Vodafone 2006 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2006 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Vodafone Group Plc Annual Report 2006 117

Financials

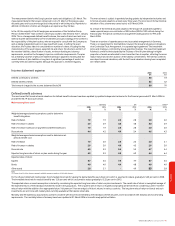

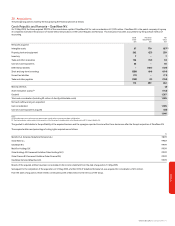

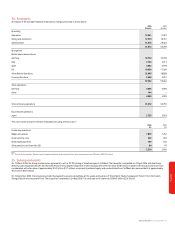

31. Contingent liabilities 2006 2005

£m £m

Performance bonds 189 382

Credit guarantees – third party indebtedness 64 67

Other guarantees and contingent liabilities 19 18

Performance bonds

Performance bonds require the Group to make payments to third parties in the event

that the Group does not perform what is expected of it under the terms of any related

contracts.

Group performance bonds include £152 million (2005: £149 million) in respect of

undertakings to roll out 3G networks in Spain and £nil (2005: £189 million) in respect of

undertakings to roll out 2G and 3G networks in Germany.

Credit guarantees – third party indebtedness

Credit guarantees comprise guarantees and indemnities of bank or other facilities

including those in respect of the Group’s associated undertakings and investments.

Other guarantees and contingent liabilities

Other guarantees principally comprise commitments to support disposed entities.

In addition to the amounts disclosed above, the Group has guaranteed financial

indebtedness and issued performance bonds for £33 million (2005: £36 million) in

respect of businesses which have been sold and for which counter indemnities have

been received from the purchasers.

The Group also enters into lease arrangements in the normal course of business, which

are principally in respect of land, buildings and equipment. Further details on the

minimum lease payments due under non-cancellable operating lease arrangements can

be found in note 30.

Legal proceedings

The Company and its subsidiaries are currently, and may be from time to time, involved

in a number of legal proceedings, including inquiries from or discussions with

governmental authorities, that are incidental to their operations. However, save as

disclosed below, the Company and its subsidiaries are not involved currently in any legal

or arbitration proceedings (including any governmental proceedings which are pending

or known to be contemplated) which may have, or have had in the twelve months

preceding the date of this report, a significant effect on the financial position or

profitability of the Company and its subsidiaries.

The Company is a defendant in four actions in the United States alleging personal injury,

including brain cancer, from mobile phone use. In each case, various other carriers and

mobile phone manufacturers are also named as defendants. These actions are at an

early stage and no accurate quantification of any losses which may arise out of the

claims can therefore be made as at the date of this report. The Company is not aware

that the health risks alleged in such personal injury claims have been substantiated and

will be vigorously defending such claims.

In 2002, a class action lawsuit was brought in the United States District Court for the

Southern District of New York against the Company and certain of its officers and

directors under Sections 10(b) and 20(a) of the Securities Exchange Act of 1934 and

Rule 10b-5 thereunder alleging principally that Vodafone had improperly delayed taking

and disclosing goodwill impairment losses relating to certain fixed line and non-

controlled mobile assets that Vodafone reported in the financial year ended 31 March

2002. Vodafone firmly denied any wrongdoing and believes the allegations are wholly

without merit. On 4 March 2005, the parties entered into a definitive settlement

agreement for a cash payment by Vodafone and its insurance carriers of $24.5 million,

before fees and expenses, which was approved by the Court on 15 July 2005. The

settlement, which covers all current and former defendants, does not involve any

admission or evidence of wrongdoing by any of them. The plaintiffs’ application for

reimbursement of costs and an award of attorneys’ fees to be paid form the settlement

fund remains pending.

A subsidiary of the Company, Vodafone 2, is responding to an enquiry (“the Vodafone 2

enquiry”) by the UK Inland Revenue (now called “Her Majesty’s Revenue and Customs”

and hereinafter referred to as “HMRC”) with regard to the UK tax treatment of its

Luxembourg holding company, Vodafone Investments Luxembourg SARL (“VIL”), under

the Controlled Foreign Companies section of the UK’s Income and Corporation Taxes Act

1988 (“the CFC Regime”) relating to the tax treatment of profits earned by the holding

company for the accounting period ended 31 March 2001. Vodafone 2’s position is that

it is not liable to corporation tax in the UK under the CFC Regime in respect of VIL.

Vodafone 2 asserts, inter alia, that the CFC Regime is contrary to EU law and has made

an application to the Special Commissioners of HMRC for closure of the Vodafone 2

enquiry. On 3 May 2005, the Special Commissioners referred certain questions relating

to the compatability of the CFC Regime with EU law to the European Court of Justice

(the “ECJ”) for determination. Vodafone 2’s application for closure has been stayed

pending delivery of the ECJ’s judgment. In its judgement, the ECJ will only determine

questions referred to it and does not have jurisdiction to determine the outcome of

Vodafone 2’s application. Instead, the Special Commissioners will apply the ECJ’s

judgement to the particular facts of Vodafone 2’s application. Although it is not possible

to address all possible outcomes, it should be noted that even if the CFC Regime is held

by the ECJ to be entirely lawful, Vodafone 2 would continue to resist the imposition of

corporation tax liability on other grounds. On 15 June 2005, HMRC appealed to the High

Court challenging the Special Commissioners’ decision to refer questions to the ECJ.

This appeal was dismissed and HMRC has since appealed this dismissal to the Court of

Appeal. A decision in the latter appeal is expected to be rendered in the second half of

2006. In addition to the Vodafone 2 enquiry, on 31 October 2005, HMRC commenced an

enquiry into the residence of VIL which is ongoing (the “VIL enquiry”). VIL’s position is

that it is resident for tax purposes solely in Luxembourg and therefore it is not liable for

corporation tax in the UK. The Company has taken provisions, which at 31 March 2006

amounted to £2,098 million, for the potential UK corporation tax liability and related

interest expense that may arise in connection with the Vodafone 2 and VIL enquiries, if

the Company is not successful in its challenge of the CFC Regime. The provisions relate

to the accounting period which is the subject of the proceedings described above as

well as to accounting periods after 31 March 2001 to date.

The judgement of the ECJ is expected to be delivered at the beginning of 2007 at the

earliest. In the absence of any material unexpected developments, the provisions are

likely to be reassessed when the views of the ECJ become known.