BMW 2013 Annual Report Download - page 155

Download and view the complete annual report

Please find page 155 of the 2013 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

|

|

155 GROUP FINANCIAL STATEMENTS

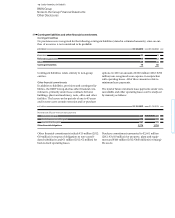

In the next stage, these exposures are compared to all

hedges that are in place. The net cash flow surplus

the reporting period amounted to € 6,760 million (2012:

€ 6,044 million).

Solvency is assured at all times by managing and moni-

toring the liquidity situation on the basis of a rolling

cash flow forecast. The resulting funding requirements

are secured by a variety of instruments placed on the

world’s financial markets. The objective is to minimise

risk by matching maturities for the Group’s financing

requirements within the framework of the target debt

structure. The BMW Group has good access to capital

markets as a result of its solid financial position and a

diversified refinancing strategy. This is underpinned

by

the longstanding long- and short-term ratings issued

by Moody’s and Standard & Poor’s.

Short-term liquidity is managed primarily by issuing

money market instruments (commercial paper). In

this

area too, competitive refinancing conditions can

be achieved thanks to Moody’s and Standard & Poor’s

short-term ratings of P-1 and A-1 respectively.

Also reducing liquidity risk, additional secured and

unsecured lines of credit are in place with first-class in-

ternational banks, including a syndicated credit line

totalling € 6 billion (2012: € 6 billion). Intra-group cash

flow fluctuations are evened out by the use of daily

cash pooling arrangements.

Market risks

The principal market risks to which the BMW Group is

exposed are currency risk, interest rate risk and raw

materials price risk.

Protection against such risks is provided in the first

instance through natural hedging which arises when the

values of non-derivative financial instruments have

matching maturities and amounts (netting). Derivative

financial instruments are used to reduce the risk

re-

represents an uncovered risk position. The cash-flow-at-

risk approach involves allocating the impact of potential

maining after netting. Financial instruments are only

used to hedge underlying positions or forecast trans-

actions.

The scope of permitted transactions, responsibilities,

financial reporting procedures and control mechanisms

used for financial instruments are set out in internal

guidelines. This includes, above all, a clear separation

of duties between trading and processing. Currency,

interest rate and raw materials price risks of the BMW

Group are managed at a corporate level.

Further information is provided in the “Report on out-

look, risks and opportunities” section of the Combined

Management Report.

Currency risk

As an enterprise with worldwide operations, business

is conducted in a variety of currencies, from which cur-

rency risks arise. Since a significant portion of Group

revenues is generated outside the euro currency region

and the procurement of production material and fund-

ing is also organised on a worldwide basis, the currency

risk is an extremely important factor for Group earnings.

At 31 December 2013 derivative financial instruments,

mostly in the form of option and forward currency con-

tracts, were in place to hedge the main currencies.

A description of the management of this risk is pro-

vided in the Combined Management Report. The BMW

Group measures currency risk using a cash-flow-at-risk

model.

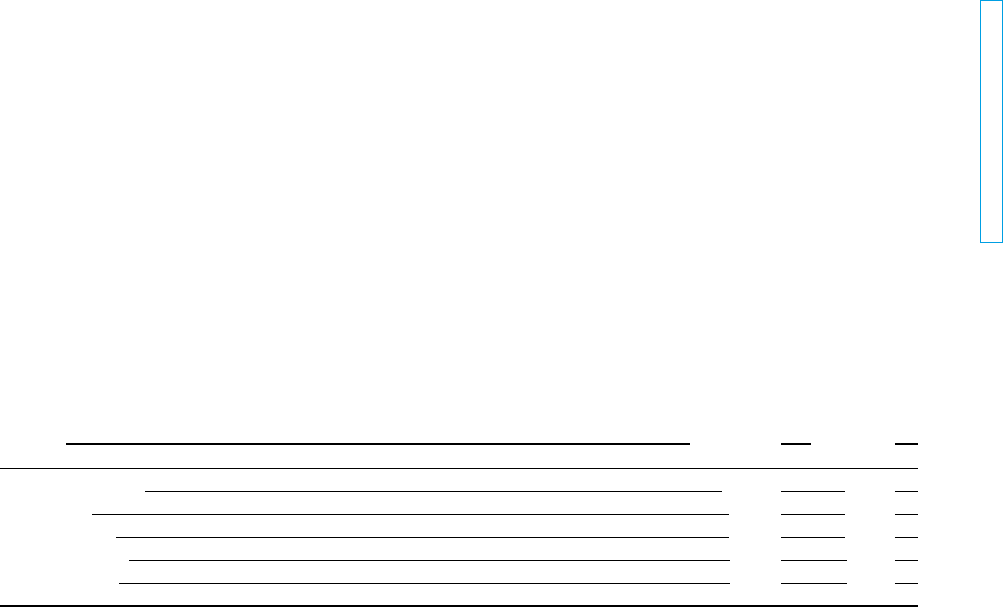

The starting point for analysing currency risk with this

model is the identification of forecast foreign currency

transactions or “exposures”. At the end of the reporting

period, the principal exposures for the relevant coming

year were as follows:

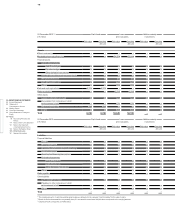

in € million 31. 12. 2013 31. 12. 2012

Euro / Chinese Renminbi 10,691 8,429

Euro / US Dollar 4,401 5,311

Euro / British Pound 3,852 3,206

Euro / Russian Rouble 1,738 1,638

Euro / Japanese Yen

1,469 1,585