Capital One 2005 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

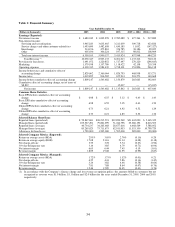

ear Ended December 31, 2004 Compared to Year Ended December 31, 2003 Y

Net income increased 36% over the prior year, while diluted earnings per share increased 28% compared to the prior year.

The growth in earnings for 2004 was primarily driven by an increase in the managed consumer loan portfolio, a reduction in

the provision for loan losses, and an increase in servicing and securitization income and other non-interest income, offset in

part by an increase in marketing and operating expenses.

Managed loans consist of the Company’ s reported loan portfolio combined with the off-balance sheet securitized loan

portfolio. The Company has retained servicing rights for its securitized loans and receives servicing fees in addition to the

excess spread generated from the off-balance sheet loan portfolio. Average managed loans increased 17% for the year ended

December 31, 2004.

The managed net interest margin for the year ended December 31, 2004, decreased 76 basis points. This decrease was due to

a reduction in managed earning asset yields, slightly offset by a reduction in the cost of funds. Managed loan yields decreased

by 83 basis points for the year ended December 31, 2004. The decrease in managed loan yields resulted from the Company’ s

continued asset diversification beyond U.S. consumer credit cards and a bias toward originating higher credit quality, lower

yielding loans. In addition, the Company built the average size of its liquidity portfolio by $3.5 billion, placing additional

downward pressure on managed earning asset yields as the yield on the liquidity portfolio is lower than the yield on

consumer loans.

For the year ended December 31, 2004, the provision for loan losses decreased to $1.2 billion from $1.5 billion for the year

ended December 31, 2003. The decrease in the provision for loan losses reflects a reduction in net charge-offs, improving

delinquency rates and lower forecasted charge-offs for the reported loan portfolio at December 31, 2004. The improvements

in the Company’ s credit quality metrics are a result of the continued asset diversification beyond U.S consumer credit cards,

continued bias toward originating higher credit quality, lower yielding loans, improved collection experience and an overall

provement in general economic conditions compared with the prior year. im

Servicing and securitizations income increased $432.1 million as a result of a 16% increase in the average off-balance sheet

loan portfolio for the year ended December 31, 2004 when compared with the prior year, partially offset by a reduction in the

excess spread generated by the off-balance sheet portfolio due to a higher concentration of higher credit quality, lower

yielding loans.

For the year ended December 31, 2004, other non-interest income increased 51%, when compared to the prior year. This

increase is primarily attributable to $72.6 million in pre-tax gains recognized in 2004 on the sale of the Company’ s joint

venture investment in South Africa and sale of the French loan portfolio. The remaining variance is due to increases in

income derived from purchased charged-off loan portfolios, slightly offset by a decrease in auto gains and an increase in

sses on sales of securities available for sale and losses on the repurchases of senior notes during 2004. lo

Marketing expense increased 20% for the year ended December 31, 2004, compared to the prior year. The increase in

marketing expense resulted from favorable opportunities to originate loans during 2004 combined with continued brand

investments. Operating expenses increased 7%, for the year ended December 31, 2004. The increases were primarily related

to charges associated with corporate-wide cost reduction initiatives, charges related to a change in asset capitalization

thresholds and charges related to the impairment of internally developed software. Although operating expenses increased,

operating expenses as a percentage of average managed loans for the year ended December 31, 2004 fell 53 basis points to

5.41% from 5.94% for the prior year. This reduction reflects the continued improvement in the Company’ s operating

efficiencies.

2005 Significant Events

Acquisitions

In November 2005, the Company acquired Hibernia Corporation, a financial holding company headquartered in New

Orleans, Louisiana. As part of the transaction, Hibernia Corporation was merged into the Corporation. Hibernia’ s retail bank

subsidiary, which is now a wholly owned subsidiary of the Corporation, Hibernia National Bank, has over 300 branch

locations operating in Louisiana and Texas. The $5.0 billion acquisition was settled through the issuance of 32.9 million

shares of the Company’ s common stock and $2.2 billion in cash and resulted in $3.2 billion of goodwill.

In the first quarter of 2005, the Company acquired Onyx Acceptance Corporation, a specialty auto loan originator; Hfs

Group, a United Kingdom based home equity broker; InsLogic, an insurance brokerage firm, and eSmartloan, a U.S. based

online originator of home equity loans and mortgages. All were acquired in all cash transactions and resulted in $391.4

32