Capital One 2005 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

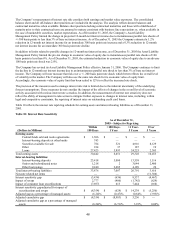

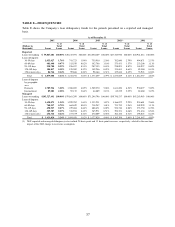

The Company has deposits that are obtained through the use of a third-party intermediary. Included in these deposits at

December 31, 2005, were brokered deposits of $11.4 billion, compared to $9.1 billion at December 31, 2004. These deposits

represented 24% and 36% of total deposits at December 31, 2005 and 2004, respectively. If these brokered deposits are not

renewed at maturity, the Company would use its investment securities and money market instruments in addition to

alternative funding sources to fund increases in loan receivables and meet its other liquidity needs. The Federal Deposit

Insurance Corporation Improvement Act of 1991 limits the use of brokered deposits to “well-capitalized” insured depository

institutions and, with a waiver from the Federal Deposit Insurance Corporation, to “adequately capitalized” institutions. At

December 31, 2005, the Bank, the Savings Bank, the National Bank and the Company were “well-capitalized” as defined

under the federal bank regulatory guidelines. Based on the Company’ s historical access to the brokered deposit market, it

expects to replace maturing brokered deposits with new brokered deposits or with the Company’ s direct deposits.

Other funding programs established by the Company include senior and subordinated notes. At December 31, 2005, the

Company had $6.7 billion in senior and subordinated notes outstanding that mature in varying amounts from 2006 to 2017, as

compared to $6.9 billion at December 31, 2004.

An additional source of funding for the Bank is provided by its global bank note program. Notes may be issued under this

program with maturities of thirty days or more from the date of issue. At December 31, 2005, the Bank had $4.4 billion in

bank notes outstanding. The bank notes are included in long-term debt and senior and subordinated notes in the Company’ s

balance sheet.

Subsidiary banks are members of various Federal Home Loan Banks (“FHLB”) that provide a source of funding through

advances. These advances carry maturities from one month to 20 years. At December 31, 2005, the Company had $1.5 billion

of advances from the FHLBs. All FHLB borrowings are collateralized with mortgage-related assets which may include

r sidential and commercial mortgages and home equity loans. e

The Company also held $9.2 billion in available-for-sale investment securities, net of $5.1 billion in pledged available-for-

sale investment securities and $4.1 billion of cash and cash equivalents at December 31, 2005, compared to $7.7 billion in

investment securities, net of $1.6 billion in pledged investment securities and $1.4 billion of cash and cash equivalents at

December 31, 2004. As of December 31, 2005, the weighted average life of the investment securities was approximately 3.4

years. These investment securities, along with cash and cash equivalents, provide increased liquidity and flexibility to support

the Company’ s funding requirements.

The Company has a $750.0 million credit facility committed through June 2007. The Company may take advances under the

facility subject to covenants and conditions customary in a transaction of this nature. This facility may be used for general

corporate purposes and was not drawn upon at December 31, 2005.

D

erivative Instruments

The Company enters into interest rate swap agreements in order to manage interest rate exposure. In most cases, this

exposure is related to the funding of fixed rate assets with floating rate obligations, including off-balance sheet

securitizations. The Company also enters into forward foreign currency exchange contracts and cross currency swaps to

reduce sensitivity to changing foreign currency exchange rates. The hedging of foreign currency exchange rates is limited to

certain intercompany obligations related to international operations. These derivatives expose the Company to certain credit

risks. The Company has established policies and limits, as well as collateral agreements, to manage credit risk related to

erivative instruments. d

Supplementary Data—Notes to the Consolidated Financial Statements—Note 22”.

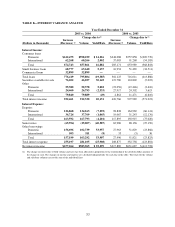

IX. Market Risk Management

In

terest Rate Risk

Interest rate risk refers to changes in earnings or the net present value of assets and off-balance sheet positions less liabilities

(termed “economic value of equity”) due to interest rate changes. To the extent that managed interest income and expense do

not respond equally to changes in interest rates, or that all rates do not change uniformly, earnings and the economic value of

equity could be affected. The Company manages and mitigates its interest rate sensitivity through several techniques, which

include, but are not limited to, changing the maturity and repricing characteristics of various balance sheet categories and by

entering into interest rate swaps.

47

Additional information regarding derivative instruments can be found on pages 97-98 in Item 8 “Financial Statements and