Capital One 2005 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

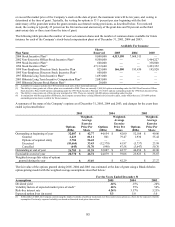

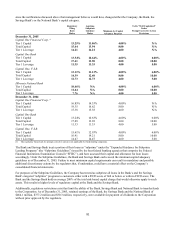

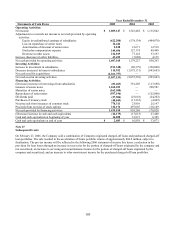

unding Commitments Related to Synthetic Fuel Tax Credit Transactions F

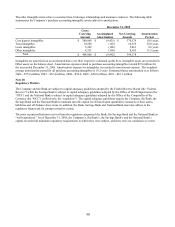

In June of 2004 and July of 2005, the Company, through two separate transactions and two consolidated special purpose

entities (SPVs), purchased minority ownership interests in two entities established to operate facilities which produce a coal-

based synthetic fuel that qualifies for tax credits pursuant to Section 29 of the Internal Revenue Code. The SPVs purchased

their minority interests from third parties paying $2.6 million in cash and agreeing to pay an estimated $159.1 million

comprised of fixed note payments, variable payments and the funding of their share of operating losses sufficient to maintain

their minority ownership percentages. Actual total payments will be based on the amount of tax credits generated through the

end of 2007. In exchange, the SPVs will receive an estimated $192.0 million in tax benefits resulting from a combination of

deductions, allocated operating losses, and tax credits. The Corporation has guaranteed the SPVs commitments under the

purchase agreements. As of December 31, 2005, the Company has recorded $66.2 million in tax benefits and had an

estimated remaining commitment for fixed note payments, variable payments and the funding of their proportionate share of

e operating losses totaling $104.6 million. th

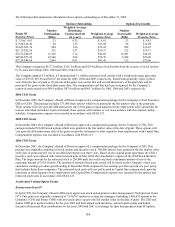

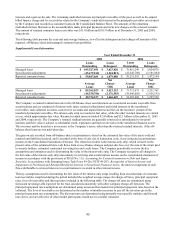

Guarantees

Residual Value Guarantees

In December 2000, the Company entered into a 10-year agreement for the lease of the headquarters building being

constructed in McLean, Virginia. The agreement called for monthly rent to commence upon completion, which occurred in

the first quarter of 2003, and is based on LIBOR rates applied to the cost of the building funded. If, at the end of the lease

term, the Company does not purchase the property, the Company guarantees a maximum residual value of up to $114.8

million representing approximately 72% of the $159.5 million cost of the building. This agreement, made with a multi-

purpose entity that is a wholly-owned subsidiary of one of the Company’ s lenders, provides that in the event of a sale of the

property, the Company’ s obligation would be equal to the sum of all amounts owed by the Company under a note issuance

made in connection with the lease inception. As of December 31, 2005, the value of the building was estimated to be above

the maximum residual value that the Company guarantees; thus, no deficiency existed and no liability was recorded relative

to this property. During 2005, the Company notified the lender of its intention to purchase the property in 2006 and as such

incurred a $20.6 million pre-payment penalty related to the refinancing of the McLean headquarters facility.

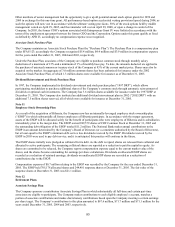

Other Guarantees

In connection with certain installment loan securitization transactions, the transferee (off-balance sheet special purpose entity

receiving the installment loans) entered into interest rate hedge agreements (the “swaps”) with a counterparty to reduce

interest rate risk associated with the transaction. In connection with the swaps, the Corporation entered into letter agreements

guaranteeing the performance of the transferee under the swaps. If at anytime the Class A invested amount equals zero and

the notional amount of the swap is greater than zero resulting in an “Early Termination Date” (as defined in the securitization

transaction’ s Master Agreement), then (a) to the extent that, in connection with the occurrence of such Early Termination

Date, the transferee is obligated to make any payments to the counterparty pursuant to the Master Agreement, the

Corporation shall reimburse the transferee for the full amount of such payment and (b) to the extent that, in connection with

the occurrence of an Early Termination Date, the transferee is entitled to receive any payment from the counterparty pursuant

to the Master Agreement, the transferee will pay to the Corporation the amount of such payment. At December 31, 2005, the

aximum exposure to the Corporation under the letter agreements was approximately $18.2 million. m

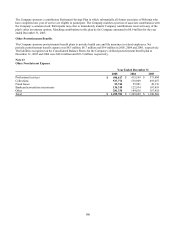

In

dustry Litigation

Over the past several years, MasterCard International and Visa U.S.A., Inc., as well as several of their member banks, have

been involved in several different lawsuits challenging various practices of MasterCard and Visa.

In 1998, the United States Department of Justice filed an antitrust lawsuit against the MasterCard and Visa membership

associations composed of financial institutions that issue MasterCard or Visa credit or debit cards (“associations”), alleging,

among other things, that the associations had violated antitrust law and engaged in unfair practices by not allowing member

banks to issue cards from competing brands, such as American Express and Discover Financial Services. In 2001, a New

York district court entered judgment in favor of the Department of Justice and ordered the associations to repeal these

policies. The United States Court of Appeals for the Second Circuit affirmed the district court and, on October 4, 2004, the

United States Supreme Court denied certiorari in the case. In November 2004, American Express filed an antitrust lawsuit

(the “Amex lawsuit”) against the associations and several member banks alleging that the associations and member banks

jointly and severally implemented and enforced illegal exclusionary agreements that prevented member banks from issuing

American Express and Discover cards. The complaint requests civil monetary damages, which could be trebled. The

Corporation, the Bank, and the Savings Bank are named defendants in this lawsuit.

93