Wells Fargo 2013 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

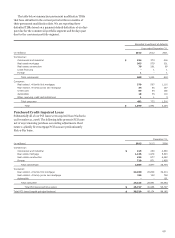

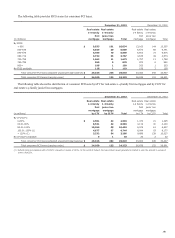

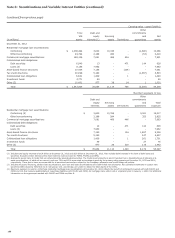

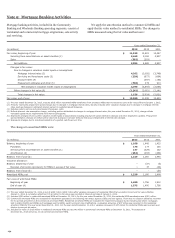

In the two preceding tables, “Total VIE assets” represents the

remaining principal balance of assets held by unconsolidated

VIEs using the most current information available. For VIEs that

obtain exposure to assets synthetically through derivative

instruments, the remaining notional amount of the derivative is

included in the asset balance. “Carrying value” is the amount in

our consolidated balance sheet related to our involvement with

the unconsolidated VIEs. “Maximum exposure to loss” from our

involvement with off-balance sheet entities, which is a required

disclosure under GAAP, is determined as the carrying value of

our involvement with off-balance sheet (unconsolidated) VIEs

plus the remaining undrawn liquidity and lending commitments,

the notional amount of net written derivative contracts, and

generally the notional amount of, or stressed loss estimate for,

other commitments and guarantees. It represents estimated loss

that would be incurred under severe, hypothetical

circumstances, for which we believe the possibility is extremely

remote, such as where the value of our interests and any

associated collateral declines to zero, without any consideration

of recovery or offset from any economic hedges. Accordingly,

this required disclosure is not an indication of expected loss.

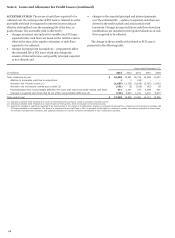

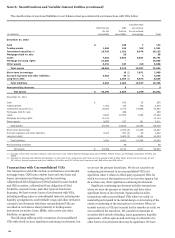

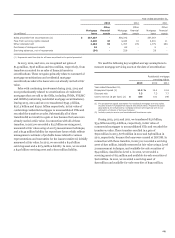

RESIDENTIAL MORTGAGE LOANS Residential mortgage loan

securitizations are financed through the issuance of fixed- or

floating-rate-asset-backed-securities, which are collateralized by

the loans transferred to a VIE. We typically transfer loans we

originated to these VIEs, account for the transfers as sales, retain

the right to service the loans and may hold other beneficial

interests issued by the VIEs. We also may be exposed to limited

liability related to recourse agreements and repurchase

agreements we make to our issuers and purchasers, which are

included in other commitments and guarantees. In certain

instances, we may service residential mortgage loan

securitizations structured by third parties whose loans we did

not originate or transfer. Our residential mortgage loan

securitizations consist of conforming and nonconforming

securitizations.

Conforming residential mortgage loan securitizations are

those that are guaranteed by GSEs, including GNMA. Because of

the power of the GSEs over the VIEs that hold the assets from

these conforming residential mortgage loan securitizations, we

do not consolidate them.

The loans sold to the VIEs in nonconforming residential

mortgage loan securitizations are those that do not qualify for a

GSE guarantee. We may hold variable interests issued by the

VIEs, primarily in the form of senior securities. We do not

consolidate the nonconforming residential mortgage loan

securitizations included in the table because we either do not

hold any variable interests, hold variable interests that we do not

consider potentially significant or are not the primary servicer

for a majority of the VIE assets.

Other commitments and guarantees include amounts related

to loans sold that we may be required to repurchase, or

otherwise indemnify or reimburse the investor or insurer for

losses incurred, due to material breach of contractual

representations and warranties as well as other retained

recourse arrangements. The maximum exposure to loss for

material breach of contractual representations and warranties

represents a stressed case estimate we utilize for determining

stressed case regulatory capital needs and is considered to be a

remote scenario.

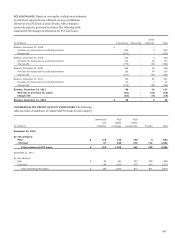

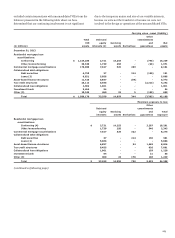

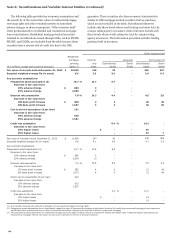

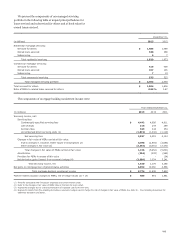

COMMERCIAL MORTGAGE LOAN SECURITIZATIONS

Commercial mortgage loan securitizations are financed through

the issuance of fixed- or floating-rate-asset-backed-securities,

which are collateralized by the loans transferred to the VIE. In a

typical securitization, we may transfer loans we originate to

these VIEs, account for the transfers as sales, retain the right to

service the loans and may hold other beneficial interests issued

by the VIEs. In certain instances, we may service commercial

mortgage loan securitizations structured by third parties whose

loans we did not originate or transfer. We typically serve as

primary or master servicer of these VIEs. The primary or master

servicer in a commercial mortgage loan securitization typically

cannot make the most significant decisions impacting the

performance of the VIE and therefore does not have power over

the VIE. We do not consolidate the commercial mortgage loan

securitizations included in the disclosure because we either do

not have power or do not have a variable interest that could

potentially be significant to the VIE.

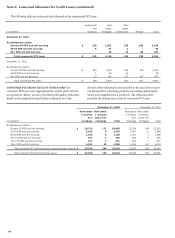

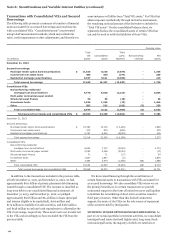

COLLATERALIZED DEBT OBLIGATIONS (CDOs) A CDO is a

securitization where a VIE purchases a pool of assets consisting

of asset-backed securities and issues multiple tranches of equity

or notes to investors. In some CDOs, a portion of the assets are

obtained synthetically through the use of derivatives such as

credit default swaps or total return swaps.

Prior to 2008, we engaged in the structuring of CDOs on

behalf of third party asset managers who would select and

manage the assets for the CDO. Typically, the asset manager has

some discretion to manage the sale of assets of, or derivatives

used by the CDO, which generally gives the asset manager the

power over the CDO. We have not structured these types of

transactions since the credit market disruption began in late

2007.

In addition to our role as arranger we may have other forms

of involvement with these CDOs, including ones established

prior to 2008. Such involvement may include acting as liquidity

provider, derivative counterparty, secondary market maker or

investor. For certain CDOs, we may also act as the collateral

manager or servicer. We receive fees in connection with our role

as collateral manager or servicer.

We assess whether we are the primary beneficiary of CDOs

based on our role in them in combination with the variable

interests we hold. Subsequently, we monitor our ongoing

involvement to determine if the nature of our involvement has

changed. We are not the primary beneficiary of these CDOs in

most cases because we do not act as the collateral manager or

servicer, which generally denotes power. In cases where we are

the collateral manager or servicer, we are not the primary

beneficiary because we do not hold interests that could

potentially be significant to the VIE.

COLLATERALIZED LOAN OBLIGATIONS (CLOs) A CLO is a

securitization where an SPE purchases a pool of assets consisting

of loans and issues multiple tranches of equity or notes to

187