Wells Fargo 2013 Annual Report Download - page 150

Download and view the complete annual report

Please find page 150 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

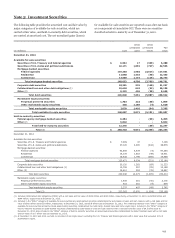

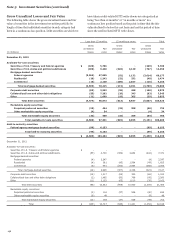

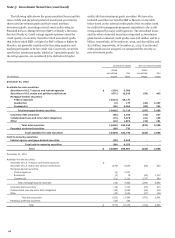

Note 1: Summary of Significant Accounting Policies (continued)

carrying amount, quantitative tests are not required. We assess

goodwill for impairment on a reporting unit level and apply

various quantitative valuation methodologies when required to

compare the estimated fair value to the carrying value of each

reporting unit. Valuation methodologies include discounted cash

flow and earnings multiple approaches. If the fair value is less

than the carrying amount, an additional test is required to

measure the amount of impairment. We recognize impairment

losses as a charge to noninterest expense (unless related to

discontinued operations) and an adjustment to the carrying

value of the goodwill asset. Subsequent reversals of goodwill

impairment are prohibited.

We amortize core deposit and other customer relationship

intangibles on an accelerated basis over useful lives not

exceeding 10 years. We review such intangibles for impairment

whenever events or changes in circumstances indicate that their

carrying amounts may not be recoverable. Impairment is

indicated if the sum of undiscounted estimated future net cash

flows is less than the carrying value of the asset. Impairment is

permanently recognized by writing down the asset to the extent

that the carrying value exceeds the estimated fair value.

Operating Lease Assets

Operating lease rental income for leased assets is recognized in

other income on a straight-line basis over the lease term. Related

depreciation expense is recorded on a straight-line basis over the

estimated useful life, considering the estimated residual value of

the leased asset. The useful life may be adjusted to the term of

the lease depending on our plans for the asset after the lease

term. On a periodic basis, leased assets are reviewed for

impairment. Impairment loss is recognized if the carrying

amount of leased assets exceeds fair value and is not recoverable.

The carrying amount of leased assets is not recoverable if it

exceeds the sum of the undiscounted cash flows expected to

result from the lease payments and the estimated residual value

upon the eventual disposition of the equipment.

Liability for Mortgage Loan Repurchase Losses

We sell residential mortgage loans to various parties, including

(1) government-sponsored entities (GSEs) Federal Home Loan

Mortgage Corporation (FHLMC) and Federal National Mortgage

Association (FNMA) who include the mortgage loans in GSE-

guaranteed mortgage securitizations, (2) SPEs that issue private

label MBS, and (3) other financial institutions that purchase

mortgage loans for investment or private label securitization. In

addition, we pool Federal Housing Administration (FHA)-

insured and Department of Veterans Affairs (VA)-guaranteed

mortgage loans, which back securities guaranteed by the

Government National Mortgage Association (GNMA).

We may be required to repurchase mortgage loans,

indemnify the securitization trust, investor or insurer, or

reimburse the securitization trust, investor or insurer for credit

losses incurred on loans (collectively “repurchase”) in the event

of a breach of specified contractual representations or warranties

that are not remedied within a period (usually 90 days or less)

after we receive notice of the breach. Our loan sale contracts to

private investors (non-GSE) typically contain an additional

provision where we would only be required to repurchase

securitized loans if a breach is deemed to have a material and

adverse effect on the value of the mortgage loan or to the

investors or interests of security holders in the mortgage loan.

We establish a mortgage repurchase liability, initially at fair

value, related to various representations and warranties that

reflect management’s estimate of losses for loans for which we

could have a repurchase obligation, whether or not we currently

service those loans, based on a combination of factors. Such

factors include default expectations, expected investor

repurchase demands (influenced by current and expected

mortgage loan file requests and mortgage insurance rescission

notices, as well as estimated levels of origination defects) and

appeals success rates (where the investor rescinds the demand

based on a cure of the defect or acknowledges that the loan

satisfies the investor’s applicable representations and

warranties), reimbursement by correspondent and other third

party originators, and projected loss severity. We continually

update our mortgage repurchase liability estimate during the life

of the loans. Although activity can vary by investor, investors

may demand repurchase at any time and there is often a lag from

the date of default to the time we receive a repurchase demand.

The majority of repurchase demands are on loans that default in

the first 24 to 36 months following origination of the mortgage

loan.

The liability for mortgage loan repurchase losses is included

in other liabilities. For additional information on our repurchase

liability, see Note 9.

Pension Accounting

We account for our defined benefit pension plans using an

actuarial model. Two principal assumptions in determining net

periodic pension cost are the discount rate and the expected long

term rate of return on plan assets.

A discount rate is used to estimate the present value of our

future pension benefit obligations. We use a consistent

methodology to determine the discount rate based upon the

yields on multiple portfolios of bonds with maturity dates that

closely match the estimated timing and amounts of the expected

benefit payments for our plans. Such portfolios are derived from

a broad-based universe of high quality corporate bonds as of the

measurement date.

Our determination of the reasonableness of our expected

long-term rate of return on plan assets is highly quantitative by

nature. We evaluate the current asset allocations and expected

returns under two sets of conditions: projected returns using

several forward-looking capital market assumptions, and

historical returns for the main asset classes dating back to 1970

or the earliest period for which historical data was readily

available for the asset classes included. Using long term

historical data allows us to capture multiple economic

environments, which we believe is relevant when using historical

returns. We place greater emphasis on the forward-looking

return and risk assumptions than on historical results. We use

the resulting projections to derive a base line expected rate of

return and risk level for the Cash Balance Plan’s prescribed asset

mix. We evaluate the portfolio based on: (1) the established

target asset allocations over short term (one-year) and longer

term (ten-year) investment horizons, and (2) the range of

148