Vodafone 2009 Annual Report Download - page 32

Download and view the complete annual report

Please find page 32 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

30 Vodafone Group Plc Annual Report 2009

Operating results continued

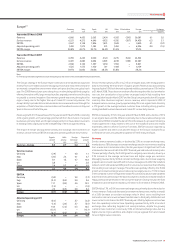

India

Revenue grew by 33% on a pro forma basis, with growth in the fourth quarter of 27.7%

at constant exchange rates. Growth in the fourth quarter remained stable in

comparison to the third quarter as the eight percentage point benefit of the new

revenue stream from the network sharing joint venture, Indus Towers, which

launched during the first half of the year, offset the slowing underlying growth rate.

Visitor revenue increased, albeit at a lower rate, due to the impact of economic

pressures as people travel less. Lower effective rates per minute reflecting price

reductions earlier in the year, coupled with the continued market shift to lifetime

validity prepaid offerings, led to a reduction in customer churn. The lower effective

rate and a slight fall in usage per customer were mitigated by net customer additions,

which averaged 2.1 million per month, and the launch of services in seven new circles,

bringing the closing customer base to 68.8 million. Customer penetration in the

Indian mobile market reached 34% at 31 March 2009.

EBITDA grew by 5% on a pro forma basis. Customer costs as a percentage of revenue

decreased, benefiting from economies of scale. Licensing costs increased as

discounts received from the regulator in some service areas were terminated.

Network expansion continued, with an average of 2,600 base stations constructed

per month, primarily in the new circles. Site sharing increased and Indus Towers

steadily increased its operations throughout the rest of the year, with 95,000 sites

under its management at the end of March 2009.

Other Asia Pacific and Middle East

The organic increase in service revenue of 8.5% was attributable to performances in

Egypt and Australia. In Egypt, service revenue grew by 11.9% at constant exchange

rates, as growth in the customer base and increased usage per customer were partially

offset by a decline in the effective rate per minute as a result of the introduction of new

tariffs in addition to lower termination rates and a fall in both visitor revenue and the

enterprise segment revenue as people travelled less. Service revenue in Australia

increased by 6.1% on an organic basis, due to an increase in the average customer base

and good data revenue growth, especially in mobile broadband services. These were

partially offset by lower ARPU, reflecting strong competition, which led to a lower

revenue growth rate in the fourth quarter. In New Zealand, service revenue grew by

4.9% at constant exchange rates, a result of an increase in the fixed broadband cus tomer

base and growth in data services, the latter following increased penetration of mobile

PC connectivity devices. These benefits were partially offset by the competitive and

recessionary trends in the market.

EBITDA grew organically by 7.3%, with a decline in the EBITDA margin, as the increase

in Egypt was offset by the decline in Australia. Egypt’s EBITDA grew by 15.9% at constant

exchange rates in proportion to revenue, with a slight increase in margin, despite the

inclusion of 3G licensing fees for the full year in comparison to only part of the prior year.

In Australia, EBITDA decreased by 17.6% on an organic basis, primarily due to a loss

provision related to a prepaid recharge vendor and an increased focus on contract

customers resulting in higher customer costs.

In February 2009, the Group and Hutchison Telecommunications (Australia) Limited

agreed to merge their Australian operations to form a 50:50 joint venture. The

transaction is expected to complete in the first half of the 2010 financial year. Following

completion, the joint venture will be proportionately consolidated.

On 10 May 2009, Vodafone Qatar completed a public offering of 40% of its authorised

share capital, raising QAR 3.4 billion (£0.6 billion). The shares are expected to be listed

on the Doha securities market by July 2009.

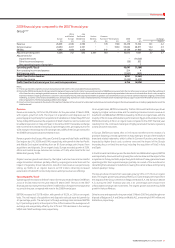

Verizon Wireless

2009 2008 % change

£m £m £ Organic

Revenue 14,085 10,144 38.9 10.4

Service revenue 12,862 9,246 39.1 10.5

EBITDA 5,543 3,930 41.0 13.0

Interest (217) (102) 100+

Tax(1) (198) (166) 19.3

Minority interest (78) (56) 39.3

Discontinued operations 57 – –

Group share of result in

Verizon Wireless 3,542 2,447 44.7 21.6

Note:

(1) The Group’s share of the tax attributable to Verizon Wireless relates only to the corporate entities

held by the Verizon Wireless partnership and certain state taxes which are levied on the

partnership. The tax attributable to the Group’s share of the partnership’s pre-tax profit is

included within the Group tax charge.

Verizon Wireless, the Group’s associated undertaking in the US, achieved 5.6 million

net customer additions in a market where penetration reached an estimated 92%

at 31 March 2009. The increased closing customer base of 86.6 million was

achieved through continued strong organic growth, the acquisitions of Rural

Cellular Corporation and Alltel, combined with concentration on the high value

contract segment and market leading customer loyalty as evidenced by low

customer churn.

Service revenue growth was 10.5% on an organic basis, driven by the expanding

customer base and robust messaging and data ARPU. Messaging and data revenue

continued to increase strongly, predominantly as a result of growth in data card,

email and messaging services. Verizon Wireless continued to extend the reach

of its 3G network, which now covers more than 280 million people after the

Alltel acquisition.

Verizon Wireless improved its EBITDA margin to 39.4% through efficiencies in

operating expenses partly offset by a higher level of customer acquisition and

retention costs, driven by increased demand for high end data devices such as the

BlackBerry Storm.

Verizon Wireless completed the acquisition of Rural Cellular Corporation in the first

half of the financial year, adding 0.7 million customers. On 9 January 2009, Verizon

Wireless completed its acquisition of Alltel, purchasing Alltel’s equity and acquiring

and repaying Alltel’s debt with Verizon Wireless and Alltel cash as well as the proceeds

from capital market transactions. The Alltel acquisition added 13.2 million customers

before required divestitures. Verizon Wireless expects to realise synergies with a net

present value, after integration costs, of more than US$9 billion, driven by aggregate

capital and operating expense savings. Increased debt in relation to the acquisition

of Alltel led to a £150 million interest charge for the quarter ended 31 March 2009.

As part of regulatory approval for the Alltel acquisition, Verizon Wireless is required

to divest overlapping properties in 105 markets, corresponding to 2.2 million

customers. On 8 May 2009, Verizon Wireless announced an agreement with AT&T,

which will acquire the network assets and mobile licences of 79 of these markets,

corresponding to 1.5 million of these customers, for $2.35 billion.