,561

Capital 102,627 117,419

The Group’s policy is to borrow centrally using a mixture of long-term and short-term capital market issues and borrowing facilities to meet

anticipated funding requirements. These borrowings, together with cash generated from operations, are loaned internally or contributed as equity

tocertain subsidiaries. The Board has approved three internal debt protection ratios being: net interest to operating cash ow (plus dividends from

associates); retained cash ow (operating cash ow plus dividends from associates less interest, tax, dividends to non-controlling shareholders and

equity dividends) to net debt; and operating cash ow (plus dividends from associates) to net debt. These internal ratios establish levels of debt that

the Group should not exceed other than for relatively short periods of time and are shared with the Group’s debt rating agencies being Moody’s, Fitch

Ratings and Standard & Poor’s. The Group complied with these ratios throughout the nancial year.