Vodafone 2006 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2006 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

106 Vodafone Group Plc Annual Report 2006

Notes to the Consolidated Financial Statements

continued

24. Borrowings continued

Financial risk management

The Group’s treasury function provides a centralised service to the Group for funding,

foreign exchange, interest rate management and counterparty risk management.

Treasury operations are conducted within a framework of policies and guidelines

authorised and reviewed annually by the Company’s Board of directors, most recently on

31 January 2006. A Treasury Risk Committee, comprising of the Group’s Chief Financial

Officer, Group General Counsel and Company Secretary, Group Treasurer and Director of

Financial Reporting, meets quarterly to review treasury activities and management

information relating to treasury activities. In accordance with the Group treasury policy, a

quorum for meetings is four members and either the Chief Financial Officer or Group

General Counsel and Company Secretary must be present at each meeting. The Group

accounting function, which does not report to the Group Treasurer, provides regular

update reports of treasury activity to the Board of directors. The Group uses a number of

derivative instruments that are transacted, for risk management purposes only, by

specialist treasury personnel. The Group’s internal auditors review the internal control

environment regularly. There has been no significant change during the financial year, or

since the end of the year, to the types of financial risks faced by the Group or the Group’s

approach to the management of those risks.

The Group’s policy is to borrow centrally, using a mixture of long term and short term

capital market issues and borrowing facilities, to meet anticipated funding requirements.

These borrowings, together with cash generated from operations, are on-lent or

contributed as equity to certain subsidiaries. The Board of directors has approved three

debt protection ratios, being: net interest to operating cash flow (plus dividends from

associated undertakings); retained cash flow (operating cash flow plus dividends from

associated undertakings less interest, tax, dividends to minorities and equity dividends)

to net debt; and operating cash flow (plus dividends from associated undertakings) to

net debt.

These internal ratios establish levels of debt that the Group should not exceed other

than for relatively short periods of time and are shared with the Group’s debt rating

agencies, being Moody’s, Fitch Ratings and Standard & Poor’s.

Liquidity risk

As at 31 March 2006, the Group had $10.9 billion committed undrawn bank facilities and

$15 billion and £5 billion commercial paper programmes, that are supported by the

$10.9 billion committed bank facilities, available to manage its liquidity.

Market risk

Interest rate management

Under the Group’s interest rate management policy, interest rates on monetary assets

and liabilities are maintained on a floating rate basis, unless the forecast interest charge

for the next eighteen months is material in relation to forecast results, in which case

rates are fixed. In addition, fixing is undertaken for longer periods when interest rates are

statistically low.

At 31 March 2006, 29% (2005: 31%) of the Group’s gross borrowings were fixed for a

period of at least one year. A one hundred basis point fall or rise in market interest rates

for all currencies in which the Group had borrowings at 31 March 2006 would increase or

reduce profit before tax by approximately £91 million, including mark-to-market

revaluations of interest rate and other derivatives and the potential interest on

outstanding tax issues.

Foreign exchange management

As Vodafone’s primary listing is on the London Stock Exchange, its share price is quoted

in sterling. Since the sterling share price represents the value of its future multi-currency

cash flows, principally in euro, yen (until disposal of its Japan operation on 27 April

2006), sterling and US dollars, the Group has a policy to hedge external foreign

exchange risks on transactions denominated in other currencies above certain de

minimis levels.

The Group also maintains the currency of debt and interest charges in proportion with

its expected future principal multi-currency cash flows. As such, at 31 March 2006,113%

of net debt was denominated in currencies other than sterling (73% euro, 21% yen, 14%

US dollar and 5% other), whilst 13% of net debt had been purchased forward in sterling

in anticipation of sterling denominated shareholder returns via share purchases,

dividends and B share distribution. This allows debt to be serviced in proportion to

expected future cash flows and, therefore, provides a partial hedge against income

statement translation exposure, as interest costs will be denominated in foreign

currencies. A relative weakening in the value of sterling against certain currencies in

which the Group maintains debt has resulted in an increase in net debt of £182 million

from currency translation differences.

When the Group’s international net earnings for the year ended 31 March 2006 are

retranslated assuming a 10% strengthening of sterling against all exchange rates, the

operating profit for the year would have increased by £1,344 million (2005: reduced by

£645 million), and would have been reduced by £1,642 million (2005: increased by

£789 million) if sterling weakened by 10%.

The change in equity due to a 10% fall or rise in sterling rates against all exchange rates

for the translation of net investment hedging instruments would be a decrease of

£1,669 million or an increase of £1,365 million. However, there would be no net impact

on equity as there would be an offset in the currency translation of the foreign

operation.

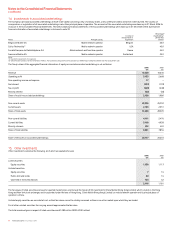

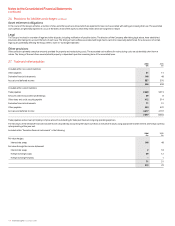

Credit risk

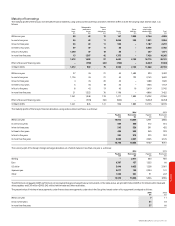

The Group considers its maximum exposure to credit risk to be as follows:

2006 2005

£m £m

Bank deposits 948 343

Money market fund investments 1,841 2,708

Commercial paper investments –512

Repurchase agreements –206

Derivative financial instruments 310 408

3,099 4,177

Concentrations of credit risk with respect to trade receivables are limited due to the

Group's customer base being large and unrelated. Due to this, management believes

there is no further credit risk provision required in excess of the normal provision for bad

and doubtful receivables (note 17).

The deposits shown in the table equate to the principal of the amount deposited. The

foreign exchange transactions and interest rate swaps shown in the table have been

marked-to-market.

For repurchase agreements, collateral equivalent to the investment value is satisfied by

triple-A rated government and/or supranational instruments and collateral is

replenished on a daily basis. In respect of financial instruments used by the Group’s

treasury function, the aggregate credit risk the Group may have with one counterparty is

limited by reference to the long term credit ratings assigned for that counterparty by

Moody’s, Fitch Ratings and Standard & Poor’s. While these counterparties may expose

the Group to credit losses in the event of non-performance, it considers the possibility of

material loss to be acceptable because of this policy.

Consistent with development of its strategy, the Group is now targeting low single A long

term credit ratings from Moody’s, Fitch Ratings and Standard & Poor’s having previously

managed the capital structure at single A credit ratings. Credit ratings are not a

recommendation to purchase, hold or sell securities, in as much as ratings do not

comment on market price or suitability for a particular investor, and are subject to

revision or withdrawal at any time by the assigning rating organisation. Each rating

should be evaluated independently.

25. Post employment benefits

Background

As at 31 March 2006, the Group operated a number of pension plans for the benefit of

its employees throughout the world, which vary depending on the conditions and

practices in the countries concerned. The Group's pension plans are provided through

both defined benefit and defined contribution arrangements. Defined benefit schemes

provide benefits based on the employees' length of pensionable service and their final

pensionable salary or other criteria. Defined contribution schemes offer employees

individual funds that are converted into benefits at the time of retirement.

The principal defined benefit pension schemes are in the United Kingdom and Germany.

The Group also operated defined benefit schemes in Japan, its discontinued operation,

and in Sweden until it was disposed of on 5 January 2006. In addition, the Group

operates defined benefit schemes in Greece, Ireland, Italy and the United States. Defined

contribution pension schemes are provided in Australia, Belgium, Egypt, Germany,

Greece, Hungary, Ireland, Italy, Malta, the Netherlands, New Zealand, Portugal, Spain, the

United Kingdom and the United States. A defined contribution scheme is also operated

in the Group’s discontinued operation in Japan. There is a post retirement medical plan

in the United States for a small closed group of participants.

The Group accounts for its pension schemes in accordance with IAS 19, Employee Benefits

(“IAS19”). The Group has also early adopted the amendment to IAS 19 that was published

in December 2004 regarding actuarial gains and losses, group plans and disclosures.

Scheme liabilities are assessed by independent actuaries using the projected unit

funding method and applying the principal actuarial assumptions set out below. Assets

are shown at market value.