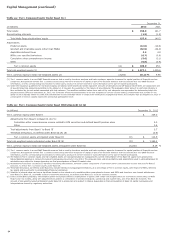

Wells Fargo 2012 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

Critical Accounting Policies (continued)

x Level 1 – Valuation is based upon quoted prices for identical

instruments traded in active markets. Level 1 instruments

include securities traded on active exchange markets, such

as the New York Stock Exchange, as well as U.S. Treasury

and other U.S. government securities that are traded by

dealers or brokers in active OTC markets.

x Level 2 – Valuation is based upon quoted prices for similar

instruments in active markets, quoted prices for identical or

similar instruments in markets that are not active, and

model-based valuation techniques, such as matrix pricing,

for which all significant assumptions are observable in the

market. Level 2 instruments include securities traded in

functioning dealer or broker markets, plain-vanilla interest

rate derivatives and MHFS that are valued based on prices

for other mortgage whole loans with similar characteristics.

x Level 3 – Valuation is generated primarily from techniques

that use significant assumptions not observable in the

market. These unobservable assumptions reflect our own

estimates of assumptions market participants would use in

pricing the asset or liability. Valuation techniques include

use of option pricing models, discounted cash flow models

and similar techniques.

When developing fair value measurements, we maximize the

use of observable inputs and minimize the use of unobservable

inputs. When available, we use quoted prices in active markets to

measure fair value. If quoted prices in active markets are not

available, fair value measurement is based upon models that use

primarily market-based or independently sourced market

parameters, including interest rate yield curves, prepayment

speeds, option volatilities and currency rates. However, in

certain cases, when market observable inputs for model-based

valuation techniques are not readily available, we are required to

make judgments about assumptions market participants would

use to estimate fair value.

The degree of management judgment involved in

determining the fair value of a financial instrument is dependent

upon the availability of quoted prices in active markets or

observable market parameters. For financial instruments with

quoted market prices or observable market parameters in active

markets, there is minimal subjectivity involved in measuring fair

value. When quoted prices and observable data in active markets

are not fully available, management judgment is necessary to

estimate fair value. Changes in the market conditions, such as

reduced liquidity in the capital markets or changes in secondary

market activities, may reduce the availability and reliability of

quoted prices or observable data used to determine fair value.

When significant adjustments are required to price quotes or

inputs, it may be appropriate to utilize an estimate based

primarily on unobservable inputs. When an active market for a

financial instrument does not exist, the use of management

estimates that incorporate current market participant

expectations of future cash flows, adjusted for an appropriate

risk premium, is acceptable.

When markets for our financial assets and liabilities become

inactive because the level and volume of activity has declined

significantly relative to normal conditions, it may be appropriate

to adjust quoted prices. The methodology we use to adjust the

quoted prices generally involves weighting the quoted prices and

results of internal pricing techniques, such as the net present

value of future expected cash flows (with observable inputs,

where available) discounted at a rate of return market

participants require to arrive at the fair value. The more active

and orderly markets for particular security classes are

determined to be, the more weighting we assign to quoted prices.

The less active and orderly markets are determined to be, the less

weighting we assign to quoted prices.

We may use third party pricing services and brokers

(collectively, “pricing vendors”) to obtain fair values (“vendor

prices”) which are used to either record the price of an

instrument or to corroborate internally developed prices. We

have processes in place to approve such vendors to ensure

information obtained and valuation techniques used are

appropriate. Once these vendors are approved to provide pricing

information, we monitor and review the results to ensure the fair

values are reasonable and in line with market experience with

similar asset classes. For certain securities, we may use internal

traders to price instruments. Where vendor prices are utilized for

recording the price of an instrument, we determine the most

appropriate and relevant pricing vendor for each security class

and obtain a price from that particular pricing vendor for each

security.

Determination of the fair value of financial instruments using

either vendor prices or internally developed prices are subject to

our internal price validation procedures, which include, but are

not limited to, one or a combination of the following procedures:

x comparison to pricing vendors (for internally developed

prices) or to other pricing vendors (for vendor developed

prices);

x variance analysis of prices;

x corroboration of pricing by reference to other independent

market data such as secondary broker quotes and relevant

benchmark indices;

x review of pricing by Company personnel familiar with

market liquidity and other market-related conditions; and

x investigation of prices on a specific instrument-by-

instrument basis.

For instruments where we utilize vendor prices to record the

price of an instrument, we perform additional procedures. We

evaluate pricing vendors by comparing prices from one vendor to

prices of other vendors for identical or similar instruments and

evaluate the consistency of prices to known market transactions

when determining the level of reliance to be placed on a

particular pricing vendor. Methodologies employed and inputs

used by third party pricing vendors are subject to additional

review when such services are provided. This review may consist

of, in part, obtaining and evaluating control reports issued and

pricing methodology materials distributed.

Significant judgment is required to determine whether

certain assets measured at fair value are included in Level 2 or

Level 3. When making this judgment, we consider available

information, including observable market data, indications of

market liquidity and orderliness, and our understanding of the

valuation techniques and significant inputs used. For securities

in inactive markets, we use a predetermined percentage to

evaluate the impact of fair value adjustments derived from

100