Reebok 2006 Annual Report Download - page 160

Download and view the complete annual report

Please find page 160 of the 2006 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

|

|

Consolidated Financial Statements ›

156 ANNUAL REPORT 2006 › adidas Group ›

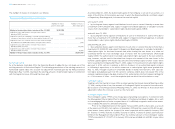

5 » Acquisition/Disposal of Subsidiaries

The adidas Group assumed full ownership of its subsidiary in India, adidas India Marketing

Private Ltd., New Delhi (India), by purchasing the remaining 8.6% of shares effective January

17, 2006 for an amount of € 2 million.

Effective January 31, 2006, the adidas Group assumed control of Reebok International

Ltd. (USA), with all its direct and indirect shareholdings. The purchase price for 100% of the

shares of Reebok International Ltd. (USA) was US $ 3.6 billion (€ 3.0 billion), fully paid in cash.

The acquisition had the following effect on the Group’s assets and liabilities:

Pre-acquisition carrying amounts were based on applicable IFRS standards.

Following valuation methods for the acquired assets have been applied:

» Inventories: The pro rata basis valuation is applied for estimating the fair value of acquired

inventories. The realized margins were added to the book values of the acquired inventories.

Subsequently, cost to complete for selling, advertising and general administration and a rea-

sonable profit allowance were deducted.

» Property, plant and equipment: The comparison method was used for acquired land by

considering the prices paid for comparable properties. The direct capitalization method was

applied for the valuation of all acquired buildings. The annual rents which can be realized will

be adjusted by deducting risk factors and applicable operating costs and are finally discounted.

The acquired machinery and equipment is valued with the depreciated replacement cost

method. The replacement costs are determined by applying an index to the asset’s historical

cost. The replacement costs are then adjusted for the loss in value caused by depreciation.

» Trademarks and other intangible assets: The relief-from-royalty method is applied for

trademarks and technologies. The fair value is determined by discounting the royalty savings

after tax and adding a tax amortization benefit, resulting from the amortization of the acquired

asset. For the valuation of licensing agreements, customer relationships and order backlogs,

the multi-period-excess-earnings method was used. The respective future excess cash flows

are identified and adjusted in order to eliminate all elements not associated with these assets.

Future cash flows are measured on the basis of the expected sales by deducting variable and

sales-related imputed costs for the use of contributory assets. Subsequently, the outcome is

discounted using an appropriate discount rate and adding a tax amortization benefit.

» Long-term financial assets: The discounted cash flow method was used for the valuation

of a participation. Future free cash flows were discounted back to the valuation date using an

appropriate discount rate.

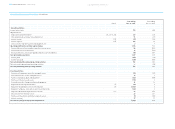

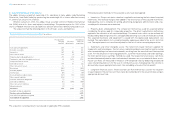

Reebok’s Net Assets at the Acquisition Date € in millions

Pre-aquisition Recognized

carrying Fair value values on

amounts adjustments acquisition

Cash and cash equivalents 539 — 539

Accounts receivable 453 — 453

Inventories 447 55 502

Other current assets 103 (3) 100

Property, plant and equipment, net 293 (33) 260

Trademarks and other intangible assets, net 68 1,674 1,742

Long-term financial assets — 4 4

Deferred tax assets 198 44 242

Other non-current assets 16 — 16

Borrowings (506) — (506)

Accounts payable (109) — (109)

Income taxes (59) — (59)

Accrued liabilities and provisions (329) (30) (359)

Other current liabilities (418) — (418)

Pensions and similar obligations (7) — (7)

Deferred tax liabilities (11) (578) (589)

Other non-current liabilities (2) — (2)

Minority interests (3) — (3)

Net assets 673 1,133 1,806

Goodwill arising on acquisition 1,165

Purchase price settled in cash 2,971

Cash and cash equivalents acquired 539

Cash outflow on acquisition 2,432