Capital One 2005 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2005 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

|

|

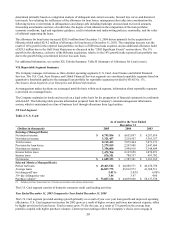

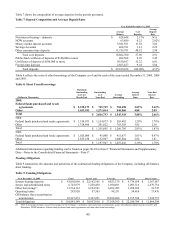

Summary of the Reported Income Statement

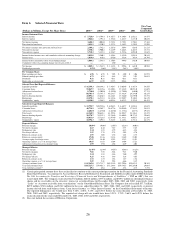

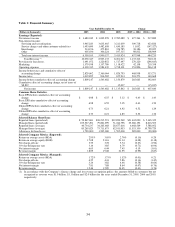

The following is a detailed description of the financial results reflected in Table 1 – Financial Summary. Additional

formation is provided in section XII, Tabular Summary as detailed in sections below. in

All 2005 comparisons are made between the year ended December 31, 2005 and the year ended December 31, 2004. All 2004

comparisons are made between the year ended December 31, 2004 and the year ended December 31, 2003.

N

et interest income

Net interest income is comprised of interest income and past-due fees earned and deemed collectible from the Company’ s

loans and income earned on securities, less interest expense on interest-bearing deposits, senior and subordinated notes and

ther borrowings. o

For the year ended December 31, 2005, reported net interest income increased 23%. The increase was primarily due to

significant growth in reported average earning assets. The yield on earning assets and cost of funds remained relatively stable

ear over year. y

Reported net interest income for the year ended December 31, 2004 increased 8% compared to the prior year. The increase in

net interest income is primarily a result of a 25% increase in the Company’ s reported average earning assets for the year

ended December 31, 2004, offset by a decrease in earning asset yields. The reported net interest margin decreased 101 basis

points compared to the prior year. The decrease was primarily due to a decrease in the reported loan yield, slightly offset by a

decrease in the cost of funds. The reported loan yield decreased 135 basis points. The yield on reported loans decreased due

to the Company’ s continued asset diversification beyond U.S. consumer credit cards and continued bias toward originating

higher credit quality, lower yielding loans when compared with the prior year. In addition, the Company increased the

average size of its liquidity portfolio by $3.5 billion during 2004. The yield on liquidity portfolio assets is typically lower

t an those on consumer loans and served to reduce the overall earning assets yields. h

For additional information, see section XII, Tabular Summary, Table A (Statements of Average Balances, Income and

Expense, Yields and Rates) and Table B (Interest Variance Analysis).

N

on-interest income

Non-interest income is comprised of servicing and securitizations income, service charges and other customer-related fees,

interchange income and other non-interest income.

For the year ended December 31, 2005 and 2004, reported non-interest income increased 8% and 9%, respectively. The 2005

and 2004 increases were both due to year over year increases in servicing and securitizations income, service charges and

other customer-related fees, interchange income and other non-interest income. See detailed discussion of the components of

on-interest income below. n

Servicing and Securitizations Income

Servicing and securitizations income represents servicing fees, excess spread and other fees derived from the off-balance

sheet loan portfolio, adjustments to the fair value of retained interests derived through securitization transactions, as well as

gains and losses resulting securitization and other sales transactions.

Servicing and securitizations income increased 9% for the year ended December 31, 2005. This increase was primarily the

result of a 13% increase in the average off-balance sheet loan portfolio offset by losses from the Gulf Coast hurricanes and

bankruptcy charge-offs resulting from the new bankruptcy legislation.

Servicing and securitizations income increased 13% for the year ended December 31, 2004. This increase was primarily the

result of a 16% increase in the average off-balance sheet loan portfolio for the year ended December 31, 2004, compared to

the prior year, partially offset by a reduction in the excess spread generated by the off-balance sheet portfolio due to a higher

oncentration of higher credit quality, lower yielding loans. c

Service Charges and Other Customer-Related Fees

Excluding $44.7 million contributed by businesses acquired in 2005, service charges and other customer-related fees

decreased 2% for the year ended December 31, 2005, while the average reported loan portfolio, exclusive of the 2005

acquisitions, grew 7%. The lower growth in service charges and other customer-related fee income when compared to

average reported loan growth is reflective of the reported loan growth being concentrated in the Auto Finance and Global

Financial Services segments that generate lower fee income.

35