Wells Fargo 2012 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

|

|

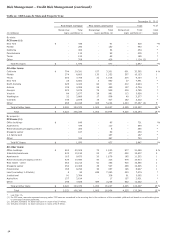

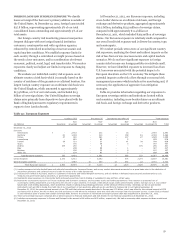

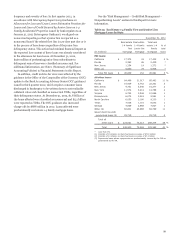

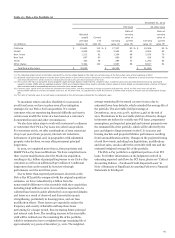

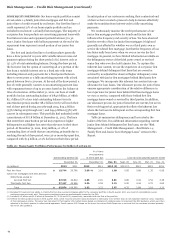

Risk Management – Credit Risk Management (continued)

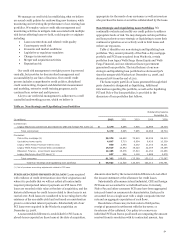

difference between these amounts is absorbed by the

nonaccretable difference. This removal method assumes

that the amount received from resolution approximates pool

performance expectations. The accretable yield percentage is

unaffected by the resolution and any changes in the effective

yield for the remaining loans in the pool are addressed by our

quarterly cash flow evaluation process for each pool. For loans

that are resolved by payment in full, there is no release of the

nonaccretable difference for the pool because there is no

difference between the amount received at resolution and the

contractual amount of the loan. Modified PCI loans are not

removed from a pool even if those loans would otherwise be

deemed TDRs. Modified PCI loans that are accounted for

individually are TDRs, and removed from PCI accounting, if

there has been a concession granted in excess of the original

nonaccretable difference. We include these TDRs in our

impaired loans.

During 2012, we recognized as income $85 million released

from the nonaccretable difference related to commercial PCI

loans due to payoffs and other resolutions. We also transferred

$1.1 billion from the nonaccretable difference to the accretable

yield for PCI loans with improving credit-related cash flows and

absorbed $2.5 billion of losses in the nonaccretable difference

from loan resolutions and write-downs. Our cash flows expected

to be collected have been favorably affected by lower expected

defaults and losses as a result of observed economic

strengthening, particularly in housing prices, and our loan

modification efforts. See the “Real Estate 1-4 Family First and

Junior Lien Mortgage Loans” section in this Report for

additional information. These factors led to the reduction in

expected losses on PCI loans, primarily Pick-a-Pay, which

resulted in a reclassification from nonaccretable difference to

accretable yield in 2012, which has also occurred in prior years.

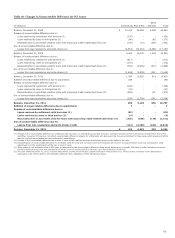

Table 18 provides an analysis of changes in the nonaccretable

difference.

52