Capital One 2005 Annual Report Download - page 38

Download and view the complete annual report

Please find page 38 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

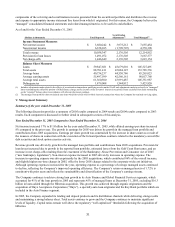

The securitization of consumer loans has been a significant source of liquidity for the Company. Maturity terms of the

existing securitizations vary from 2006 to 2025 and, for revolving securitizations, have accumulation periods during which

principal payments are aggregated to make payments to investors. As payments on the loans are accumulated and are no

longer reinvested in new loans, the Company’ s funding requirements for such new loans increase accordingly. The Company

believes that it has the ability to continue to utilize off-balance sheet securitization arrangements as a source of liquidity;

however, a significant reduction or termination of the Company’ s off-balance sheet securitizations could require the

Company to draw down existing liquidity and/or to obtain additional funding through the issuance of secured borrowings or

unsecured debt, the raising of additional deposits or the slowing of asset growth to offset or to satisfy liquidity needs.

Recourse Exposure

The credit quality of the receivables transferred is supported by credit enhancements, which may be in various forms

including interest-only strips, subordinated interests in the pool of receivables, cash collateral accounts, cash reserve accounts

and accrued interest and fees on the investor’ s share of the pool of receivables. Some of these credit enhancements are

retained by the seller and are referred to as retained residual interests. The Company’ s retained residual interests are generally

restricted or subordinated to investors’ interests and their value is subject to substantial credit, repayment and interest rate

risks on transferred assets if the off-balance sheet loans are not paid when due. Securitization investors and the trusts only

have recourse to the retained residual interests, not the Company’ s assets. See pages 109-112 in Item 8 “Financial Statements

and Supplementary Data—Notes to the Consolidated Financial Statements—Note 21” for quantitative information regarding

tained interests. re

Collections and Amortization

Collections of interest and fees received on securitized receivables are used to pay interest to investors, servicing and other

fees, and are available to absorb the investors’ share of credit losses. For revolving securitizations, amounts collected in

excess of that needed to pay the above amounts are remitted, in general, to the Company. Under certain conditions, some of

the cash collected may be retained to ensure future payments to investors. For amortizing securitizations, amounts collected

in excess of the amount that is used to pay the above amounts are generally remitted to the Company, but may be paid to

Supplementary Data—Notes to the Consolidated Financial Statements—Note 21” for quantitative information regarding

revenues, expenses and cash flows that arise from securitization transactions.

Securitization transactions may amortize earlier than scheduled due to certain early amortization triggers, which would

accelerate the need for funding. Additionally, early amortization would have a significant impact on the ability of the Bank

and Savings Bank to meet regulatory capital adequacy requirements as all off-balance sheet loans experiencing such early

amortization would be recorded on the balance sheet and accordingly would require incremental regulatory capital. As of

December 31, 2005, no early amortization events related to the Company’ s off-balance sheet securitizations have occurred.

The amounts of investor principal from off-balance sheet consumer loans as of December 31, 2005 that are expected to

amortize into the Company’ s consumer loans, or be otherwise paid over the periods indicated, are summarized in Table 9. Of

the Company’ s total managed loans, 43% and 52% were included in off-balance sheet securitizations for the years ended

December 31, 2005 and 2004, respectively.

Letters of Credit and Financial Guarantees

As a result of the acquisition of Hibernia, the Company issues letters of credit and financial guarantees (“standby letters of

credit”) whereby it agrees to honor certain financial commitments in the event its customers are unable to perform. The

majority of the standby letters of credit consist of financial guarantees. Collateral requirements are similar to those for funded

transactions and are established based on management’ s credit assessment of the customer. Management conducts regular

reviews of all outstanding standby letters of credit and customer acceptances, and the results of these reviews are considered

assessing the adequacy of the Company’ s allowance for loan losses. in

The Company had contractual amounts of standby letters of credit of $569.2 million at December 31, 2005. As of

December 31, 2005, standby letters of credit had expiration dates ranging from 2006 to 2010. The fair value of the guarantees

outstanding at December 31, 2005 that have been issued since January 1, 2003, was $4.7 million and was included in other

liabilities.

oan and Line of Credit Commitments L

As a result of the acquisition of Hibernia, the Company enters into commitments to extend credit are legally binding

conditional agreements having fixed expirations or termination dates and specified interest rates and purposes. These

29

investors in further reduction of their outstanding principal. See pages 94-96 in Item 8 “Financial Statements and