Wells Fargo 2012 Annual Report Download - page 179

Download and view the complete annual report

Please find page 179 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

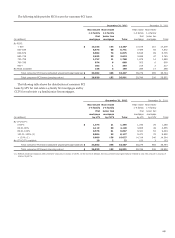

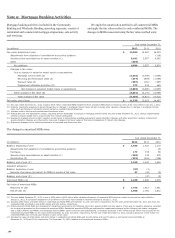

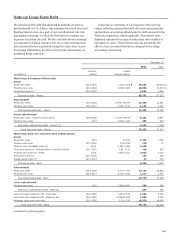

In addition to residential mortgage servicing rights (MSRs)

included in the previous table, we have a small portfolio of

commercial MSRs with a fair value of $1.4 billion at

December 31, 2012, and December 31, 2011. The nature of our

commercial MSRs, which are carried at LOCOM, is different

from our residential MSRs. Prepayment activity on serviced

loans does not significantly impact the value of commercial

MSRs because, unlike residential mortgages, commercial

mortgages experience significantly lower prepayments due to

certain contractual restrictions, impacting the borrower’s ability

to prepay the mortgage. Additionally, for our commercial MSR

portfolio, we are typically master/primary servicer, but not the

special servicer, who is separately responsible for the servicing

and workout of delinquent and foreclosed loans. It is the special

servicer, similar to our role as servicer of residential mortgage

loans, who is affected by higher servicing and foreclosure costs

due to an increase in delinquent and foreclosed loans.

Accordingly, prepayment speeds and costs to service are not key

assumptions for commercial MSRs as they do not significantly

impact the valuation. The primary economic driver impacting

the fair value of our commercial MSRs is forward interest rates,

which are derived from market observable yield curves used to

price capital markets instruments. Market interest rates most

significantly affect interest earned on custodial deposit balances.

The sensitivity of the current fair value to an immediate adverse

25% change in the assumption about interest earned on deposit

balances at December 31, 2012, and 2011, results in a decrease in

fair value of $139 million and $219 million, respectively. See

Note 9 for further information on our commercial MSRs.

The sensitivities in the preceding paragraph and table are

hypothetical and caution should be exercised when relying on

this data. Changes in value based on variations in assumptions

generally cannot be extrapolated because the relationship of the

change in the assumption to the change in value may not be

linear. Also, the effect of a variation in a particular assumption

on the value of the other interests held is calculated

independently without changing any other assumptions. In

reality, changes in one factor may result in changes in others (for

example, changes in prepayment speed estimates could result in

changes in the credit losses), which might magnify or counteract

the sensitivities.

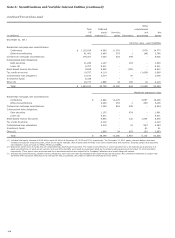

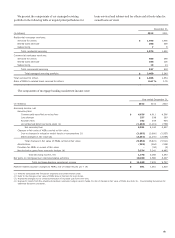

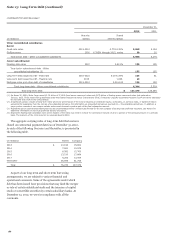

The following table presents information about the principal

balances of off-balance sheet securitized loans, including

residential mortgages sold to FNMA, FHLMC, GNMA and

securitizations where servicing is our only form of continuing

involvement. Delinquent loans include loans 90 days or more

past due and still accruing interest as well as nonaccrual loans.

In securitizations where servicing is our only form of continuing

involvement, we would only experience a loss if required to

repurchase a delinquent loan due to a breach in representations

and warranties associated with our loan sale or servicing

contracts.

Net charge-offs

Total loans Delinquent loans Year ended

December 31, December 31, December 31,

(in millions) 2012 2011 2012 2011 2012 2011

Commercial:

Real estate mortgage $ 128,564 137,121 12,216 11,142 541 569

Total commercial 128,564 137,121 12,216 11,142 541 569

Consumer:

Real estate 1-4 family first mortgage 1,283,504 1,171,666 21,574 24,235 1,170 1,506

Real estate 1-4 family junior lien mortgage 1 2 - - - 16

Other revolving credit and installment 2,034 2,271 110 131 - -

Total consumer 1,285,539 1,173,939 21,684 24,366 1,170 1,522

Total off-balance sheet securitized loans (1) $ 1,414,103 1,311,060 33,900 35,508 1,711 2,091

(1) At December 31, 2012 and 2011, the table includes total loans of $1.3 trillion and $1.2 trillion, respectively, and delinquent loans of $17.4 billion and $19.7 billion,

respectively for FNMA, FHLMC and GNMA. Net charge-offs exclude loans sold to FNMA, FHLMC and GNMA as we do not service or manage the underlying real estate upon

foreclosure and, as such, do not have access to net charge-off information.

177