Vodafone 2009 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

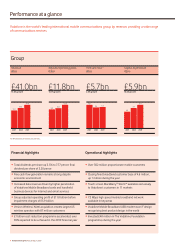

Vodafone Group Plc Annual Report 2009 7

include bundled mobile data and fixed broadband options. SuperFlat net

additions have remained strong at 404,000 in the last quarter. Similar

concepts of value enhancement products have been launched in most

European markets, including Italy, Spain, the UK and Ireland.

We have accelerated our £1 billion cost reduction programme, which

will help us to of fset the pressures of cost inflation and the competitive

environment and invest in revenue growth opportunities. In the 2009

financial year, we achieved approximately £200 million of cost savings,

which were partially offset by restructuring charges. We now intend to

deliver at least 65% of the total programme in the 2010 financial year,

ahead of plan. The benefits of the programme are visible in our results.

In the 2009 financial year, despite significant increases in mobile voice

minutes and data usage, Europe’s operating expenses remained

broadly flat and mobile contribution margins were stable.

Since November 2008: we have established the Vodafone Roaming

Services business unit, which will manage international wholesale

roaming activities across the Group; we have outsourced our field

network maintenance operations in the UK; and we have executed

network sharing arrangements across Germany, Ireland, Spain and

the UK.

We are reviewing our programme to identify further ways in which the

Group can benefit from its regional scale and further reduce costs

in order to offset external pressures and competitor action and invest

in growth.

Pursue growth opportunities in total communications

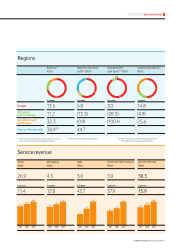

Data revenue grew by 25.9% on an organic basis and is now over

£3 billion. We continue to push penetration of handheld business

and PC connectivity devices. In April, Verizon Wireless joined the

Joint Innovation Lab (‘JIL’) established by Vodafone, China Mobile and

SoftBank. The JIL is creating a single platform for developers to create

mobile widgets and applications on multiple operating systems and

access the partners’ combined 1.1 billion customer base. Vodafone

will also provide access to third parties to billing, location and other

platforms, to enhance user experience and create a favourable

environment for all.

In fixed broadband, we have continued to grow our customer base in

Italy and Spain, and in Germany, returned to revenue growth in the

fourth quarter. We now have 4.6 million customers, an increase of

around 1 million during the year, of which 0.6 million arose in the

second half. The addition of appropriate quality fixed broadband

capability is increasing the range of products we can offer to

customers, in particular in enterprise, and providing us with the ability

to compete with integrated competitors.

Europe’s enterprise revenue grew by 1.2% during the year, ahead of

overall business trends, demonstrating the progress we are making to

address the enterprise opportunity. Vodafone Global Enterprise, which

serves our larger enterprise customers on a Group-wide basis,

delivered revenue growth of around 9%, demonstrating the appeal of

Vodafone to multinational corporations.

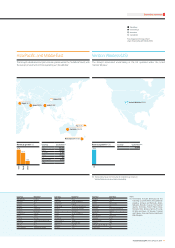

Execute in emerging markets

We have continued to drive penetration in India, generating strong

revenue growth from our brand and commercial offers and a substantial

investment in network coverage. Indus Towers, our infrastructure joint

venture with Bharti and Idea, began operating during the financial year.

We expect Indus Towers will enable Vodafone to increase its capital

efficiency in India and also to benefit from revenue generated from

selling capacity to other operators. Growth at Vodacom, which has

strengthened its total communications offering through the acquisition

of Gateway, has been strong. Our performance in Turkey, where we

remain focused on our turnaround plan, has been disappointing. We will

continue to invest throughout the 2010 financial year to relaunch the

company. In Qatar, the Group commenced operations after the end of

the financial year, having been awarded the second licence with its

partner, the Qatar Foundation, during the year. In August 2008, the

Group acquired 70.0% of Ghana Telecommunications, an integrated

mobile and fixed line telecommunications operator, which has since

been rebranded to Vodafone.

Whilst emerging markets are of interest to us, we remain cautious and

selective on future expansion. Our primary focus will remain on driving

results from our existing assets.

Strengthen capital discipline

During the year we returned approximately 87% of free cash flow

before licence and spectrum payments to shareholders in the form of

dividends and share buy backs. Net debt has increased to £34 billion,

primarily as a result of foreign currency movements. The Group has

retained a low single A credit rating in line with its target.

In February 2009, consistent with our active stance on in-market

consolidation, we agreed to merge Vodafone Australia with Hutchison

3G Australia to create a new jointly owned company which will operate

under the Vodafone brand. This transaction, which is subject to

regulatory approval, is expected to generate cost synergies with a

present value of AUS$2 billion and will release capital to Vodafone

through a AUS$0.5 billion deferred payment. Customers in Australia

will benefit from the enlarged entity’s scale.

Prospects for the year ahead

In Europe and Central Europe, operating conditions will be challenging in

the 2010 financial year. IMF forecasts indicate a GDP decline of 4% in 2009

across the Vodafone footprint within Europe and Central Europe and that

unemployment could increase significantly. In these markets, we expect

that voice and messaging revenue trends will continue as a result of

ongoing pricing pressures and slowing usage. However, we expect further

growth in data revenue. In Turkey, where we will focus on our turnaround

plan, we expect that the 2010 financial year will be challenging. Revenue

growth in other emerging markets, in particular India and Africa, is

expected to continue as we drive penetration in these markets. We expect

another year of good performance at Verizon Wireless.

Adjusted operating profit is expected to be in the range of £11.0 billion to

£11.8 billion. We have widened our outlook for adjusted operating profit

this year to reflect current economic uncertainty. Performance will be

determined by actual economic trends, our success in closing the

performance gaps we have identified in certain markets and the extent

to which we decide to reinvest cost savings into total communications

growth opportunities. Underlying EBITDA margins, before the impact of

acquisitions and disposals, foreign exchange and business mix, are

expected to decline by a similar amount to the 2009 financial year. This

trend reflects the benefit of the acceleration of the Group’s cost savings

programme in a weaker revenue environment. Overall Group EBITDA

margin is expected to decline at a slightly slower rate.

Free cash flow before licence and spectrum payments is expected to be

in the range of £6.0 billion to £6.5 billion, ahead of our medium term

target to deliver between £5.0 and £6.0 billion annual free cash flow. We

intend to maintain European capital intensity at around 10% of revenue

and to continue to invest significantly in India. Capital expenditure is

expected to be similar to last year after adjusting for foreign currency.

Summary

Overall, these results reflect the benefits of Vodafone’s exposure to a

diverse range of economies, our successful exploitation of data services

and the opportunities derived from our regional approach, as well as the

initial impact of our accelerated £1 billion cost savings programme.

We are confident that our strategy is appropriate for the current

operating environment.

Vittorio Colao

Chief Executive

87% of free cash

flow before licence

and spectrum

payments returned

to shareholders

Executive summary