Wells Fargo 2012 Annual Report Download - page 181

Download and view the complete annual report

Please find page 181 of the 2012 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

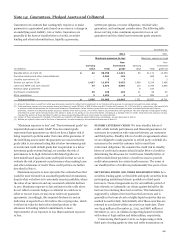

|

|

of commercial paper issued by the conduit and is described

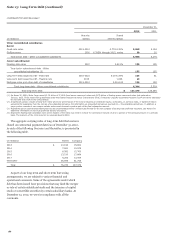

further below.

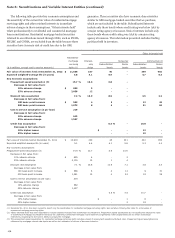

MUNICIPAL TENDER OPTION BOND SECURITIZATIONS As part

of our normal portfolio investment activities, we consolidate

municipal bond trusts that hold highly rated, long-term, fixed-

rate municipal bonds, the majority of which are rated AA or

better. Our residual interests in these trusts generally allow us to

capture the economics of owning the securities outright, and

constructively make decisions that significantly impact the

economic performance of the municipal bond vehicle, primarily

by directing the sale of the municipal bonds owned by the

vehicle. In addition, the residual interest owners have the right

to receive benefits and bear losses that are proportional to

owning the underlying municipal bonds in the trusts. The trusts

obtain financing by issuing floating-rate trust certificates that

reprice on a weekly or other basis to third-party investors. Under

certain conditions, if we elect to terminate the trusts and

withdraw the underlying assets, the third party investors are

entitled to a small portion of any unrealized gain on the

underlying assets. We may serve as remarketing agent and/or

liquidity provider for the trusts. The floating-rate investors have

the right to tender the certificates at specified dates, often with

as little as seven days’ notice. Should we be unable to remarket

the tendered certificates, we are generally obligated to purchase

them at par under standby liquidity facilities unless the bond’s

credit rating has declined below investment grade or there has

been an event of default or bankruptcy of the issuer and insurer.

NONCONFORMING RESIDENTIAL MORTGAGE LOAN

SECURITIZATIONS We have consolidated certain of our

nonconforming residential mortgage loan securitizations in

accordance with consolidation accounting guidance. We have

determined we are the primary beneficiary of these

securitizations because we have the power to direct the most

significant activities of the entity through our role as primary

servicer and also hold variable interests that we have determined

to be significant. The nature of our variable interests in these

entities may include beneficial interests issued by the VIE,

mortgage servicing rights and recourse or repurchase reserve

liabilities. The beneficial interests issued by the VIE that we hold

include either subordinate or senior securities held in an amount

that we consider potentially significant.

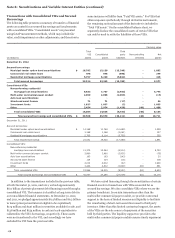

MULTI-SELLER COMMERCIAL PAPER CONDUIT We administer

a multi-seller asset-based commercial paper conduit that

finances certain client transactions. This conduit is a bankruptcy

remote entity that makes loans to, or purchases certificated

interests, generally from SPEs, established by our clients

(sellers) and which are secured by pools of financial assets. The

conduit funds itself through the issuance of highly rated

commercial paper to third party investors. The primary source of

repayment of the commercial paper is the cash flows from the

conduit’s assets or the re-issuance of commercial paper upon

maturity. The conduit’s assets are structured with deal-specific

credit enhancements generally in the form of

overcollateralization provided by the seller, but may also include

subordinated interests, cash reserve accounts, third party credit

support facilities and excess spread capture. The timely

repayment of the commercial paper is further supported by

asset-specific liquidity facilities in the form of liquidity asset

purchase agreements that we provide. Each facility is equal to

102% of the conduit’s funding commitment to a client. The

aggregate amount of liquidity must be equal to or greater than

all the commercial paper issued by the conduit. At the discretion

of the administrator, we may be required to purchase assets

from the conduit at par value plus accrued interest or discount

on the related commercial paper, including situations where the

conduit is unable to issue commercial paper. Par value may be

different from fair value.

We receive fees in connection with our role as administrator

and liquidity provider. We may also receive fees related to the

structuring of the conduit’s transactions. We are the primary

beneficiary of the conduit because we have power over the

significant activities of the conduit and have a significant

variable interest due to our liquidity arrangement.

INVESTMENT FUNDS We have consolidated certain of our

investment funds where we manage the assets of the fund and

our interests absorb a majority of the funds’ variability. We

consolidate these VIEs because we have discretion over the

management of the assets and are the sole investor in these

funds.

179