Capital One 2005 Annual Report Download - page 2

Download and view the complete annual report

Please find page 2 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

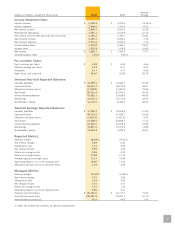

2005 was a transformational year for Capital One. Two years ago, we announced our intention to buy a bank. In

November of 2005, we made banking a reality at Capital One with the acquisition of Hibernia. Our diversification

strategy continued to drive strong results. We delivered our 11th straight year of record earnings with diluted earnings

per share of $6.73. Asset growth was strong, with managed loans increasing 32% to $106 billion in 2005, including

Hibernia. Our balance sheet remained solid and diversified with $47.9 billion of total deposits, exceptional liquidity,

and more than half of our managed loans now in businesses beyond U.S. credit cards. We also continued to see stellar

credit performance with managed charge-offs of 4.25%.

We’re Delivering On Our Strategy

At Capital One, we believe that the essence of strategy is figuring out where the world is going and then working backwards

from that vision to position our company to win. Here’s where we believe the world of consumer banking is going.

Consumer lending businesses, like credit cards and home equity, used to be dominated by the local branch on the

corner. However, the ability to win in these markets is increasingly dependent on having national marketing capabilities,

a national customer base, a national brand, and the efficiencies that go along with national scale. Consumer lending

businesses are consolidating nationally at a rapid pace. A handful of big players ultimately will emerge as winners as

these businesses continue to consolidate one product at a time.

Certain banking businesses, like deposits and parts of small business, remain steadfastly local in nature. Success in these

businesses is not driven by national scale. Instead, banks with a sizeable share in their local markets tend to disproportionately

win in those businesses.

We believe that the winners in consumer banking will be the nationally branded players who bring together the best

of national scale lending and local scale banking. However, while banks are focused on consolidation, few are directly

pursuing our vision of the end game. Monolines specializing in a single lending product generally are focused on building

bigger and bigger versions of themselves, but they’re not diversifying. Regional banks typically are focused on expanding

geographically, but they’re not building national scale lending platforms in the process. The largest national banks have

both national and local scale, but often tend to take a national approach to competing in their local businesses. Only

a handful of banks are building a national brand.

We’ve been focused on the inevitable transformation of consumer banking since we began building our credit card

business in 1988. We chose to enter the credit card business because we believed that it was at the forefront of this

transformation. We thought that, using the power of information, technology and testing, we could build a winning

national scale business as the credit card business consolidated.

We believed that we could export the capabilities that we built in credit cards to other consumer lending businesses

as they eventually followed a similar path. Our vision was to acquire or build growth platforms in key consumer lending

businesses to capitalize on future waves of consolidation. Seven years ago, we started down the diversification path in

the United States with our move into auto finance. We’ve also created national scale growth platforms in small business

lending, home equity, installment lending and other emerging lending businesses, as well as diversifying internationally

in the United Kingdom and Canada.

CHAIRMAN’S LETTER TO SHAREHOLDERS AND FRIENDS

- 1 -

We’re delivering on our strategy

of combining the power of

national scale lending and local

scale banking.

“

”