Vodafone 2009 Annual Report Download - page 120

Download and view the complete annual report

Please find page 120 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

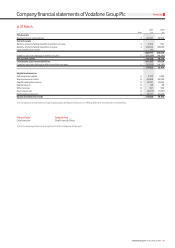

118 Vodafone Group Plc Annual Report 2009

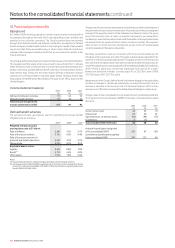

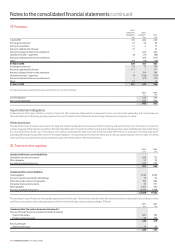

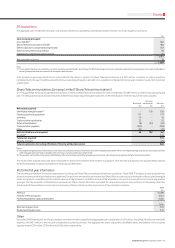

Notes to the consolidated nancial statements continued

“Improvements to IFRSs” was issued in April 2009 and its requirements are effective

over a range of dates, with the earliest being for annual periods beginning on or after

1 July 2009. This comprises a number of amendments to IFRSs, which resulted from

the IASB’s annual improvements project. The Group is currently assessing the impact

of adoption of these improvements on the Group’s results, financial position and cash

flows. The improvements have not yet been endorsed for use in the EU.

The Group has not adopted the following pronouncements, which have been issued

by the IASB or the IFRIC. The Group does not currently believe the adoption of these

pronouncements will have a material impact on the consolidated results, financial

position or cash flows of the Group. These pronouncements have been endorsed for

use in the EU, unless otherwise stated.

“Amendment to IFRS 2 Share-based Payment: Vesting Conditions and •

Cancellations”, effective for annual periods beginning on or after 1 January 2009.

“Amendments to IAS 32 Financial Instruments: Presentation and IAS 1 •

Presentation of Financial Statements – Puttable Financial Instruments and

Obligations Arising on Liquidation”, effective for annual periods beginning on or

after 1 January 2009.

“Amendments to IFRS 1, “First-time adoption of IFRS and IAS 27 Consolidated and •

Separate Financial Statements – Cost of an Investment in a Subsidiary, Jointly

Controlled Entity or Associate”, effective for annual periods beginning on or after

1 January 2009.

“Improvements to IFRSs” issued in May 2008 are effective over a range of dates, •

with the earliest being for annual periods beginning on or after 1 January 2009.

“Eligible Hedged Items: Amendment to IAS 39 Financial Instruments: Recognition •

and Measurement” is effective for annual periods beginning on or after 1 July

2009. This amendment has not yet been endorsed for use in the EU.

IFRS 1 (Revised), “First-time Adoption of International Financial Reporting •

Standards”, effective for periods beginning on or after 1 January 2009. This

standard has not yet been endorsed for use in the EU.

“Improving Disclosures about Financial Instruments: Amendments to IFRS 7 •

Financial Instruments: Disclosures”, effective for annual periods beginning on or

after 1 January 2009.

“Embedded Derivatives: Amendments to IFRIC 9 and IAS 39”, effective for annual •

periods ending on or after 30 June 2009.

IFRIC 15, “Agreements for the Construction of Real Estate”, effective for annual •

periods beginning on or after 1 January 2009. This interpretation has not yet been

endorsed for use in the EU.

IFRIC 16, “Hedges of a Net Investment in a Foreign Operation”, effective for annual •

periods beginning on or after 1 October 2008. This interpretation has not yet been

endorsed for use in the EU.

IFRIC 17, “Distributions of Non-cash Assets to Owners”, effective for annual periods •

beginning on or after 1 July 2009. This interpretation has not yet been endorsed

for use in the EU.

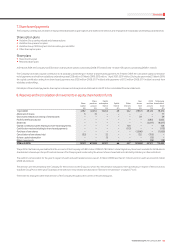

38. New accounting standards

The Group has not applied and does not intend to early adopt the following

pronouncements, which have been issued by the IASB or the International Financial

Reporting Interpretations Committee (‘IFRIC’).

IFRIC 13 “Customer Loyalty Programmes” was issued in June 2007 and is effective

for annual periods beginning on or after 1 July 2008. The interpretation addresses

how companies that grant their customers loyalty award credits when buying goods

or services should account for their obligations to provide free or discounted goods

and services. It requires that consideration received be allocated between the award

credits and the other components of the sale. This interpretation will not have a

material impact on the Group’s results, financial position or cash flows. This

interpretation has been endorsed for use in the EU. The Group adopted IFRIC 13 on

1 April 2009.

IAS 23 (Revised) “Borrowing Costs” was issued in March 2007 and is effective for

annual periods beginning on or after 1 January 2009. It requires the capitalisation of

borrowing costs, to the extent they are directly attributable to the acquisition,

production or construction of a qualifying asset. The option of immediate recognition

of those borrowing costs as an expense has been removed. This standard will not

have a material impact on the Group’s results, financial position or cash flows. This

standard has been endorsed for use in the EU. The Group adopted IAS 23 (Revised)

on 1 April 2009.

IFRS 3 (Revised) “Business Combinations” was issued in January 2008 and will apply

to business combinations occurring on or after 1 April 2010. The revised standard

introduces a number of changes in the accounting for business combinations that

will impact the amount of goodwill recognised, the reported results in the period that

a business acquisition occurs and future reported results. This standard is likely to

have a significant impact on the Group’s accounting for business acquisitions post

adoption. This standard has not yet been endorsed for use in the EU.

An amendment to IAS 27 “Consolidated and Separate Financial Statements” was

issued in January 2008 and is effective for annual periods beginning on or after 1 July

2009. The amendment requires that when a transaction occurs with non-controlling

interests in Group entities that do not result in a change in control, the difference

between the consideration paid or received and the recorded non-controlling

interest should be recognised in equity. In cases where control is lost, any retained

interest should be remeasured to fair value with the difference between fair value and

the previous carrying value being recognised immediately in the income statement.

The Group has historically entered into transactions that are within the scope of this

standard and may do so in the future. This amendment has not yet been endorsed

by the EU.

IAS 1 (Revised) “Presentation of Financial Statements” was issued in September 2007

and will be effective for annual periods beginning on or after 1 January 2009. The

revised standard introduces the concept of a statement of comprehensive income,

which enables users of the financial statements to analyse changes in an entity’s

equity resulting from transactions with owners separately from non-owner changes.

The revised standard provides the option of presenting items of income and expense

and components of other comprehensive income either as a single statement of

comprehensive income or in two separate statements. The Group does not currently

believe the adoption of this revised standard will have a material impact on the

results, financial position or cash flows. This statement has been endorsed for use in

the EU.

IFRIC 18 “Transfers of Assets from Customers” was issued in January 2009 and is

effective for transactions occurring on or after 1 July 2009. The interpretation

provides guidance on accounting by entities receiving property, plant and equipment

(or cash which must be used to construct or acquire property, plant and equipment)

which must then be used to either connect the customer to a network and/or provide

the customer with ongoing access to a supply of goods or services. The Group is

currently assessing the impact of the interpretation on it’s results, financial position

and cash flows. This interpretation has not yet been endorsed for use in the EU.