Wells Fargo 2013 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

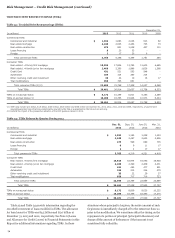

Risk Management – Credit Risk Management (continued)

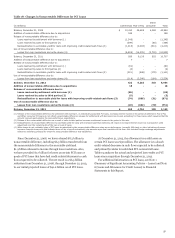

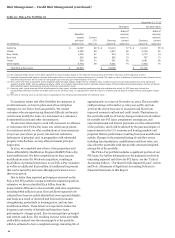

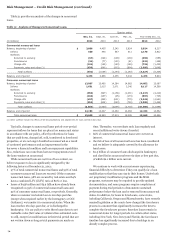

Table 25: Pick-a-Pay Portfolio (1)

December 31, 2013

PCI loans All other loans

(in millions)

Adjusted

unpaid

principal

balance (2)

Current

LTV

ratio (3)

Carrying

value (4)

Ratio of

carrying

value to

current

value (5)

Carrying

value (4)

Ratio of

carrying

value to

current

value (5)

California $ 19,797 89 % $ 16,213 72 % $ 13,219 65 %

Florida 2,395 98 1,827 69 2,764 80

New Jersey 1,029 87 974 74 1,770 74

New York 609 84 592 73 797 73

Texas 266 70 241 62 1,081 56

Other states 4,704 89 4,001 74 7,492 75

Total Pick-a-Pay loans $ 28,800 $ 23,848 $ 27,123

(1) The individual states shown in this table represent the top five states based on the total net carrying value of the Pick-a-Pay loans at the beginning of 2013.

(2) Adjusted unpaid principal balance includes write-downs taken on loans where severe delinquency (normally 180 days) or other indications of severe borrower financial stress

exist that indicate there will be a loss of contractually due amounts upon final resolution of the loan.

(3) The current LTV ratio is calculated as the adjusted unpaid principal balance divided by the collateral value. Collateral values are generally determined using automated

valuation models (AVM) and are updated quarterly. AVMs are computer-based tools used to estimate market values of homes based on processing large volumes of market

data including market comparables and price trends for local market areas.

(4) Carrying value, which does not reflect the allowance for loan losses, includes remaining purchase accounting adjustments, which, for PCI loans may include the

nonaccretable difference and the accretable yield and, for all other loans, an adjustment to mark the loans to a market yield at date of merger less any subsequent charge-

offs.

(5) The ratio of carrying value to current value is calculated as the carrying value divided by the collateral value.

To maximize return and allow flexibility for customers to

avoid foreclosure, we have in place several loss mitigation

strategies for our Pick-a-Pay loan portfolio. We contact

customers who are experiencing financial difficulty and may in

certain cases modify the terms of a loan based on a customer’s

documented income and other circumstances.

We also have taken steps to work with customers to refinance

or restructure their Pick-a-Pay loans into other loan products.

For customers at risk, we offer combinations of term extensions

of up to 40 years (from 30 years), interest rate reductions,

forbearance of principal, and, in geographies with substantial

property value declines, we may offer permanent principal

forgiveness.

In 2013, we completed more than 11,800 proprietary and

Home Affordability Modification Program (HAMP) Pick-a-Pay

loan modifications. We have completed more than 123,000

modifications since the Wachovia acquisition, resulting in

$5.8 billion of principal forgiveness to our Pick-a-Pay customers

as well as an additional $229 million of conditional forgiveness

that can be earned by borrowers through performance over a

three year period.

Due to better than expected performance observed on the

Pick-a-Pay PCI portfolio compared with the original acquisition

estimates, we have reclassified $3.9 billion from the

nonaccretable difference to the accretable yield since acquisition,

including $866 million in 2013. Our cash flows expected to be

collected have been favorably affected by lower expected defaults

and losses as a result of observed and forecasted economic

strengthening, particularly in housing prices, and our loan

modification efforts. These factors are expected to reduce the

frequency and severity of defaults and keep these loans

performing for a longer period, thus increasing future principal

and interest cash flows. The resulting increase in the accretable

yield will be realized over the remaining life of the portfolio,

which is estimated to have a weighted-average remaining life of

approximately 12.7 years at December 31, 2013. The accretable

yield percentage at December 31, 2013 was 4.98%, up from

4.70% at the end of 2012 due to increased cash flows from

improved economic outlook and credit trends. Fluctuations in

the accretable yield are driven by changes in interest rate indices

for variable rate PCI loans, prepayment assumptions, and

expected principal and interest payments over the estimated life

of the portfolio, which will be affected by the pace and degree of

improvements in the U.S. economy and housing markets and

projected lifetime performance resulting from loan modification

activity. Changes in the projected timing of cash flow events,

including loan liquidations, modifications and short sales, can

also affect the accretable yield rate and the estimated weighted-

average life of the portfolio.

The Pick-a-Pay portfolio includes a significant portion of our

PCI loans. For further information on the judgment involved in

estimating expected cash flows for PCI loans, see the “Critical

Accounting Policies – Purchased Credit-Impaired Loans” section

and Note 1 (Summary of Significant Accounting Policies) to

Financial Statements in this Report.

64