Wells Fargo 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

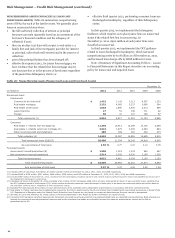

Risk Management – Credit Risk Management (continued)

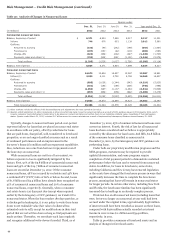

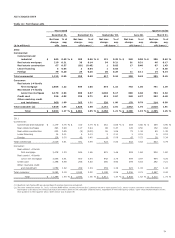

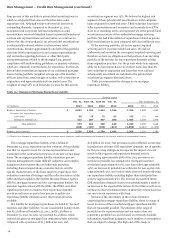

Table 36 presents net charge-offs for the four quarters and

full year of 2012 and 2011. Net charge-offs in 2012 were

$9.0 billion (1.17% of average total loans outstanding) compared

with $11.3 billion (1.49%) in 2011. Net charge-offs in 2012

included $888 million resulting from the OCC guidance issued

in third quarter 2012. Excluding the impact of this guidance, net

charge-offs in 2012 were $8.1 billion (1.05% of average total

loans outstanding), and total net charge-offs as a percentage of

average loans decreased in each of the four quarters of the year,

as we saw signs of stabilization in the housing market although

the economic recovery remained uneven.

Net charge-offs in the real estate 1-4 family first mortgage

portfolio totaled $2.9 billion in 2012, compared with $3.5 billion

a year ago.

Net charge-offs in the real estate 1-4 family junior lien

portfolio decreased $367 million to $3.2 billion in 2012. More

information about the home equity portfolio, which includes

substantially all of our real estate 1-4 family junior lien mortgage

loans, is available in Table 27 of this Report and the related

discussion.

Credit card net charge-offs decreased $282 million to

$916 million in 2012.

Commercial net charge-offs were $1.2 billion in 2012

compared with $2.0 billion in 2011, as market liquidity and

improving market conditions helped stabilize performance

results.

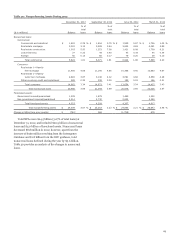

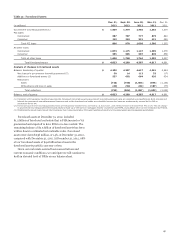

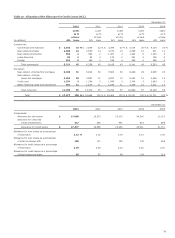

ALLOWANCE FOR CREDIT LOSSES The allowance for credit

losses, which consists of the allowance for loan losses and the

allowance for unfunded credit commitments, is management’s

estimate of credit losses inherent in the loan portfolio and

unfunded credit commitments at the balance sheet date,

excluding loans carried at fair value. The detail of the changes in

the allowance for credit losses by portfolio segment (including

charge-offs and recoveries by loan class) is in Note 6 (Loans and

Allowance for Credit Losses) to Financial Statements in this

Report.

We employ a disciplined process and methodology to

establish our allowance for credit losses each quarter. This

process takes into consideration many factors, including

historical and forecasted loss trends, loan-level credit quality

ratings and loan grade-specific loss factors. The process involves

subjective and complex judgments. In addition, we review a

variety of credit metrics and trends. These credit metrics and

trends, however, do not solely determine the amount of the

allowance as we use several analytical tools. For additional

information on our allowance for credit losses, see the “Critical

Accounting Policies – Allowance for Credit Losses” section,

Note 1 (Summary of Significant Accounting Policies) and Note 6

(Loans and Allowance for Credit Losses) to Financial Statements

in this Report.

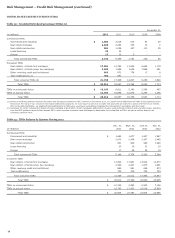

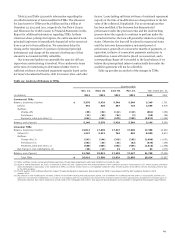

Table 37 presents an analysis of the allowance for credit

losses by loan segments and classes for the last five years.

72