Capital One 2005 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

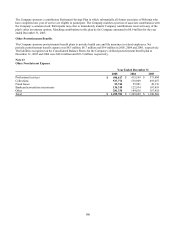

|

|

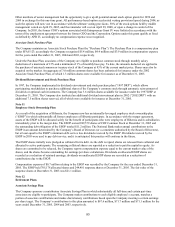

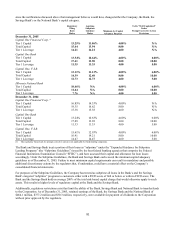

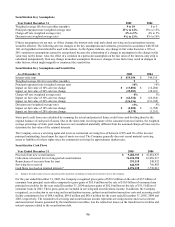

since the notifications discussed above that management believes would have changed either the Company, the Bank, the

avings Bank’ s or the National Bank’ s capital category. S

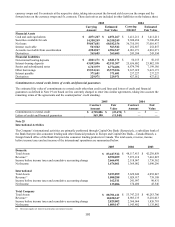

Regulatory

Filing

Basis

Ratios

Applying

Subprime

Guidance

Ratios Minimum for Capital

Adequacy Purposes

To Be “Well Capitalized”

Under

Prompt Corrective Action

Provisions

December 31, 2005

Capital One Financial Corp. (1)

Tier 1 Capital 13.25% 11.86% 4.00% N/A

Total Capital 15.44 13.94 8.00 N/A

Tier 1 Leverage 14.21 14.21 4.00 N/A

Capital One Bank

Tier 1 Capital 13.54% 10.64% 4.00% 6.00%

Total Capital 17.41 13.90 8.00 10.00

Tier 1 Leverage 11.35 11.35 4.00 5.00

Capital One, F.S.B.

Tier 1 Capital 13.11% 11.13% 4.00% 6.00%

Total Capital 14.39 12.40 8.00 10.00

Tier 1 Leverage 12.73 12.73 4.00 5.00

Hibernia National Bank

Tier 1 Capital 10.46% N/A 4.00% 6.00%

Total Capital 11.64 N/A 8.00 10.00

Tier 1 Leverage 7.76 N/A 4.00 5.00

December 31, 2004

Capital One Financial Corp. (1)

Tier 1 Capital 16.85% 14.33% 4.00% N/A

Total Capital 19.35 16.62 8.00 N/A

Tier 1 Leverage 15.38 15.38 4.00 N/A

Capital One Bank

13.24%

10.63%

4.00%

6.00%Tier 1 Capital

Total Capital 17.09 13.92 8.00 10.00

Tier 1 Leverage 11.33 11.33 4.00 5.00

Capital One, F.S.B.

Tier 1 Capital 15.61% 12.93% 4.00% 6.00%

Total Capital 16.91 14.21 8.00 10.00

Tier 1 Leverage 14.47 14.47 4.00 5.00

(1

) The regulatory framework for prompt corrective action is not applicable for bank holding companies.

The Bank and Savings Bank treat a portion of their loans as “subprime” under the “Expanded Guidance for Subprime

Lending Programs” (the “Subprime Guidelines”) issued by the four federal banking agencies that comprise the Federal

Financial Institutions Examination Council (“FFIEC”), and have assessed their capital and allowance for loan losses

accordingly. Under the Subprime Guidelines, the Bank and Savings Bank each exceed the minimum capital adequacy

guidelines as of December 31, 2005. Failure to meet minimum capital requirements can result in mandatory and possible

additional discretionary actions by the regulators that, if undertaken, could have a material effect on the Company’ s

consolidated financial statements.

For purposes of the Subprime Guidelines, the Company has treated as subprime all loans in the Bank’ s and the Savings

Bank’ s targeted “subprime” programs to customers either with a FICO score of 660 or below or with no FICO score. The

Bank and the Savings Bank hold on average 200% of the total risk-based capital charge that would otherwise apply to such

ssets. This results in higher levels of regulatory capital at the Bank and the Savings Bank. a

Additionally, regulatory restrictions exist that limit the ability of the Bank, Savings Bank and National Bank to transfer funds

to the Corporation. As of December 31, 2005, retained earnings of the Bank, the Savings Bank and the National Bank of

$464.1 million, $377.2 million and $30.3 million, respectively, were available for payment of dividends to the Corporation

without prior approval by the regulators.

91