Wells Fargo 2012 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

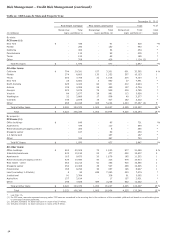

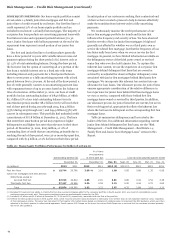

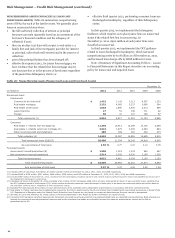

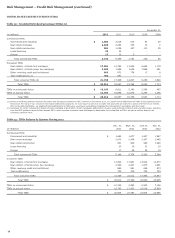

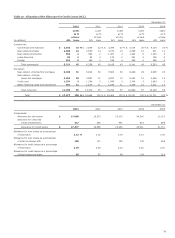

Risk Management – Credit Risk Management (continued)

NONPERFORMING ASSETS (NONACCRUAL LOANS AND

FORECLOSED ASSETS) Table 28 summarizes nonperforming

assets (NPAs) for each of the last five years. We generally place

loans on nonaccrual status when:

x the full and timely collection of interest or principal

becomes uncertain (generally based on an assessment of the

borrower’s financial condition and the adequacy of

collateral, if any);

x they are 90 days (120 days with respect to real estate 1-4

family first and junior lien mortgages) past due for interest

or principal, unless both well-secured and in the process of

collection;

x part of the principal balance has been charged off;

x effective first quarter 2012, for junior lien mortgages, we

have evidence that the related first lien mortgage may be

120 days past due or in the process of foreclosure regardless

of the junior lien delinquency status; or

x effective third quarter 2012, performing consumer loans are

discharged in bankruptcy, regardless of their delinquency

status.

In first quarter 2012, we implemented the Interagency

Guidance, which requires us to place junior liens on nonaccrual

status if the related first lien is nonaccruing. At

December 31, 2012, $960 million of such junior liens were

classified as nonaccrual.

In third quarter 2012, we implemented the OCC guidance

related to loans discharged in bankruptcy, which increased

nonperforming assets by $1.8 billion as of December 31, 2012,

and increased loan charge-offs by $888 million for 2012.

Note 1 (Summary of Significant Accounting Policies – Loans)

to Financial Statements in this Report describes our accounting

policy for nonaccrual and impaired loans.

Table 28: Nonperforming Assets (Nonaccrual Loans and Foreclosed Assets)

December 31,

(in millions) 2012 2011 2010 2009 2008

Nonaccrual loans:

Commercial:

Commercial and industrial $ 1,422 2,142 3,213 4,397 1,253

Real estate mortgage 3,322 4,085 5,227 3,696 594

Real estate construction 1,003 1,890 2,676 3,313 989

Lease financing 27 53 108 171 92

Foreign 50 47 127 146 57

Total commercial (1) 5,824 8,217 11,351 11,723 2,985

Consumer:

Real estate 1-4 family first mortgage (2) 11,455 10,913 12,289 10,100 2,648

Real estate 1-4 family junior lien mortgage (3) 2,922 1,975 2,302 2,263 894

Other revolving credit and installment 285 199 300 332 273

Total consumer (4) 14,662 13,087 14,891 12,695 3,815

Total nonaccrual loans (5)(6)(7) 20,486 21,304 26,242 24,418 6,800

As a percentage of total loans 2.56 % 2.77 3.47 3.12 0.79

Foreclosed assets:

Government insured/guaranteed (8) $ 1,509 1,319 1,479 960 667

Non-government insured/guaranteed 2,514 3,342 4,530 2,199 1,526

Total foreclosed assets 4,023 4,661 6,009 3,159 2,193

Total nonperforming assets $ 24,509 25,965 32,251 27,577 8,993

As a percentage of total loans 3.07 % 3.37 4.26 3.52 1.04

(1)

Includes LHFS of $16 million, $25 million, $3 million and $27 million at December 31, 2012, 2011, 2010, and 2009 respectively.

(2) Includes MHFS of $336 million, $301 million, $426 million, $339 million, and $193 million at December 31, 2012, 2011, 2010, 2009, and 2008 respectively.

(3) Includes $960 million at December 31, 2012, resulting from the Interagency Guidance issued in 2012 which requires performing junior liens to be classified as nonaccrual if

the related first mortgage is nonaccruing.

(4) Includes $1.8 billion at December 31, 2012 consisting of $1.4 billion of first mortgages, $205 million of junior liens and $140 million of auto and other loans, resulting from

the OCC guidance issued in third quarter 2012, which requires performing consumer loans discharged in bankruptcy to be placed on nonaccrual status and written down to

net realizable collateral value, regardless of their delinquency status.

(5) Excludes PCI loans because they continue to earn interest income from accretable yield, independent of performance in accordance with their contractual terms.

(6) Real estate 1-4 family mortgage loans predominantly insured by the FHA or guaranteed by the VA and student loans predominantly guaranteed by agencies on behalf of the

U.S. Department of Education under the Federal Family Education Loan Program are not placed on nonaccrual status because they are insured or guaranteed.

(7) See Note 6 (Loans and Allowance for Credit Losses) to Financial Statements in this Report for further information on impaired loans.

(8) Consistent with regulatory reporting requirements, foreclosed real estate securing government insured/guaranteed loans are classified as nonperforming. Both principal and

interest for government insured/guaranteed loans secured by the foreclosed real estate are collectible because the loans are predominantly insured by the FHA or

guaranteed by the VA.

64