Capital One 2005 Annual Report Download - page 50

Download and view the complete annual report

Please find page 50 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

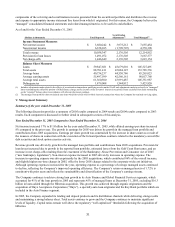

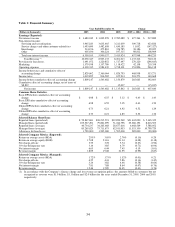

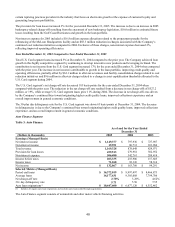

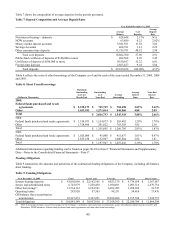

ear Ended December 31, 2005 Compared to Year Ended December 31, 2004 Y

The Auto Finance segment’ s loan portfolio increased 64% year over year as a result of 2005 acquisitions of Onyx Acceptance

Corporation and the Key Bank non-prime auto loan portfolio, as well as, strong organic originations growth aided, in part, by

uto manufacturers’ employee-pricing initiatives and other discount programs in 2005. a

Auto Finance net income decreased for the year ended December 31, 2005, as a result of increases in the provision for loan

l sses and non-interest expense, as well as lower gains from the sale of auto loans. o

Growth in the loan portfolio also resulted in a significant increase in revenue. However, this increase was offset by a decrease

in non-interest income primarily related to $24.7 million reduction in gains from the sale of auto loans, inclusive of

llocations related to funds transfer pricing, compared to the prior year. a

The provision for loan losses increased 64% for the year ended December 31, 2005, as a result of significant organic loan

growth, $16.0 million of estimated future incremental losses resulting from the Gulf Coast Hurricanes, and losses related to

e enactment of the new bankruptcy legislation. th

Non-interest expense increased 48% for the year ended December 31, 2005, driven by growth in the loan portfolio and

incremental operating and integration expenses related to the 2005 acquisitions.

For the year ended, December 31, 2005, the Auto Finance segment’ s net charge-off rate was down 58 basis points from the

prior year. Net charge-offs of Auto Finance segment loans increased $77.1 million, or 25%, while average Auto Finance

loans for the year ended December 31, 2005 grew $4.9 billion, or 52%, compared to the prior year. The decrease in the

charge-off rate was primarily driven by the acquisition of Onyx Acceptance Corporation, which originates and services a

portfolio of mostly prime auto receivables, improved loan quality, collections performance and favorable industry trends, and

a $20.4 million one-time acceleration of charge-offs in 2004 related to a change in the charge-off recognition process for auto

ans in bankruptcy. lo

The 30-plus day delinquency rate for the Auto Finance segment was up 21 basis points at December 31, 2005. The increase

in delinquencies was the result of a spike in bankruptcy filings prior to the enactment of the new bankruptcy legislation in

October 2005 and the $20.4 million one-time acceleration of charge-offs in December 2004, which moved delinquent

accounts to charge-off status in that year.

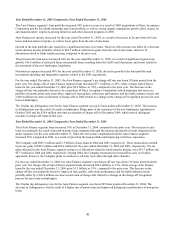

Year Ended December 31, 2004 Compared to Year Ended December 31, 2003

Total Auto Finance segment loans increased 18% at December 31, 2004, compared to the prior year. The increase in auto

loans was primarily the result of growth in prime loans originated through the internet and growth in loans originated in the

dealer segment. For the year ended December 31, 2004, the net income contribution from the Auto Finance segment

creased 65% compared to 2003, as a result of growth in the loan portfolio and improving credit loss experience. in

The Company sold $901.3 million and $1.9 billion of auto loans in 2004 and 2003, respectively. These transactions resulted

in pre-tax gains of $40.3 million and $66.4 million for the years ended December 31, 2004 and 2003, respectively. Pre-tax

gains allocated to the Auto Finance segment, inclusive of allocations related to funds transfer pricing, were $41.7 million and

$57.3 million in 2004 and 2003, respectively. During 2004, the Company terminated its forward flow auto receivables

agreement; however, the Company plans to continue to sell auto receivables through other channels.

For the year ended December 31, 2004, the Auto Finance segment’ s net charge-off rate was down 134 basis points from the

prior year. Net charge-offs of Auto Finance segment loans decreased $54.8 million, or 15%, while average Auto Finance

loans for the year ended December 31, 2004 grew $1.5 billion, or 19%, compared to the prior year. The decrease in the

charge-off rate was primarily driven by improved loan quality, collections performance and favorable industry trends,

partially offset by a $20.4 million one-time acceleration of charge-offs related to a change in the charge-off recognition

rocess for auto loans in bankruptcy. p

The 30-plus day delinquency rate for the Auto Finance segment was down 205 basis points at December 31, 2004. The

decrease in delinquencies was the result of a higher mix of prime loans and improved delinquency performance of non-prime

l ans. o

41