Wells Fargo 2012 Annual Report Download - page 182

Download and view the complete annual report

Please find page 182 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

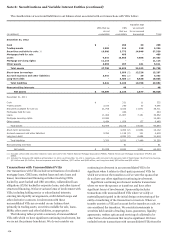

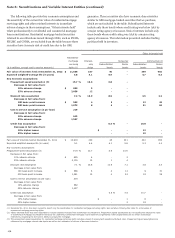

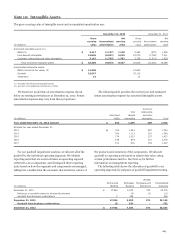

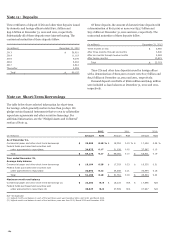

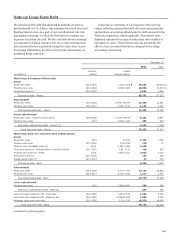

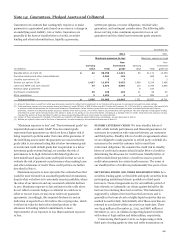

Note 9: Mortgage Banking Activities

Mortgage banking activities, included in the Community

Banking and Wholesale Banking operating segments, consist of

residential and commercial mortgage originations, sale activity

and servicing.

We apply the amortization method to all commercial MSRs

and apply the fair value method to only residential MSRs. The

changes in MSRs measured using the fair value method were:

Year ended December 31,

(in millions) 2012 2011 2010

Fair value, beginning of year $ 12,603 14,467 16,004

Adjustments from adoption of consolidation accounting guidance - - (118)

Servicing from securitizations or asset transfers (1) 5,182 3,957 4,092

Sales (293) - -

Net additions 4,889 3,957 3,974

Changes in fair value:

Due to changes in valuation model inputs or assumptions:

Mortgage interest rates (2) (2,092) (3,749) (1,944)

Servicing and foreclosure costs (3) (677) (694) (1,095)

Discount rates (4) (397) (150) (387)

Prepayment estimates and other (5) 273 913 469

Net changes in valuation model inputs or assumptions (2,893) (3,680) (2,957)

Other changes in fair value (6) (3,061) (2,141) (2,554)

Total changes in fair value (5,954) (5,821) (5,511)

Fair value, end of year $ 11,538 12,603 14,467

(1) The year ended December 31, 2012, includes $315 million residential MSRs transferred from amortized MSRs that we elected to carry at fair value effective January 1, 2012.

(2) Primarily represents prepayment speed changes due to changes in mortgage interest rates, but also includes other valuation changes due to changes in mortgage interest

rates (such as changes in estimated interest earned on custodial deposit balances).

(3) Includes costs to service and unreimbursed foreclosure costs.

(4) Reflects discount rate assumption change, excluding portion attributable to changes in mortgage interest rates; the year ended December 31, 2012, change predominantly

reflects increased capital return requirements from market participants.

(5) Represents changes driven by other valuation model inputs or assumptions including prepayment speed estimation changes and other assumption updates. Prepayment

speed estimation changes are influenced by observed changes in borrower behavior that occur independent of interest rate changes.

(6) Represents changes due to collection/realization of expected cash flows over time.

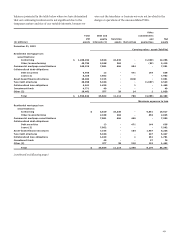

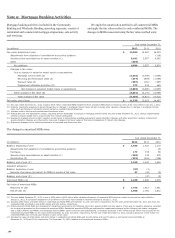

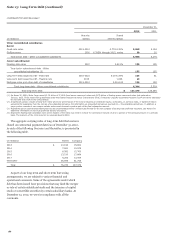

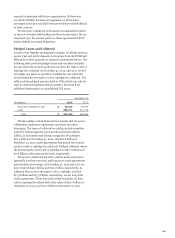

The changes in amortized MSRs were:

Year ended December 31,

(in millions) 2012 2011 2010

Balance, beginning of year $ 1,445 1,422 1,119

Adjustments from adoption of consolidation accounting guidance - - (5)

Purchases 177 155 58

Servicing from securitizations or asset transfers (1) (229) 132 478

Amortization (2) (233) (264) (228)

Balance, end of year (2) 1,160 1,445 1,422

Valuation allowance:

Balance, beginning of year (37) (3) -

Reversal of provision (provision) for MSRs in excess of fair value 37 (34) (3)

Balance, end of year (3) - (37) (3)

Amortized MSRs, net $ 1,160 1,408 1,419

Fair value of amortized MSRs:

Beginning of year $ 1,756 1,812 1,261

End of year (4) 1,400 1,756 1,812

(1) The year ended December 31, 2012, is net of $350 million ($313 million after valuation allowance) of residential MSRs that we elected to carry at fair value effective

January 1, 2012. A cumulative adjustment of $2 million to fair value was recorded in retained earnings at January 1, 2012.

(2) Includes $350 million and $400 million in residential amortized MSRs at December 31, 2011 and 2010, respectively. For the years ended December 31, 2011 and 2010, the

residential MSR amortization was $(50) million and $(5) million, respectively.

(3) Commercial amortized MSRs are evaluated for impairment purposes by the following risk strata: agency (GSEs) and non-agency. There was no valuation allowance recorded

for the periods presented on the commercial amortized MSRs. Residential amortized MSRs are evaluated for impairment purposes by the following risk strata: mortgages

sold to GSEs (FHLMC and FNMA) and mortgages sold to GNMA, each by interest rate stratifications. A valuation allowance of $37 million and $3 million was recorded on the

residential amortized MSRs for the years ended December 31, 2011 and 2010, respectively. For the year ended December 31, 2012, valuation allowance of $37 million for

residential MSRs was reversed upon election to carry at fair value.

(4) Includes fair value of $316 million and $441 million in residential amortized MSRs and $1,440 million and $1,371 million in commercial amortized MSRs at

December 31, 2011 and 2010, respectively. The December 31, 2012, balance is all commercial amortized MSRs.

180