Reebok 2006 Annual Report Download - page 168

Download and view the complete annual report

Please find page 168 of the 2006 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

|

|

Consolidated Financial Statements ›

164 ANNUAL REPORT 2006 › adidas Group ›

The actuarial valuations of the defined benefit plans are made at the end of each reporting

period. The assumptions for employee turnover and mortality are based on empirical data, the

latter for Germany on the 2005 version of the mortality tables of Dr. Heubeck. The actuarial

assumptions in Germany and in other countries are not materially different.

As of January 1, 2005, due to application of the amendment to IAS 19 “Employee Benefits”

issued in December 2004, the Group recognizes actuarial gains or losses of defined benefit

plans arising during the financial year immediately outside the income statement in the state-

ment of recognized income and earnings (SoRIE). The actuarial gain (loss) recognized in the

statement of recognized income and expense for 2006 was € 2 million (2005: € 14 million) The

cumulative recognized actuarial losses amount to € 30 million (2005: € 31 million) (see also

Note 22).

Of the total pension expenses, an amount of € 7 million (2005: € 11 million) relates to em-

ployees in Germany. Contributions to post-employment benefit plans for employees living in

Germany for the year ending December 31, 2007, are expected to amount to € 11 million. The

pension expense is recorded within the operating expenses whereas the production-related

part thereof is recognized within the cost of sales.

The calculations of the recognized assets and liabilities from defined benefit plans are based

upon statistical and actuarial calculations. In particular, the present value of the defined ben-

efit obligation is impacted by assumptions on discount rates used to arrive at the present

value of future pension liabilities and assumptions on future increases in salaries and benefits.

Furthermore, the Group’s independent actuaries use statistically based assumptions cover-

ing areas such as future participant plan withdrawals and estimates on life expectancy. The

actuarial assumptions used may differ materially from actual results due to changes in market

and economic conditions, higher or lower withdrawal rates or longer or shorter life spans of

participants and other changes in the factors being assessed. These differences could impact

the assets or liabilities recognized in the balance sheet in future periods.

The plan assets are invested in several pension funds. The return on plan assets is in confor-

mity with the current strategy of the pension funds. In 2006, the actual return on plan assets

was € 2 million.

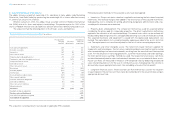

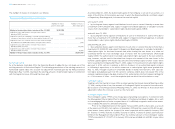

Pension Expenses € in millions

Year ending Dec. 31

2006 2005

Current service cost 7 9

Interest cost 5 5

Expected return on plan assets (1) —

Pension expenses 11 14

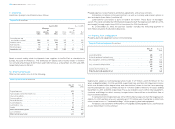

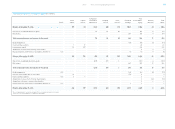

Defined Benefit Obligation € in millions

2006

Defined benefit obligation as at January 1 131

Increase in companies consolidated 34

Currency translation differences 1

Current service cost 7

Interest cost 5

Pensions paid (6)

Actuarial loss in 2006 (2)

Defined benefit obligation as at December 31 170

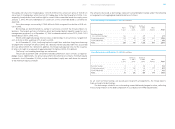

Status of Funded and Unfunded Obligations € in millions

Dec. 31 Dec. 31

2006 2005

Present value of unfunded obligation 110 131

Present value of funded obligation 60 —

Present value of total obligations 170 131

Fair value of plan assets (44)1) —

Recognized Liability for defined benefit obligations 126 131

1) Part of the € 46 million total of plan assets cannot be deducted, as it is not possible to use the exceeding amount for another plan.

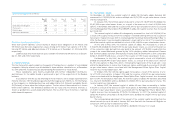

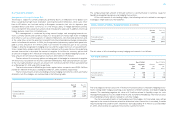

Movement in Plan Assets € in millions

2006

Fair value of plan assets at January 1 —

Increase in companies consolidated 25

Contributions paid into the plan 20

Expected return on plan assets 1

Fair value of plan assets at December 31 46