BMW 2013 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2013 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

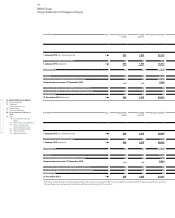

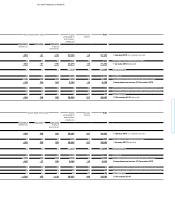

101 GROUP FINANCIAL STATEMENTS

Where Group products are recognised by BMW Group

entities as leased products under operating leases, they

are measured at manufacturing cost. All other leased

products are measured at acquisition cost. All leased

products are depreciated over the period of the lease

using the straight-line method down to their expected

residual value. Changes in residual value expectations

are recognised – in situations where the recoverable

amount of the lease exceeds the carrying amount of

the asset – by adjusting scheduled depreciation

pro-

spectively over the remaining term of the lease

contract. If the recoverable amount is lower than the

expected residual value, an impairment loss is recog-

nised for the shortfall. A test is carried out at each

balance sheet date to determine whether an impair-

ment loss recognised in prior years no longer exists

or has decreased. In these cases, the carrying amount

of the asset is increased to the recoverable amount.

The higher carrying amount resulting from the rever-

sal may not, however, exceed the rolled-forward amor-

tised cost of the asset.

If there is any evidence of impairment of non-financial

assets (except inventories and deferred taxes), or if an

annual impairment test is required to be carried out –

i. e. for intangible assets not yet available for use, intan-

gible assets with an indefinite useful life and goodwill

acquired as part of a business combination – an impair-

ment test pursuant to IAS 36 (Impairment of Assets)

is performed. Each individual asset is tested separately

unless the asset generates cash flows that are largely

independent of the cash flows from other assets or

groups of assets (cash-generating units / CGUs). For the

purposes of the impairment test, the asset’s carrying

amount is compared with its recoverable amount, the

latter defined as the higher of the asset’s fair value less

costs to sell and its value in use. An impairment loss

is

recognised when the recoverable amount is lower than

the asset’s carrying amount. Fair value is the price that

would be received to sell an asset in an orderly trans-

action between market participants at the measurement

date. The value in use corresponds to the present value

of future cash flows expected to be derived from an asset

or groups of assets.

The first step of the impairment test is to determine the

value in use of an asset. If the calculated value in use is

lower than the carrying amount of the asset, then its

fair value less costs to sell are also determined. If the lat-

ter is also lower than the carrying amount of the asset,

then an impairment loss is recorded, reducing the car-

rying

amount to the higher of the asset’s value in use

or fair value less costs to sell. The value in use is deter-

mined on the basis of a present value computation.

Cash flows used for the purposes of this calculation are

derived from long-term forecasts approved by manage-

ment.

The long-term forecasts themselves are based on

detailed forecasts drawn up at an operational level

and, based on a planning period of six years, correspond

roughly to a typical product’s life-cycle. For the purposes

of calculating cash flows beyond the planning period,

the asset’s assumed residual value does not take growth

into account. Forecasting assumptions are continually

brought up to date and regularly compared with exter-

nal sources of information. The assumptions used take

account in particular of expectations of the profitability

of the product portfolio, future market share

develop-

ments, macro-economic developments (such as currency,

interest rate and raw materials) as well as the legal

en-

vironment and past experience. Cash flows of the Auto-

motive and Motorcycles CGUs are discounted using a

risk-adjusted pre-tax weighted average cost of capital

(WACC) of 12.0 % (2012: 12.0 %). In the case of the Finan-

cial Services CGU, a sector-compatible pre-tax cost of

equity capital of 13.4 % (2012: 13.4 %) is applied. In con-

junction with the impairment tests for CGUs, sensitivity

analyses are performed for the main assumptions.

Analyses performed in the year under report confirmed,

as in the previous year, that no impairment loss was re-

quired to be recognised.

If the reason for a previously recognised impairment

loss no longer exists, the impairment loss is reversed up

to the level of the recoverable amount, capped at the

level of rolled-forward amortised cost. This does not ap-

ply to goodwill: previously recognised impairment

losses

on goodwill are not reversed.

Investments accounted for using the equity method are

(except when the investment is impaired) measured at

the Group’s share of equity taking account of fair value

adjustments on acquisition. Investments accounted

for using the equity method comprise joint ventures and

significant associated companies.