Chrysler 2005 Annual Report Download - page 266

Download and view the complete annual report

Please find page 266 of the 2005 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

256 -

257

257 -

258

258 -

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

-

278

|

|

265

Reports of the Board of Statutory Auditors

After studying in detail the allegations put forth by the complainant

and reviewing the complaints both individually and as a whole, we

concluded that the portions of the complaints that contain general

criticisms of the Company’s management practices do not identify

improper acts, such as those specifically referred to in Article 2408 of

the Italian Civil Code. Earlier in this report, we already discussed the

soundness of the Company’s management decisions, insofar as they

apply to those areas that fall under our jurisdiction pursuant to

Article 149, Section 1, of Legislative Decree No. 58 of February 24,

1998.

These matters are not reprehensible but instead involve requests

for information. In response, we can affirm that:

in regard to point a) hereinabove, the northwest area of the

Mirafiori plant was sold by the indirect subsidiary Fiat Auto S.p.A.

to Torino Nuova Economia S.p.A., pursuant to an agreement under

the hand and seal of the notary public Ganelli on December 23,

2005, Notary’s Register no. 5462, at a price of 60,000,000 euros

for a total area of 300,393 square meters. The value of the sold

lots was appraised by Prof. Riccardo Ruscelli (Turin Polytechnic

University), who was retained by the Public Entities, and by REAG

S.p.A., a company belonging to the American Appraisal Group,

which was retained by Fiat Auto S.p.A.;

in regard to point b), the complainant does not identify improper

acts, but asks the Board of Statutory Auditors to seek such acts

by auditing the allocation of restructuring costs affecting the entire

group, and thus the consolidated financial statements, which are

subject to audit by the external auditors pursuant to Article 41

no. 3 of Legislative Decree no. 127 of April 9, 1991. To complete

our investigation, we contacted Deloitte & Touche S.p.A., which had

been informed of the requests after receiving the complaint itself.

This firm informed us:

– “In the consolidated financial statements of Fiat at December 31,

2004, which were drafted in compliance with Group accounting

principles that conformed with the requirements of Legislative

Decree no. 127 of April 9, 1991, interpreted and supplemented by

the accounting principles issued by the National boards of “Dottori

Commercialisti e dei Ragionieri” and, where there were none and

not at variance, by those laid down by the International Accounting

Standards Board (IASB), the valuation principle applied for

accounting of reserves for current restructuring was described in

the notes to the consolidated financial statements in the section

“Principles of Consolidation and Significant Accounting Policies,”

at the subsection “Reserves for risks and charges and employee

severance indemnities.” The notes to the consolidated financial

statements specifically showed how the costs to carry out corporate

reorganization and restructuring plans were “provided in the year

the company formally decided to commence such plans and the

relative costs could be reasonably estimated.”

– In the Fiat Group consolidated financial statements at December

31, 2005, which were prepared in compliance with the International

Financial Reporting Standards (IFRS) issued by the International

Accounting Standards Board and approved by the European Union,

the valuation principle applied to restructuring costs is described in

the section entitled “Significant Accounting Policies,” at the subsection

“Provisions.” The notes to the consolidated financial statements

specifically state that “the Group records provisions when it has an

obligation, legal or constructive, to a third party, when it is probable

that an outflow of Group resources will be required to satisfy the

obligation and when a reliable estimate of the amount can be

made.”

Based on the audits we performed in those areas that fall under our

jurisdiction pursuant to Article 149 of Legislative Decree No. 58 of

February 24, 1998 and the information received from the External

Auditors, we have verified that the statutory financial statements,

which show a net income of 223,019,671 euros, compared with a

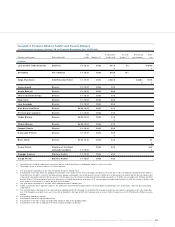

net loss of 949,100,522 euros in the previous fiscal year, have been

prepared and presented in accordance with the applicable provisions

of law.

Therefore, we recommend that you approve them as they have been

submitted to you, together with the motion put forward by the

Board to allocate the net income of 223,019,671 euros to partially

cover the losses carried forward.

We take this opportunity to thank you for your confidence and

to inform you that our term of office has expired.

Turin, April 6, 2006

The Statutory Auditors

Cesare Ferrero

Giuseppe Camosci

Giorgio Ferrino