BMW 2013 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2013 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

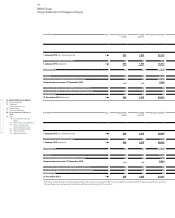

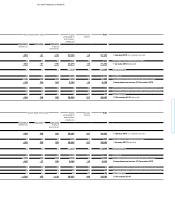

99 GROUP FINANCIAL STATEMENTS

Accounting policies

The financial statements of BMW AG and of its subsidi-

aries in Germany and elsewhere have been prepared

for consolidation purposes using uniform accounting

policies in accordance with IAS 27 (Consolidated and

Separate Financial Statements).

Revenues from the sale of products are recognised when

the risks and rewards of ownership of the goods are

transferred to the dealer or customer, provided that the

amount of revenue can be measured reliably, it is

probable that the economic benefits associated with the

transaction will flow to the entity and costs incurred

or

to be incurred in respect of the sale can be measured

reliably. Revenues are stated net of settlement discount,

bonuses and rebates. Revenues also include lease rentals

and interest income earned in conjunction with

finan-

cial services. Revenues from leasing instalments relate

to operating leases and are recognised in the income

statement on a straight line basis over the relevant term

of the lease. Interest income from finance leases and

from customer and dealer financing are recognised using

the effective interest method and reported as revenues

within the line item “Interest income on loan financing”.

If the sale of products includes a determinable amount

for subsequent services (multiple-component contracts),

the related revenues are deferred and recognised as

income over the relevant service period. Amounts are

normally recognised as income by reference to the pat-

tern of related expenditure.

Profits arising on the sale of vehicles for which a Group

company retains a repurchase commitment (buy-back

contracts) are not recognised until such profits have

been

realised. The vehicles are included in inventories and

stated at cost.

Cost of sales comprises the cost of products sold and the

acquisition cost of purchased goods sold. In addition

to directly attributable material and production costs, it

also includes research costs and development costs not

recognised as assets, the amortisation of capitalised

development costs as well as overheads (including de-

preciation of property, plant and equipment and amor-

tisation of other intangible assets relating to produc-

tion) and write-downs on inventories. Cost of sales also

includes freight and insurance costs relating to deliveries

to dealers and agency fees on direct sales. Expenses

which are directly attributable to financial services busi-

ness (including depreciation on leased products) and in-

terest expense from refinancing the entire financial ser-

vices business, including the expense of

risk provisions

and write-downs, are reported in cost of

sales.

In accordance with IAS 20 (Accounting for Government

Grants and Disclosure of Government Assistance),

pub-

lic sector grants are not recognised until there is

reason-

able assurance that the conditions attaching to them

have been complied with and the grants will be received.

They are recognised as income over the periods neces-

sary to match them with the related costs which they are

intended to compensate.

Basic earnings per share are computed in accordance with

IAS 33 (Earnings per Share). Basic earnings per share

are calculated for common and preferred stock by di-

viding the net profit after minority interests, as attribut-

able to each category of stock, by the average number

of outstanding shares. The net profit is accordingly allo-

cated to the different categories of stock. The portion of

the Group net profit for the year which is not being

dis-

tributed is allocated to each category of stock based on

the number of outstanding shares. Profits available for

distribution are determined directly on the basis of the

dividend resolutions passed for common and preferred

stock. Diluted earnings per share would have to be dis-

closed separately.

Share-based remuneration programmes which are ex-

pected to be settled in shares are, in accordance with

IFRS 2 (Share-based Payments), measured at their fair

value at grant date. The related expense is recognised

in the income statement (as personnel expense) over the

vesting period, with a contra (credit) entry recorded

against capital reserves.

Share-based remuneration programmes expected to be

settled in cash are revalued to their fair value at each

balance sheet date between the grant date and the settle-

ment date (and on the settlement date itself). The ex-

pense for such programmes is recognised in the income

statement (as personnel expense) over the vesting pe-

riod of the programmes and recognised in the balance

sheet as a provision.

The share-based remuneration programme for Board

of

Management members and senior heads of depart-

ment entitles BMW AG to elect whether to settle its

commitments in cash or with shares of BMW AG

com-

mon stock. Following the decision to settle in cash,

5