Reebok 2006 Annual Report Download - page 156

Download and view the complete annual report

Please find page 156 of the 2006 Reebok annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

|

|

Consolidated Financial Statements ›

152 ANNUAL REPORT 2006 › adidas Group ›

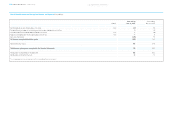

Irrespective of whether there is an indication of impairment, intangible assets with an

indefinite useful life and goodwill acquired in business combinations are tested annually for

impairment.

An impairment loss recognized for goodwill is not reversed. In respect of other assets,

an impairment loss recognized in prior periods is reversed if there has been a change in the

estimates used to determine the recoverable amount. An impairment loss is reversed only to

the extent that the asset’s carrying amount does not exceed the carrying amount that would

have been determined (net of depreciation or amortization) if no impairment loss had been

recognized.

Finance Leases

If under a lease agreement substantially all risks and rewards associated with an asset are

transferred to the Group, the asset less accumulated depreciation and the corresponding

liability are recognized at the fair value of the asset or the lower net present value of the mini-

mum lease payments. Minimum lease payments are apportioned between the finance charge

and the reduction of the outstanding liability. The finance expense is allocated to each period

during the lease term so as to produce a constant periodic rate of interest on the remaining

balance of the liability.

Identifiable Intangible Assets

Acquired intangible assets are valued at cost less accumulated amortization and impairment

losses. Amortization is calculated on a straight-line basis with the following useful lives:

In 2006, the adidas Group determined that there was no impairment necessary for any of its

trademarks with indefinite useful lives.

The recoverable amount is determined on the basis of fair value less costs to sell, which

are calculated with 1% of the fair value. The fair value is determined in discounting the royalty

savings after tax and adding a tax amortization benefit, resulting from the amortization of

the acquired asset (relief-from-royalty method). These calculations use projections of royalty

savings based on the financial planning covering a maximum period of five years in total. Roy-

alty savings beyond this period are extrapolated using steady growth rates of around 2%. The

growth rates do not exceed the long-term average growth rate of the business in which the

trademarks are allocated.

The discount rate is based on a weighted average cost of capital calculation consider-

ing the debt/equity structure and financing costs of the major competitors. The discount rate

used is after-tax rates and reflects specific equity and country risk. The applied discount rate

is 7.5%.

Expenditures for internally generated intangible assets are expensed as incurred if they

do not qualify for recognition.

Goodwill

Goodwill is the excess of the purchase cost over the fair value of acquired identifiable assets

and liabilities. Goodwill arising from the acquisition of a foreign entity and any fair value ad-

justments to the carrying amounts of assets and liabilities of that foreign entity are treated

as assets of the reporting entity and are translated at exchange rates prevailing at the date of

the initial consolidation. Goodwill is carried in the functional currency of the acquired foreign

entity.

Acquired goodwill is valued at cost less accumulated impairment losses. From January 1,

2005, scheduled amortization of goodwill ceased. Goodwill is tested annually for impairment,

and additionally when there are indications of potential impairment.

Goodwill has been allocated for impairment testing purposes to three cash-generating

units. The Group’s cash-generating units are identified according to brand of operations (in the

prior year according to brands and regions) in line with the internal management approach.

The adidas Group has thus defined the three segments adidas, Reebok and TaylorMade-adidas

Golf as the relevant cash-generating units.

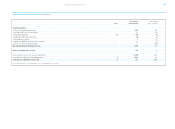

Useful Lives of Identifiable Intangible Assets

Years

Trademarks indefinite

Patents, trademarks and concessions 5 – 15

Software 3 – 5