Vodafone 2012 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2012 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

|

|

116

Vodafone Group Plc

Annual Report 2012

Notes to the consolidated nancial statements (continued)

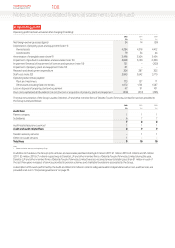

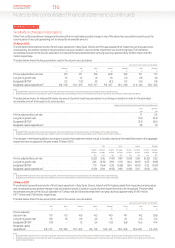

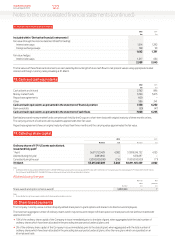

Sensitivity to changes in assumptions

Other than as disclosed below, management believes that no reasonably possible change in any of the above key assumptions would cause the

carrying value of any cash generating unit to exceed its recoverable amount.

31 March 2012

The estimated recoverable amounts of the Group’s operations in Italy, Spain, Greece and Portugal equalled their respective carrying values and,

consequently, any adverse change in key assumption would, in isolation, cause a further impairment loss to be recognised. The estimated

recoverable amounts of the Group’s operations in India and Romania exceeded their carrying values by approximately £2,060 million and £66

million respectively.

The table below shows the key assumptions used in the value in use calculations.

Assumptions used in value in use calculation

Germany Italy Spain Greece Portugal India Romania

%%%%%%%

Pre-tax adjusted discountrate 8.5 12.1 10.6 22.8 16.9 15.1 11.5

Long-term growth rate 1.5 1.2 1.6 1.0 2.3 6.8 3.0

Budgeted EBITDA12.3 (1.2) 3.9 (6.1) 0.2 15.0 0.8

Budgeted capital expenditure2 8.5–11.8 10.1–12.3 10.3–11.7 9.3–12.7 12.5–14.0 11.4–14.4 12.0–14.3

Notes:

1 Budgeted EBITDA is expressed as the compound annual growth rates in the initial ve years for all cash generating units of the plans used for impairment testing.

2 Budgeted capital expenditure is expressed as the range of capital expenditure as a percentage of revenue in the initial ve years for all cash generating units of the plans used for impairment testing.

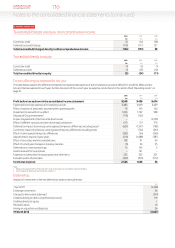

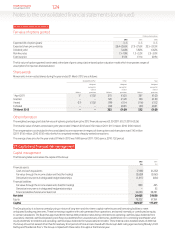

The table below shows, for India and Romania, the amount by which each key assumption must change in isolation in order for the estimated

recoverable amount to be equal to its carrying value.

Change required for carrying value to equal the recoverable amount

India Romania

pps pps

Pre-tax adjusted discount rate 1.1 0.3

Long-term growth rate (1.6) (0.4)

Budgeted EBITDA1(3.3) (0.6)

Budgeted capital expenditure23.6 1.0

Notes:

1 Budgeted EBITDA is expressed as the compound annual growth rates in the initial ve years for all cash generating units of the plans used for impairment testing.

2 Budgeted capital expenditure is expressed as a percentage of revenue in the initial ve years for all the cash generating units of the plans used for impairment testing.

The changes in the following table to assumptions used in the impairment review would, in isolation, lead to an (increase)/decrease to the aggregate

impairment loss recognised in the year ended 31 March 2012:

Italy Spain Greece Portugal

Increase Decrease Increase Decrease Increase Decrease Increase Decrease

by 2pps by 2pps by 2pps by 2pps by 2pps by 2pps by 2pps by 2pps

£bn £bn £bn £bn £bn £bn £bn £bn

Pre-tax adjusted discount rate (2.22) 2.45 (1.42) 0.90 (0.03) 0.06 (0.23) 0.25

Long-term growth rate 2.45 (2.16) 0.90 (1.31) 0.04 (0.01) 0.25 (0.18)

Budgeted EBITDA11.70 (1.64) 0.30 (0.28) 0.04 (0.01) 0.22 (0.20)

Budgeted capital expenditure2(1.00) 0.94 (0.93) 0.90 (0.05) 0.07 (0.13) 0.14

Notes:

1 Budgeted EBITDA is expressed as the compound annual growth rates in the initial ve years for all cash generating units of the plans used for impairment testing.

2 Budgeted capital expenditure is expressed as a percentage of revenue in the initial ve years for all cash generating units of the plans used for impairment testing.

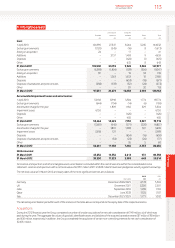

31 March 2011

The estimated recoverable amounts of the Group’s operations in Italy, Spain, Greece, Ireland and Portugal equalled their respective carrying values

and, consequently, any adverse change in key assumptions would, in isolation, cause a further impairment loss to be recognised. The estimated

recoverable amounts of the Group’s operations in Turkey, India and Ghana exceeded their carrying values by approximately £1,481million,

£977million and £138million, respectively.

The table below shows the key assumptions used in the value in use calculations.

Assumptions used in value in use calculation

Italy Spain Greece Ireland Portugal Turkey India Ghana

% % % % % % % %

Pre-tax adjusted

discountrate 11.9 11.5 14.0 14.5 14.0 14.1 14.2 20.8

Long-term growth rate 0.8 1.6 2.0 2.0 1.5 6.1 6.3 6.3

Budgeted EBITDA1(1.0) – 1.2 2.4 (1.2) 16.8 16.5 41.4

Budgeted capital

expenditure29.6–11.3 7.8–10.6 10.7–12.3 9.4–11.6 12.4–14.1 10.0–16.6 12.9–22.7 7.3–41.3

Notes:

1 Budgeted EBITDA is expressed as the compound annual growth rates in the initial ten years for Turkey and Ghana and the initial ve years for all other cash generating units of the plans used for impairment testing.

2 Budgeted capital expenditure is expressed as the range of capital expenditure as a percentage of revenue in the initial ten years for Turkey and Ghana and the initial ve years for all other cash generating units of the plans

used for impairment testing.

10. Impairment (continued)