Vodafone 2006 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2006 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

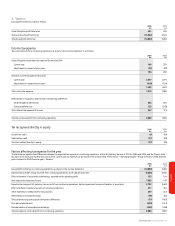

78 Vodafone Group Plc Annual Report 2006

Notes to the Consolidated Financial Statements

continued

levied by the same taxation authority on either the same taxable entity or on different

taxable entities which intend to settle the current tax assets and liabilities on a net basis.

Tax is charged or credited to the income statement, except when it relates to items

charged or credited directly to equity, in which case the tax is also recognised directly

in equity.

Financial instruments

Financial assets and financial liabilities, in respect of financial instruments, are

recognised on the Group’s balance sheet when the Group becomes a party to the

contractual provisions of the instrument.

The Group has applied the requirements of IFRS to financial instruments for all periods

presented and has not taken advantage of any exemptions available to first time

adopters of IFRS in this respect. The Group has early adopted IFRS 7, “Financial

Instruments: Disclosures”, amendments to IAS 39, “Financial Instruments: Recognition

and Measurement” and IFRS 4, “Insurance Contracts”, regarding “Financial Guarantee

Contracts” and amendments to IAS 39 regarding “The Fair Value Option” and “Cash Flow

Hedge Accounting of Forecast Intragroup Transactions” and applied them from 1 April

2004.

Trade receivables

Trade receivables do not carry any interest and are stated at their nominal value as

reduced by appropriate allowances for estimated irrecoverable amounts. Estimated

irrecoverable amounts are based on the ageing of the receivable balances and historical

experience. Individual trade receivables are written off when management deems them

not to be collectible.

Investments

Investments are recognised and derecognised on a trade date where a purchase or sale

of an investment is under a contract whose terms require delivery of the investment

within the timeframe established by the market concerned, and are initially measured at

cost, including transaction costs.

Investments are classified as either held for trading or available-for-sale, and are

measured at subsequent reporting dates at fair value. Where securities are held for

trading purposes, gains and losses arising from changes in fair value are included in net

profit or loss for the period. For available-for-sale investments, gains and losses arising

from changes in fair value are recognised directly in equity, until the security is disposed

of or is determined to be impaired, at which time the cumulative gain or loss previously

recognised in equity, determined using the weighted average costs method, is included

in the net profit or loss for the period.

Cash and cash equivalents

Cash and cash equivalents comprise cash on hand and call deposits, and other short

term highly liquid investments that are readily convertible to a known amount of cash

and are subject to an insignificant risk of changes in value.

Trade payables

Trade payables are not interest bearing and are stated at their nominal value.

Financial liabilities and equity instruments

Financial liabilities and equity instruments issued by the Group are classified according

to the substance of the contractual arrangements entered into and the definitions of a

financial liability and an equity instrument. An equity instrument is any contract that

evidences a residual interest in the assets of the Group after deducting all of its liabilities

and includes no obligation to deliver cash or other financial assets. The accounting

policies adopted for specific financial liabilities and equity instruments are set out below.

Capital market and bank borrowings

Interest bearing loans and overdrafts are initially measured at fair value (which is equal to

cost at inception), and are subsequently measured at amortised cost, using the effective

interest rate method, except where they are identified as a hedged item in a fair value

hedge. Any difference between the proceeds net of transaction costs and the

settlement or redemption of borrowings is recognised over the term of the borrowing.

Equity instruments

Equity instruments issued by the Group are recorded at the proceeds received, net of

direct issue costs.

Derivative financial instruments and hedge accounting

The Group’s activities expose it to the financial risks of changes in foreign exchange rates

and interest rates.

The use of financial derivatives is governed by the Group’s policies approved by the

board of directors, which provide written principles on the use of financial derivatives

consistent with the Group’s risk management strategy. Changes in values of all

derivatives of a financing nature are included within investment income and financing

costs in the income statement. The Group does not use derivative financial instruments

for speculative purposes.

Derivative financial instruments are initially measured at fair value on the contract date,

and are subsequently re-measured to fair value at each reporting date. The Group

designates certain derivatives as either:

•hedges of the change of fair value of recognised assets and liabilities (“fair value

hedges”); or

•hedges of net investments in foreign operations.

Hedge accounting is discontinued when the hedging instrument expires or is sold,

terminated, or exercised, or no longer qualifies for hedge accounting.

Fair value hedges

The Group’s policy is to use derivative instruments (primarily interest rate swaps) to

convert a proportion of its fixed rate debt to floating rates in order to hedge the interest

rate risk arising, principally, from capital market borrowings. The Group designates these

as fair value hedges of interest rate risk with changes in fair value of the hedging

instrument recognised in the income statement for the period together with the

changes in the fair value of the hedged item due to the hedged risk, to the extent the

hedge is effective. The ineffective portion is recognised immediately in the income

statement.

Net investment hedges

Exchange differences arising from the translation of the net investment in foreign

operations are recognised directly in equity. Gains and losses on those hedging

instruments designated as hedges of the net investments in foreign operations are

recognised in equity to the extent that the hedging relationship is effective. These

amounts are included in exchange differences on translation of foreign operations as

stated in the statement of recognised income and expense. Any ineffectiveness is

recognised immediately in the income statement for the period. Gains and losses

accumulated in the translation reserve are included in the income statement when the

foreign operation is disposed of. The Group has adopted the Amendments to IAS 21,

“The Effect of Changes in Foreign Exchange Rates”, with effect from 1 April 2004, being

the date of transition to IFRS for the Group.

Provisions

Provisions are recognised when the Group has a present obligation as a result of a past

event, and it is probable that the Group will be required to settle that obligation.

Provisions are measured at the directors’ best estimate of the expenditure required to

settle the obligation at the balance sheet date, and are discounted to present value

where the effect is material.

Share-based payments

The Group issues equity-settled share-based payments to certain employees. Equity-

settled share-based payments are measured at fair value (excluding the effect of non

market-based vesting conditions) at the date of grant. The fair value determined at the

grant date of the equity-settled share-based payments is expensed on a straight-line

basis over the vesting period, based on the Group’s estimate of the shares that will

eventually vest and adjusted for the effect of non market-based vesting conditions.

Fair value is measured using a binomial pricing model which is calibrated using a Black-

Scholes framework. The expected life used in the model has been adjusted, based on

management’s best estimate, for the effects of non-transferability, exercise restrictions

and behavioural considerations.

Advertising costs

Expenditure on advertising is written off in the year in which it is incurred.

2. Significant accounting policies continued