Capital One 2005 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

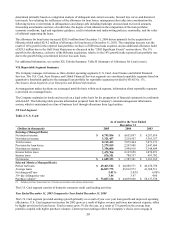

Foreign Exchange Risk

The Company is exposed to changes in foreign exchange rates which may impact translated income and expense associated

with foreign operations. In order to limit earnings exposure to foreign exchange risk, the Company’ s Asset/Liability

Management Policy requires that material foreign currency denominated transactions be hedged. As of December 31, 2005,

the estimated reduction in 12-month earnings due to adverse foreign exchange rate movements corresponding to a 95%

probability is less than 1%. The precision of this estimate is also limited due to the inherent uncertainty of the underlying

recast assumptions. fo

X

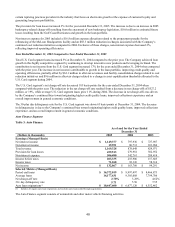

. Capital

Capital Adequacy

The Company and the Bank are subject to capital adequacy guidelines adopted by the Federal Reserve Board (the “Federal

Reserve”) while the Savings Bank is subject to capital adequacy guidelines adopted by the Office of Thrift Supervision (the

“OTS”) and the National Bank is subject to capital adequacy guidelines adopted by the Office of the Comptroller of the

Currency (the “OCC”) (collectively, the “regulators”). The capital adequacy guidelines require the Company, the Bank, the

Savings Bank and the National Bank to maintain specific capital levels based upon quantitative measures of their assets,

liabilities and off-balance sheet items. In addition, the Bank, Savings Bank and National Bank must also adhere to the

regulatory framework for prompt corrective action.

The most recent notifications received from the regulators categorized the Bank, the Savings Bank and the National Bank as

“well-capitalized.” As of December 31, 2005, the Company’ s, the Bank’ s, the Savings Bank’ s and the National Bank’ s

capital exceeded all minimum regulatory requirements to which they were subject, and there were no conditions or events

since the notifications discussed above that management believes would have changed either the Company, the Bank, the

Savings Bank’ s or the National Bank’ s capital category.

The Bank and Savings Bank treat a portion of their loans as “subprime” under the “Expanded Guidance for Subprime

Lending Programs” (the “Subprime Guidelines”) issued by the four federal banking agencies that comprise the Federal

Financial Institutions Examination Council (“FFIEC”), and have assessed their capital and allowance for loan losses

accordingly. Under the Subprime Guidelines, the Bank and Savings Bank each exceed the minimum capital adequacy

guidelines as of December 31, 2005. Failure to meet minimum capital requirements can result in mandatory and possible

additional discretionary actions by the regulators that, if undertaken, could have a material effect on the Company’ s

consolidated financial statements.

For purposes of the Subprime Guidelines, the Company has treated as subprime all loans in the Bank’ s and the Savings

Bank’ s targeted “subprime” programs to customers either with a FICO score of 660 or below or with no FICO score. The

Bank and the Savings Bank hold on average 200% of the total risk-based capital charge that would otherwise apply to such

assets. This results in higher levels of regulatory capital at the Bank and the Savings Bank.

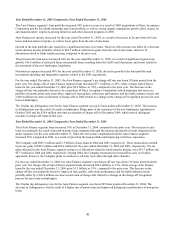

Additionally, regulatory restrictions exist that limit the ability of the Bank, Savings Bank and National Bank to transfer funds

to the Corporation. As of December 31, 2005, retained earnings of the Bank, the Savings Bank and the National Bank of

$464.1 million, $377.2 million and $30.3 million, respectively, were available for payment of dividends to the Corporation

ithout prior approval by the regulators. w

Supplementary Data—Notes to the Consolidated Financial Statements—Note 18”.

Dividend Policy

Although the Company expects to reinvest a substantial portion of its earnings in its business, the Company also intends to

continue to pay regular quarterly cash dividends on its common stock. The declaration and payment of dividends, as well as

the amount thereof, are subject to the discretion of the Board of Directors of the Company and will depend upon the

Company’ s results of operations, financial condition, cash requirements, future prospects and other factors deemed relevant

by the Board of Directors. Accordingly, there can be no assurance that the Corporation will declare and pay any dividends.

As a holding company, the ability of the Corporation to pay dividends is dependent upon the receipt of dividends or other

payments from its subsidiaries. Applicable banking regulations and provisions that may be contained in borrowing

agreements of the Corporation or its subsidiaries may restrict the ability of the Corporation’ s subsidiaries to pay dividends to

the Corporation or the ability of the Corporation to pay dividends to its stockholders.

49

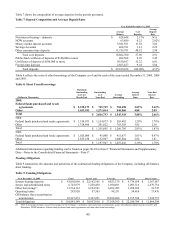

Additional information regarding capital adequacy can be found on pages 90-92 in Item 8 “Financial Statements and