Vodafone 2009 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2009 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

Performance

Vodafone Group Plc Annual Report 2009 31

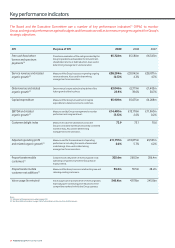

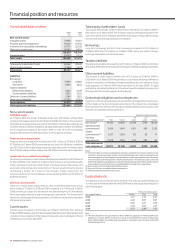

Revenue

Revenue increased by 14.1% to £35,478 million for the year ended 31 March 2008,

with organic growth of 4.2%. The impact of acquisitions and disposals was 6.5

percentage points, primarily from acquisitions of subsidiaries in India in May 2007 and

Turkey in May 2006 as well as the acquisition of Tele2’s fixed line communication and

broadband operations in Italy and Spain in December 2007. Favourable exchange

rate movements increased revenue by 3.4 percentage points, principally due to the

4.2% change in the average euro/£ exchange rate, as 60% of the Group’s revenue for

the 2008 financial year was denominated in euro.

Revenue grew in the Europe, Africa and Central Europe and Asia Pacific and Middle

East regions by 6.1%, 20.8% and 87.4%, respectively, with growth in the Asia Pacific

and Middle East region benefiting from an 81.9 percentage point impact from

acquisitions and disposals. On an organic basis, Europe recorded growth of 2.0%,

Africa and Central Europe delivered an increase of 13.6%, while Asia Pacific and

Middle East grew by 15.9%.

Organic revenue growth was driven by the higher customer base and successful

usage stimulation initiatives, partially offset by ongoing price reductions and the

impact of regulatory driven reductions. Growth in data revenue was particularly

strong, up 39.0% on an organic basis to £2,119 million, reflecting increased

penetration of mobile PC connectivity devices and improved service offerings.

Operating profit/(loss)

Operating profit increased to £10,047 million for the year ended 31 March 2008 from

a loss of £1,564 million for the year ended 31 March 2007. The loss in the 2007

financial year was mainly the result of the £11,600 million of impairment charges that

occurred in the year, compared with none in the 2008 financial year.

EBITDA increased to £13,178 million, with growth of 10.2%, or 2.6% on an organic

basis. The net impact of acquisitions and disposals reduced reported growth by

4.5 percentage points. The net impact of foreign exchange rates increased EBITDA

by 3.1 percentage points, as the impact of the 4.2% increase in the average euro/£

exchange rate was partially offset by the 5.7% and 7.2% decreases in the average

US$/£ and ZAR/£ exchange rates, respectively.

On an organic basis, EBITDA increased by 15.6% in Africa and Central Europe, driven

largely by a higher customer base and the resulting increase in service revenue. In

Asia Pacific and Middle East, EBITDA increased by 14.3% on an organic basis, with the

majority of the increase attributable to performances in Egypt and Australia. Europe’s

EBITDA declined by 0.1% on an organic basis compared to the 2007 financial year,

resulting from the continued challenges of highly penetrated markets, regulatory

activity and price reductions.

In Europe, EBITDA was stated after a £115 million benefit from the release of a

provision following a revised agreement in Italy relating to the use of the Vodafone

brand and related trademarks, which is offset in Common Functions, and was also

impacted by higher direct costs, customer costs and the impact of the Group’s

increasing focus on fixed line services, including the acquisition of Tele2 in Italy

and Spain.

In the Africa and Central Europe and the Asia Pacific and Middle East regions, EBITDA

was impacted by the investment in growing the customer base and the impact of the

acquisitions in Turkey and India, respectively. Both India and Turkey generated lower

operating profits than regional averages, partially as a result of the investment in

rebranding the businesses to Vodafone, increasing the customer base and improving

network quality in Turkey.

The Group’s share of results from associates grew by 5.5%, or 15.1% on an organic

basis. The organic growth was partially offset by a 5.5 percentage point impact from

the disposal of the Group’s interests in Belgacom Mobile S.A. and Swisscom Mobile

A.G. during the 2007 financial year and a 4.1 percentage point impact from

unfavourable exchange rate movements. The organic growth was driven by 24.8%

growth in Verizon Wireless.

Other income and expense for the year ended 31 March 2007 included the gains on

disposal of Belgacom S.A. and Swisscom Mobile A.G., amounting to £441 million and

£68 million, respectively.

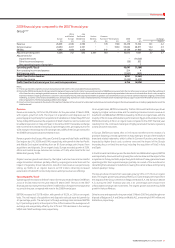

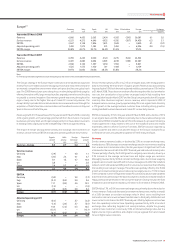

2008 nancial year compared to the 2007 nancial year

Group(1)(2)

Africa Asia

and Central Pacific and Verizon Common

Europe Europe Middle East Wireless Functions(3) Eliminations 2008 2007 % change

£m £m £m £m £m £m £m £m £ Organic

Revenue 26,081 4,946 4,399 − 170 (118) 35,478 31,104 14.1 4.2

Service revenue 24,430 4,617 4,101 − − (106) 33,042 28,871 14.4 4.3

EBITDA 9,690 1,669 1,476 − 343 − 13,178 11,960 10.2 2.6

Adjusted operating profit 6,206 752 530 2,447 140 − 10,075 9,531 5.7 5.7

Adjustments for:

Impairment losses − (11,600)

Other income and expense (28) 502

Non-operating income of associates − 3

Operating profit/(loss) 10,047 (1,564)

Non-operating income and expense 254 4

Net financing costs (1,300) (823)

Profit/(loss) before taxation 9,001 (2,383)

Income tax expense (2,245) (2,423)

Profit/(loss) for the financial year from continuing operations 6,756 (4,806)

Notes:

(1) The Group revised its segment structure during the year. See note 3 to the consolidated financial statements.

(2) During the 2009 financial year, the Group revised its analysis of revenue and costs. Visitor revenue and revenue from MVNOs are now reported in the line ‘other service revenue’, rather than within each

of the lines for voice, messaging and data revenue. In the revised presentation of costs: direct costs include amounts previously reported as interconnect costs and other direct costs, except for

expenses related to ongoing commission; customer costs include amounts previously reported within acquisition costs and retention costs, as well as expenses related to ongoing commissions,

marketing, customer care and sales and distribution; and operating expenses are now comprised primarily of network and IT related expenditure, support costs from HR and finance and certain

intercompany items. The following analysis reflects this change.

(3) Common Functions represents the results of the partner markets and the net result of unallocated central Group costs and recharges to the Group’s operations, including royalty fees for use of the

Vodafone brand.