Vodafone 2009 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148

|

|

138 Vodafone Group Plc Annual Report 2009

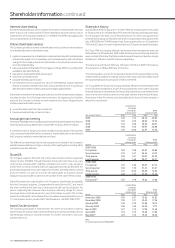

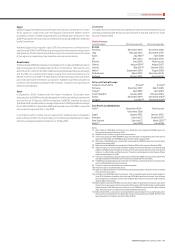

EBITDA

EBITDA is operating profit excluding share in results of associates, depreciation and amortisation, gains/losses on the disposal of fixed assets, impairment losses and other

operating income and expense. The Group uses EBITDA, in conjunction with other GAAP and non-GAAP financial measures such as adjusted operating profit, operating

profit and net profit, to assess its operating performance. The Group believes that EBITDA is an operating performance measure, not a liquidity measure, as it includes non-

cash changes in working capital and is reviewed by the Group Chief Executive to assess internal performance in conjunction with EBITDA margin, which is an alternative

sales margin figure. The Group believes that it is both useful and necessary to report EBITDA as a performance measure as it enhances the comparability of profit

across segments.

Because EBITDA does not take into account certain items that affect operations and performance, EBITDA has inherent limitations as a performance measure. To compensate

for these limitations, the Group analyses EBITDA in conjunction with other GAAP and non-GAAP operating performance measures. EBITDA should not be considered in

isolation or as a substitute for a GAAP measure of operating performance.

A reconciliation of EBITDA to the respective closest equivalent GAAP measure, operating profit/(loss), is provided in “Operating results” beginning on page 25.

Group adjusted operating prot and adjusted earnings per share

Group adjusted operating profit excludes non-operating income of associates, impairment losses and other income and expense. Adjusted earnings per share also excludes

changes in fair value of equity put rights and similar arrangements and certain foreign exchange differences, together with related tax effects. The Group believes that it is both

useful and necessary to report these measures for the following reasons:

these measures are used by the Group for internal performance analysis; •

these measures are used in setting director and management remuneration; and•

they are useful in connection with discussion with the investment analyst community and debt rating agencies.•

Reconciliation of adjusted operating profit and adjusted earnings per share to the respective closest equivalent GAAP measure, operating profit/(loss) and basic earnings/

(loss) per share, is provided in “Operating results” beginning on page 25.

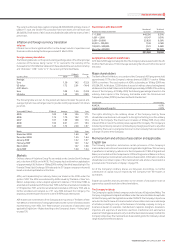

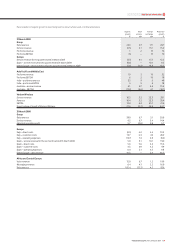

Cash ow measures

In presenting and discussing the Group’s reported results, free cash flow and operating free cash flow are calculated and presented even though these measures are not

recognised within International Financial Reporting Standards (‘IFRS’). The Group believes that it is both useful and necessary to communicate free cash flow to investors

and other interested parties, for the following reasons:

free cash flow allows the Company and external parties to evaluate the Group’s liquidity and the cash generated by the Group’s operations. Free cash flow does not include •

items determined independently of the ongoing business, such as the level of dividends, and items which are deemed discretionary, such as cash flows relating to

acquisitions and disposals or financing activities. In addition, it does not necessarily reflect the amounts which the Group has an obligation to incur. However, it does

reflect the cash available for such discretionary activities, to strengthen the consolidated balance sheet or to provide returns to shareholders in the form of dividends or

share purchases;

free cash flow facilitates comparability of results with other companies, although the Group’s measure of free cash flow may not be directly comparable to similarly titled •

measures used by other companies;

these measures are used by management for planning, reporting and incentive purposes; and•

these measures are useful in connection with discussion with the investment analyst community and debt rating agencies.•

A reconciliation of net cash inflow from operating activities, the closest equivalent GAAP measure, to operating free cash flow and free cash flow, is provided in “Financial

position and resources” on page 41.

Other

Certain of the statements within the section titled “Chief Executive’s review” on pages 6 to 7 contain forward-looking non-GAAP financial information for which at this time

there is no comparable GAAP measure and which at this time cannot be quantitatively reconciled to comparable GAAP financial information.

Certain of the statements within the section titled “Outlook” on page 37 contain forward-looking non-GAAP financial information which at this time cannot be quantitatively

reconciled to comparable GAAP financial information.

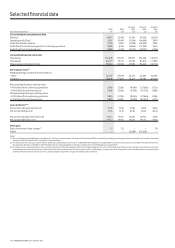

Organic growth

The Group believes that “organic growth”, which is not intended to be a substitute, or superior to, reported growth, provides useful and necessary information to investors

and other interested parties for the following reasons:

it provides additional information on underlying growth of the business without the effect of factors unrelated to the operating performance of the business;•

it is used by the Group for internal performance analysis; and•

it facilitates comparability of underlying growth with other companies, although the term “organic” is not a defined term under IFRS and may not, therefore, •

be comparable with similarly titled measures reported by other companies.

Non-GAAP information